FEDERAL COURT OF AUSTRALIA

Chowder Bay Pty Ltd v Paganin [2018] FCAFC 25

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

2. The cross-appeal be dismissed.

3. The appellants pay the respondents’ costs of the appeal (except for any costs incurred by the first respondent in relation to the notice of contention filed by the first respondent on 17 July 2017).

4. The cross-appellants pay the cross respondents’ costs of the cross-appeal.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

THE COURT:

A INTRODUCTION AND SUMMARY

1 This appeal primarily concerns the not unfamiliar circumstance of a valuer being sued for what is alleged to have been a misleading and deceptive valuation of commercial property.

2 The critical dealings and arguments that are the focus of the appeal are considered in detail below, but it is convenient to commence with a general overview of the dispute and how it was determined by the primary judge.

3 The appellants are six of 23 investors in a joint venture (Syndicate) involved in the redevelopment of a former caravan park in Busselton in Western Australia as a residential ‘resort’ (Resort). The appellants and other investors subscribed sums in exchange for units in a Unit Trust and other proprietary and contractual rights (described below), including the right to the allocation of a portion of the Resort property, upon which a villa would be built. It was proposed that the balance of unallocated villas would be sold to third parties, with the profits from such third party sales to be distributed to the various joint venturers with the goal of investors, at the end of the project, obtaining the benefit of securing a villa for an outlay considerably less than its ‘market’ value.

4 St George Bank Ltd (Bank) provided an indicative finance proposal to the promoters (Ibex companies) for a loan facility (Facility) with a total facility limit of $32.3 million. The Facility was to be used to finance the construction and development of the Resort. Unsurprisingly, the approval of the Facility was conditional upon terms that included an acceptable loan to value ratio (LVR), with the ratio to be calculated by reference to a valuation of the development property on various bases. The Bank commissioned a valuation from the third respondent (Egan Valuers), which was prepared by the fourth respondent (Mr Smith). The valuation obtained, dated 1 June 2008 (First Valuation), relevantly valued the Resort on an “As If Complete” basis, subject to qualifications, in the amount of $67,785,197 (GST exclusive). Later, another valuation was provided to the Bank, which noted the opinion as to “market valuation assessments”, as expressed in the First Valuation, remained “unchanged” as at 30 October 2008 (Later Valuation).

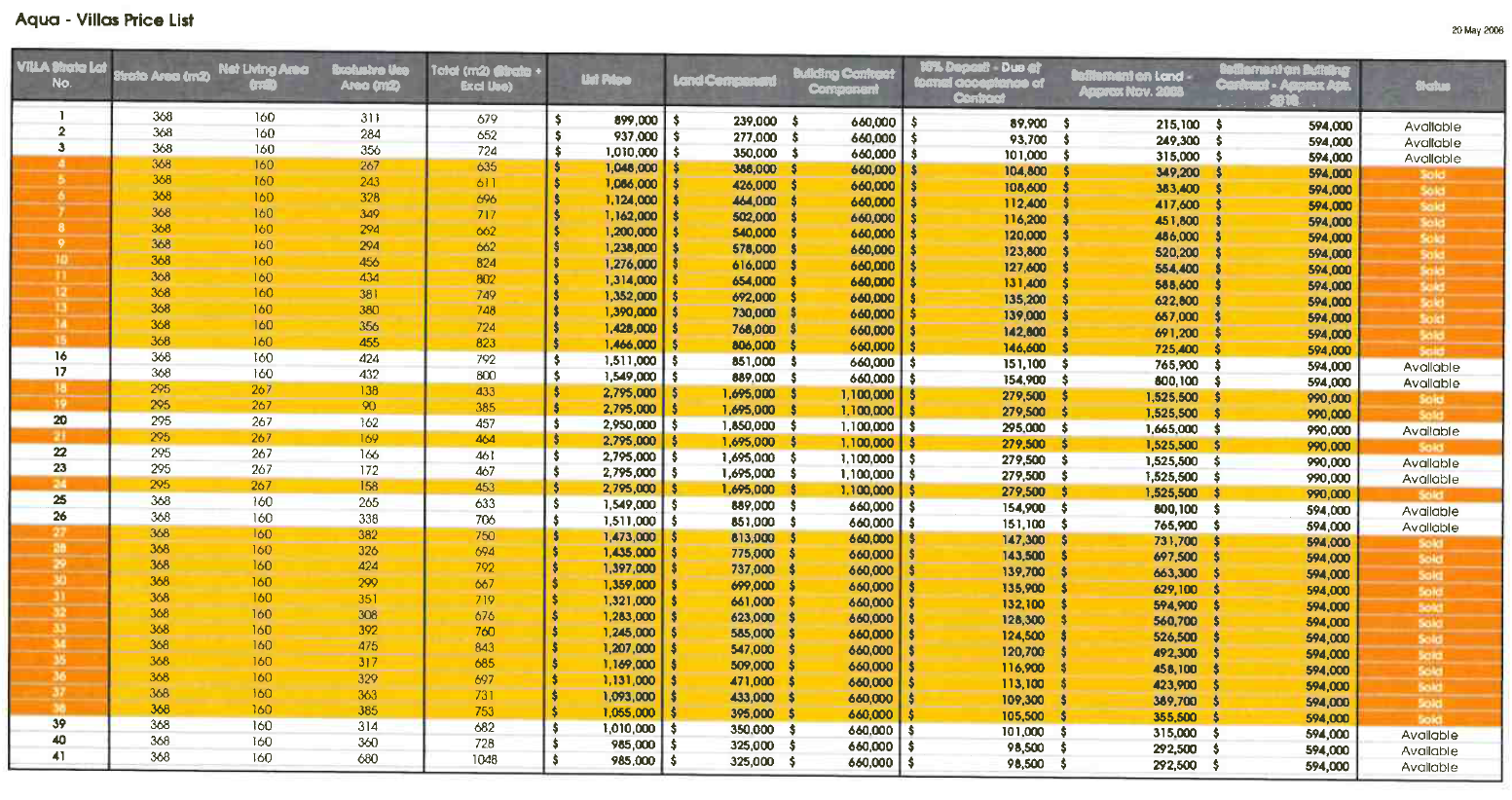

5 As will be obvious given the way the transaction was structured, the villas to be allocated to the investors were not ‘sold’ in the sense that they were the subject of contracts for sale of land, or presale contracts, for a consideration reflecting the then market value of the lot. Notwithstanding this, for the purpose of the First Valuation, on 5 June 2008, Egan Valuers was provided by one of the Ibex companies, Ibex Capital Pty Ltd (Ibex Capital) with, among other things, a document bearing the file name “AQUA.Villa Pricing & Sale Schedule” and another document with the file name “AQUA.Third-party Sale Schedule”. The first of these documents (which had the heading “Aqua – Villas Price List”) recorded that, of the 41 villas, 28 had been “Sold”, and also recorded a “List Price” for each of the villas; the document also identified 13 villas as being “Available” (June Price Schedule). The June Price Schedule is reproduced as Schedule A to these reasons.

6 The documents were dated 20 May 2008 and, as by now should be evident, the “List Price” for the villas allocated to the investors was a notional amount ascribed by Ibex Capital to each lot. The notional prices were arrived at following internal discussion and consultation with agents who were to market the available lots, and then were determined by a ‘Compliance Committee’.

7 Importantly, in relation to the non-existent presale contracts, Egan Valuers, in the First Valuation, noted that liability for the valuation was “extended” subject to the Bank being satisfied the presales were legitimate market transactions and, in relation to the Later Valuation, recommended that the Bank obtain the contracts and confirm their acceptability to the Bank. As will become evident, these qualifications, which can conveniently be called the Presales Qualifications, are of central importance to the appeal.

8 It should also be noted for the purposes of this overview that a few weeks before the Later Valuation, Ibex Capital had written to the investors (Ibex Letter) including an extract of a valuation table from the First Valuation, which specified villa values.

9 In any event, following the Bank’s receipt of the Later Valuation, the Facility was approved, drawdowns took place and the Resort was constructed and completed. Unfortunately, the development was not a success and the Ibex companies, in December 2010, corresponded with the investors, advising that the villa values were significantly below the values referred to in the Ibex Letter; that the Ibex companies were unable to sell the villas in the Resort which were “Available” to prospective third-party purchasers; and that the Facility required repayment very shortly. The Facility was not repaid and, in April 2011, the Bank appointed receivers and managers.

10 The appellants allege that Egan Valuers engaged in conduct in contravention of various statutory norms in providing the First Valuation and the Later Valuation (collectively, the Valuations) and that Mr Smith was involved in that contravening conduct (and himself engaged in misleading or deceptive conduct). They also contend that each of the first respondent (Mr Paganin) and the second respondent (Mr Robertson), being directors of the Ibex companies (together, the Directors), engaged in, or were involved in, misleading or deceptive conduct by the Ibex companies, by providing presale schedules, by failing to provide instructions to Egan Valuers to correct the First Valuation, and in relation to the provision of the Ibex Letter to investors.

11 These claims were rejected by the primary judge who, in summary, found:

(a) “a generally reliable estimate” of the value of the Resort, as at the date of the Valuations, was $45,500,000 (GST exclusive): at [225], [226], [285];

(b) the Valuations were misleading or deceptive “if they stood alone” because they did not provide an accurate valuation of the Resort: at [226], [285];

(c) the Valuations were not, however, misleading or deceptive because they were “replete with advice that the Bank needed to satisfy itself as to the existence of the relevant presale contracts” (being the Presales Qualifications): at [234], [293];

(d) there was “no evidence to prove” the Bank was misled or deceived or relied on the Valuations: at [233], [235]; and it could not be concluded that the Bank would not have provided the Facility but for the Valuations and that the Resort would not have been built: at [352];

(e) the provision of the price list by the Ibex companies was not misleading nor deceptive as Egan Valuers and Mr Smith understood that the investors were part of the Syndicate and the identification of the relevant investor lots in the price list as “Sold” was not, in the circumstances, apt to mislead: at [257]-[258]; and hence neither Mr Paganin (who was not responsible for providing instructions or information to Egan Valuers: see [301]) nor Mr Robertson (who had greater involvement) were engaged in, or were relevantly concerned in, contravening conduct as to the price list: at [311];

(f) neither the Ibex companies nor the Directors were required to provide instructions to correct the First Valuation by disclosing the various syndicate agreements in circumstances where Egan Valuers, through Mr Smith, was aware of the Syndicate, and the Directors were not bound to correct some misunderstanding following the provision of the First Valuation: at [267]-[269];

(g) the Ibex Letter did not materially alter the understanding initially conveyed to the investors and was not misleading nor deceptive: at [286]-[289]; and hence neither of the Directors were engaged or involved in contravening conduct in relation to the Ibex Letter: at [327].

B THE SCOPE OF THE APPEAL

12 The case of the appellants on the appeal transformed significantly from the case advanced below. It had a beguiling simplicity. The multifarious representations pleaded in the statement of claim were confined to the contention that Egan Valuers represented to the Bank that the “As If Complete” value of the Resort as at the time of the Valuations was $69,856,500 and that this representation was falsified by reason of the fact that the values at the time of the Valuations were “substantially less than that”: see Statement of Claim (SOC) [40(f)], [41(g)]. Notwithstanding the abandonment of the other pleaded alleged misrepresentations, the argument developed on appeal travelled beyond the one representation which had been pleaded and maintained (SOC [40(f)]). The argument articulated by Senior Counsel for the appellants, Mr Walker QC, proceeded as follows:

(a) given the acceptance by the primary judge that a Resort valuation of $45,500,000 ought to be accepted, it followed that the Valuations were misleading as they were likely to lead the Bank into error because they materially overvalued the Resort;

(b) Egan Valuers communicated to the Bank that: (i) there was a reasonable basis for the Valuations when there was not on the findings of the primary judge; and (ii) that the Later Valuation could be relied upon for mortgage security purposes when it could not;

(c) the primary judge’s finding that the Valuations were, in effect, rendered inoperative because of the Presales Qualifications was erroneous because the qualification as to presales in the Later Valuation did not “detract from the force of expression of opinion by [the] Egan Valuations”;

(d) it was plain that the Bank relied upon the Later Valuation for mortgage security purposes and the primary judge fell into error in concluding that there was a want of evidence to prove the counterfactual that the Bank would not have provided the Facility (and hence the Resort would not have been built);

(e) the evidence established that there was contravening conduct on the part of Egan Valuers and Mr Smith, and the losses suffered by the appellants by reason of the development of the Resort were sufficiently causally connected to that contravening conduct such as to require an award of statutory compensation.

13 Additionally, the case against the balance of the respondents was narrowed. The only conduct of the Directors relied upon on appeal was conduct which was said to have led Egan Valuers and Mr Smith into error; it followed that Senior Counsel for the appellants accepted (T 38) that it was only if contravening conduct could be proved in relation to the Valuations (or at least the Later Valuation), that causation could be established such as to render the Directors liable for any of their impugned conduct. Put another way, as now pressed on appeal, the point of departure of any case against the Directors was that the Valuations were misleading or deceptive and that a necessary condition of establishing causation against the Directors was that the Bank relied upon contravening conduct proved against Egan Valuers and Mr Smith.

14 In these circumstances, it is convenient for these reasons to deal: first, with the case concerning the Valuations; and secondly, with the case against the Directors. Following the determination as to whether the primary judge erred as the appellants contend, consideration will then be given to: thirdly, issues that arise in relation to the appropriate remedial response in the event the appellants did establish error; and fourthly, a contention that certain costs incurred by the appellants in other litigation did not properly form part of the loss properly recoverable in the event the appellants otherwise succeeded. In addressing these matters, the balance of these reasons will be organised into the following sections:

Section C: Were the Valuations Misleading?

C.1 Relevant Findings and Contextual Matters

C.2 The Applicable Law

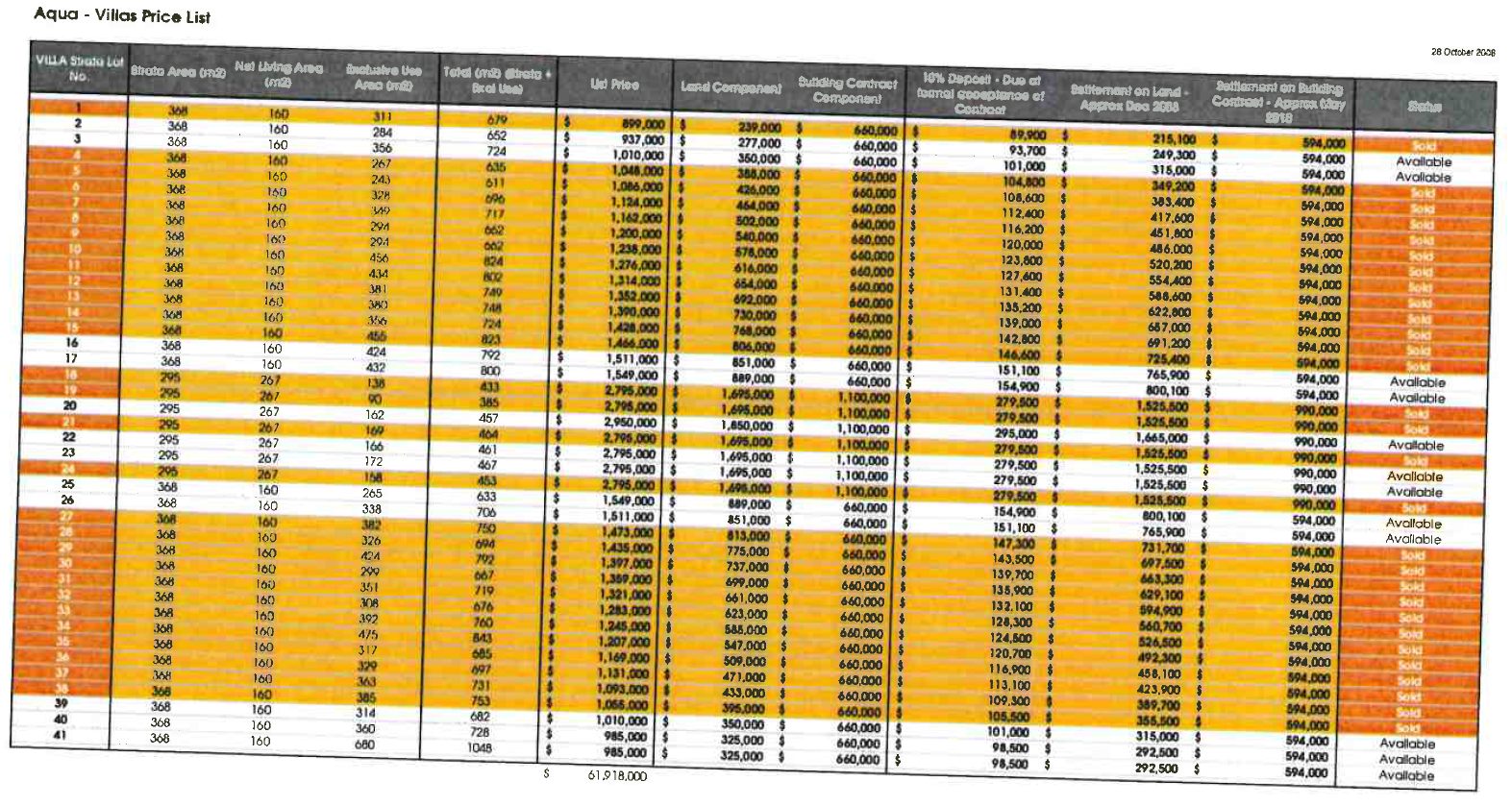

C.2.1 The Statutory Norms Relied Upon

C.2.2 The Principled Approach to Characterisation of Conduct

C.3 The Presales Qualifications

C.4 The Later Valuation and the Dealings between Egan Valuers and the Bank

C.5 Conclusions as to the Conduct of Egan Valuers and Mr Smith

Section D: The Bank and Reliance

D.1 A Preliminary Matter: Reliance and Causation

D.2 The Finding as to a Want of Reliance and the Evidence

D.3 Consideration of Evidence as to the Bank’s Reliance

Section E: Additional Issues as to Causation

Section F: The Case Against the Directors

Section G: Issues as to Relief

Section H: The “Cross-Appeal” and the Notice of Contention

Section I: Conclusion and Orders

C WERE THE VALUATIONS MISLEADING?

C.1 Relevant Findings and Contextual Matters

15 It is trite that the consideration as to whether particular conduct is misleading or deceptive is a question of fact to be determined in the context of the evidence as to the alleged conduct and all relevant surrounding facts and circumstances: Taco Company of Australia Inc v Taco Bell Pty Ltd (1982) 42 ALR 177 at 199 per Deane and Fitzgerald JJ. A fundamental requirement is that, in the circumstances, the impugned conduct induces or is capable of inducing error: Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd (1982) 149 CLR 191 at 198 per Gibbs CJ. It necessarily follows that context is critical.

16 A general overview of the relevant surrounding facts and circumstances has already been provided in Section A. Although the requirement is to have regard to all relevant facts and circumstances, there is, obviously enough, in any case, a hierarchy in the importance of relevant circumstances and specific attention should be directed to five matters arising from findings of the primary judge and the dealings between Egan Valuers and the Bank. These matters are not exclusive considerations but assume particular importance in both considering how the primary judge assessed the impugned conduct and also in evaluating the argument of the appellants.

17 First, it is important to understand the nature of the interests of the investors in the Syndicate. The 23 investors, including the appellants, each subscribed the sum of $500,000 and executed a series of syndicate agreements being: a Unit Trust Deed (with the investors as unit holders); an “Investor Agreement”; and the “Aqua Joint Venture Agreement” and “Aqua Development Management Agreement” (between, among others, Ibex Capital, the trustee of the Unit Trust and the investors as joint venturers and “villa owners”). The primary judge concluded that this web of arrangements relevantly disclosed the following structure:

(a) each Syndicate member held one twenty-third of the units issued in the Unit Trust;

(b) the construction and development of the Resort would be undertaken by the three participants in the Syndicate, being Ibex Capital as to a 9.89% share, the trustee of the Unit Trust as to a 43.65% share and each of the 23 Syndicate members as to a 2.02% share (totalling 46.46%);

(c) Ibex Aqua Pty Ltd was the development manager for the construction and development of the Resort;

(d) each investor would be allocated a separate lot, together with a share of the common property as tenants in common on registration of the plan of subdivision and partition, and would become registered as the proprietor of the lot, on which a villa would be constructed;

(e) apart from the sums subscribed, Syndicate costs and expenses to construct and complete the Resort would be paid by borrowed monies, giving rise to Syndicate debt, which debt was to be repaid from the sale of villas comprising part of the developed Resort (other than villas allocated to the investors and also to Ibex Capital);

(f) profits from the sale of the available villas to third parties, after payment of all Syndicate debt, would be distributed to the joint venturers.

18 It follows from the above that each investor’s interest comprised:

(a) a proprietary interest in land which, prior to allocation of the lots, was an interest as a tenant in common; and after allocation of the lots, as a registered proprietor of a lot at the developed Resort, upon which their villa would be constructed, together with their share of the common property; and

(b) their rights, through the Unit Trust and the related contractual documentation.

19 Secondly, it is important to understand the extent of the Bank’s knowledge of these matters. The primary judge found at [228]-[229] that the Bank “knew full well, or should be taken to have known” the true position in relation to the Resort development, that there was the Syndicate, and that the investors were not in the “position of third party, arm’s length purchasers of villas in the project”. It is worth pausing to stress that whatever may have been indications in contemporaneous business records as to a less than complete appreciation by various Bank employees of the substance of the Syndicate arrangements (see, for example, [38] below), the findings of the primary judge as to knowledge of the Bank were unchallenged. Moreover, no party suggested that anything turned on the use by the primary judge of the words “should be taken to have known” which, in other contexts, might be thought to be words of attribution of knowledge where actual knowledge did not exist. Indeed, for differing reasons, each party emphatically embraced the finding that the Bank had actual knowledge of the matters to which his Honour referred.

20 Thirdly, in contrast to the Bank’s knowledge, his Honour accepted (at [232]) that “at one level…there was some real confusion, perhaps between the valuers’ understanding and that of the Bank as to the nature of the presales” and the related conclusions that:

(a) Mr Smith (and through him) Egan Valuers “laboured under some misapprehension” as to “the legal nature of the syndicate and the interests held” by the investors and that Mr Smith “plainly treated them as being the subject of concluded (or to be concluded) presale contracts” (at [227]); and

(b) notwithstanding that presale contracts did not exist for the investors’ villas, “[i]t was obvious Mr Smith believed they existed” and that the Valuations had been given to the Bank on this basis (at [229]).

21 It appears that the primary judge spoke in terms of confusion rather than ignorance because, as noted above at [11(e)] and [11(f)] above, his Honour did find that Egan Valuers and Mr Smith at least understood that the investors were part of the Syndicate and any conduct of the Directors in identifying the relevant investor lots on the June Price Schedule as being “Sold” did not mislead.

22 Fourthly, there are the Presales Qualifications to which general reference has already been made and which assumed central significance in the primary judge’s reasoning. These qualifications will be examined, in detail, in Section C.3 below.

23 Fifthly, the matter which assumed particular significance in the appellants’ oral argument on appeal was that, notwithstanding his Honour’s finding that the “Bank knew that 25 of the ‘presales’ were not on an arm’s length basis”, by an email dated 4 November 2008, the primary judge further found (at [231]) that Ms Kylie Gilbey, the Business Development Manager of the Bank “explicitly mentioned [these] matters to Mr Smith and asked him to confirm his valuation on that basis”. These critical dealings between the Bank and Mr Smith leading up to the provision of the Later Valuation will also be examined in detail, in Section C.4 below.

24 Before descending to the detail of the Presales Qualifications and the precise dealings leading up to the provision of the Later Valuation, it is useful to focus briefly on the provisions the appellants allege were contravened and the principled approach to assessing whether they have been breached.

C.2 The Applicable Law

C.2.1 The Statutory Norms Relied Upon

25 As is already evident, the events giving rise to this claim occurred almost a decade ago. Given its vintage, this dispute presumably provides one of the last times an intermediate court of appeal will need to have regard to the 23 words of s 52 of the Trade Practices Act 1974 (Cth) (TPA) which, as Justice Finn observed, writing extra-judicially, “worked a revolution in Australian law”: see Finn P, “Equitable Doctrine and Discretion in Remedies” in Cornish W, Nolan RC, O'Sullivan J and Virgo GJ (eds), Restitution Past, Present and Future – Essays in Honour of Gareth Jones (Bloomsbury Publishing, 1988), Ch 17.

26 Of course, as might now be expected, the appellants also pleaded that the conduct upon which they relied contravened s 1041H of the Corporations Act 2001 (Cth), s 12DA of the Australian Securities and Investments Commission Act 2001 (Cth) and s 10(1) of the Fair Trading Act 1987 (WA) (FTA). No attempt was made, however, to distinguish between these statutory norms, nor did the respondents suggest that the TPA did not apply. Accordingly, the analysis can proceed as it did below and in submissions, by reference to the relevant provisions of the TPA, and the vitals of cognate provisions can be put to one side. The only exception is the direct liability case advanced against the Directors under the FTA (see SOC [56]), when the case against the Directors under the TPA is one of accessorial liability (see SOC [55]).

C.2.2 The Principled Approach to Characterisation of Conduct

27 Given the nature of the claim, it is unsurprising that there was no difference between the parties as to the applicable principles. Despite this, it is worth emphasising some bedrock notions which inform the assessment as to whether the primary judged erred in finding that no contravention was established. Reference has already been made to Parkdale, where Gibbs CJ, at 198, observed that consideration must be given to the class of persons likely to be affected by the conduct. However, in cases such as the present where the misleading or deceptive conduct is directed not to a class but to a specific individual or entity, the court must necessarily take into account the knowledge of the person to whom the conduct is directed: Butcher v Lachlan Elder Realty Pty Ltd [2004] HCA 60; (2004) 218 CLR 592 at 604-605 per Gleeson CJ, Hayne and Heydon JJ. In this regard, as French CJ noted in Campbell v Backoffice Investments Pty Ltd [2009] HCA 25; (2009) 238 CLR 304 at 319 [26]:

Characterisation [of the conduct] may proceed by reference to the circumstances and context of the questioned conduct. The state of knowledge of the person to whom the conduct is directed may be relevant, at least in so far as it relates to the content and circumstances of the conduct.

28 Here, of course, as Egan Valuers and Mr Smith stressed, the recipient of the relevant representations as to value was a bank lending on security over land, an obviously sophisticated consumer of valuation services. Moreover, it is not only the situational or relative commercial position of representor and representee that is relevant, but the specific dealings which related to the impugned conduct: see Butcher at 604-605 per Gleeson CJ, Hayne and Heydon JJ.

29 What is also clear is that in determining whether any particular conduct is misleading or deceptive is a question of fact to be determined objectively. In Campbell at 341-342, Gummow, Hayne, Heydon and Kiefel JJ approved the following statements of McHugh J in Butcher at 625 [109]:

The question whether conduct is misleading or deceptive or is likely to mislead or deceive is a question of fact. In determining whether a contravention of s 52 has occurred, the task of the court is to examine the relevant course of conduct as a whole. It is determined by reference to the alleged conduct in the light of the relevant surrounding facts and circumstances. It is an objective question that the court must determine for itself. It invites error to look at isolated parts of the [person’s] conduct. The effect of any relevant statements or actions or any silence or inaction occurring in the context of a single course of conduct must be deduced from the whole course of conduct. Thus, where the alleged contravention of s 52 relates primarily to a document, the effect of the document must be examined in the context of the evidence as a whole. The court is not confined to examining the document in isolation. It must have regard to all the conduct of the [person] in relation to the document including the preparation and distribution of the document and any statement, action, silence or inaction in connection with the document.

(Emphasis added, citations omitted)

30 This task is more straightforward when one is dealing with the representation of existing fact; representations as to opinions, such as valuations, raise particular issues. The initial step is to identify precisely what representations the statement of opinion entails. French CJ remarked on the importance of properly characterising the representation in Campbell at 321 [32]-[33], where his Honour observed:

It is important in considering whether conduct is misleading or deceptive to identify clearly the conduct to be characterised…

Opinions may carry with them one or more implied representations according to the circumstances of the case. There will ordinarily be an implied representation that the person offering the opinion actually holds it. Other implied representations may be that the opinion is based upon reasonable grounds, which may include the representation that it was formed on the basis of reasonable inquiries. In the case of a person professing expertise or particular skill or experience the opinion may carry the implied representation that it is based upon his or her expertise, skill or experience.

31 Despite generalised complaint by Senior Counsel for Egan Valuers and Mr Smith as to the pleading and, more particularly, as to the appellants’ failure below to adopt the common course of specifying the implied representations said to have been conveyed, there was no issue that the statements of opinion, contained in the Valuations, read in the light of all the relevant circumstances, would be misleading and deceptive if those opinions as to value were not based on reasonable grounds, were not the product of due care and skill and could not reasonably be held on the basis of information available to the representors (Egan Valuers and Mr Smith) at the times the opinions were conveyed: see Campbell at 321 [33] and 327 [50] per French CJ; MGICA (1992) Ltd (formerly MGICA Ltd) v Kenny & Good Pty Ltd (1996) 140 ALR 313 at 356-357 per Lindgren J; Bathurst Regional Council v Local Government Financial Services Pty Ltd (No 5) [2012] FCA 1200 at [2164] and [2416] per Jagot J.

32 Having identified the relevant principles, it is convenient to focus next on two contextual matters to which reference has already been made (in [22] and [23] above) but which are of central importance in understanding the reasoning of the primary judge in dismissing the case advanced below.

C.3 The Presales Qualifications

33 As noted at [11] above, the primary judge determined the Valuations were not, in the end, misleading or deceptive notwithstanding that his Honour accepted that the Valuations would have been misleading or deceptive if the opinions as to value “stood alone”: at [226] and [284]. The reason why the primary judge reached this conclusion is best seen by reference to [230]-[235] where his Honour, after noting the advice given that the Bank needed to satisfy itself of the existence of the presale contracts, reasoned as follows:

In those circumstances, a question arises whether that factor alone is sufficient to cause the applicants’ claim against the valuers to be dismissed. That is to say, given what the Bank knew or should be taken to have known at material times, can it be said that the valuations misled or deceived the Bank, or that the Bank relied on misleading and deceptive valuations?

…

It may be accepted at one level that there was some real confusion, perhaps between the valuers’ understanding and that of the Bank as to the nature of the presales, but the applicants have not established that the Bank was relevantly misled or deceived by the valuations prepared by Mr Smith, or that the Bank relied on misleading or deceptive valuations.

While, as I say, it might be contended that there was a potential in the circumstances for the Bank to have been confused, or misled or deceived by those valuations, the applicants have not established that they were. No person from the Bank was called to give any evidence to the contrary.

As the valuers submit, the valuations were replete with advice that the Bank needed to satisfy itself as to the existence of the relevant presale contracts. In circumstances where the Bank has not been shown to have been ignorant of the true position involving the joint venture, the syndicate and the relevant contractual arrangements between the investors and the other parties under the syndicate agreements, the effective advice provided by the valuers as to their assumptions in giving the valuations should be given weight in the particular circumstances of this case. The Bank was specifically told at the time of the provision of the 30 October 2008 Egan valuation, to “obtain copies of the presales contracts to confirm their authority as liability for our valuation is extended subject to these contract being confirmed as accepted to the Bank”.

It is, in those circumstances, difficult to finally conclude that the Egan valuations were misleading or deceptive, or likely to mislead or deceive the Bank. Certainly, there is no evidence to prove the Bank was misled or deceived or relied on valuations that were misleading or deceptive.

34 Although there is reference in these passages to a lack of evidence from Bank witnesses (a matter dealt with below), what these passages illustrate is the centrality of the Presales Qualifications to the primary judge’s overall characterisation of the relevant conduct. Put simply, his Honour accepted the submissions made on behalf of Egan Valuers and Mr Smith that it was a condition of the Valuations that the Bank sight the presale contracts and be satisfied that the presales were legitimate market transactions and that unless and until that happened, the Valuations could not be regarded as being ‘operative’.

35 In this regard, Egan Valuers and Mr Smith had placed particular emphasis before his Honour on clauses 12-13 of the First Valuation which stated:

12. We have assumed that the 25 existing investors have entered into presale contracts for the purchase of vacant survey strata lots and construction of the proposed beach houses.

13. Liability for the valuation is extended to [the Bank] for lending purposes subject to the [Bank] sighting the additional contracts and being satisfied that the 25 presales are legitimate market transactions with reasonable deposits or investment funds forwarded to and held by the developer.

36 The circumstances surrounding the finalisation of the Presales Qualifications in the Later Valuation and its precise terms are set out in Section C.4 below, but, in broad terms, in the Later Valuation, the recommendation that the Bank obtain copies of the presale contracts to confirm their authenticity was repeated, as was the condition that the extension of liability was made subject to the presale contracts being confirmed “as acceptable to the Bank”.

C.4 The Later Valuation and the Dealings between Egan Valuers and the Bank

37 In [23] above, reference was made to the important dealings between the Bank and Mr Smith immediately leading up to the provision of the Later Valuation in early November 2008. It will be recalled, in examining these events, that somewhat earlier, on 2 September 2008, conditional approval was granted by the Bank to provide the Facility and, a few days later, on 4 September 2008, Ibex Aqua Pty Ltd was sent an indicative letter of offer and there was internal Bank discussion about an issue that had arisen as to the provision of joint and several guarantees from the investors. In this context, a comment was made, in a recommendation signed by both Ms Gilbey and also Mr Justin Pearce, the Senior Relationship Manager, that an issue had arisen concerning the provision of guarantees, but notwithstanding this, the Facility was “still supported” and was recommended on the basis that, among other things, “LVR on completion is a strong 46.2%” and “[t]otal pre-sales are $45M and held (based on valuation at June 2008)”. It was also said that “$34.7M pre-sales are provided by high net worth Syndicate Members, each having provided $500K non refundable deposit, which is considered to provide comfort in the intention to finalise the pre-sale settlement for each Syndicate Member villa” (AB3576).

38 It is worth pausing to note that this last comment, although consistent with his Honour’s findings (referred to in [19] above) that the Bank knew there was the Syndicate, and that the investors were not in the “position of third party, arm’s length purchasers of villas in the project”, did demonstrate a somewhat maladroit understanding by Ms Gilbey and Mr Pearce as to the legal and practical effect of those arrangements. The $500,000 was not a deposit pending settlement of the presales in the conventional sense, but rather an amount subscribed in consideration of the receipt of the units in the Unit Trust and other rights as a joint venturer in the Syndicate (as explained at [18] above).

39 Consistent with the communication by the Bank internally that the proposed facility was still supported, on 28 October 2008 at 1:28 pm, Ms Gilbey sent an email to Mr Smith (AB4201). It was in the following terms:

As discussed, [the Bank] has approved a facility to fund the proposed Aqua Resort project and is required to rely on your valuation for mortgage purposes. Accordingly can you please:

i) Update/ extend the date on the valuation so that the Bank can rely on the valuation for an additional 3 month period from now, and

ii) …

iii) confirm the current level of presales. I believe that another pre-sale has been obtained (and the builder – Sizer might be taking one of the villa’s [sic]). Could you also please check the level of single level pre-sales on page 32 on [the First Valuation].

I will ask [Mr Robertson] to confirm the current level of presales to you separately

Thank you and I look forward to receiving your updated assignment.

40 Ms Gilbey forwarded a copy of the email that she sent to Mr Smith to Mr Johnny Sheldrick, Development Manager of Ibex Capital (AB4198). Very shortly thereafter, at 2:37 pm on 28 October 2008, Mr Sheldrick wrote to Mr Smith in the following terms (AB4195):

Hi [Mr Smith],

We understand that [the Bank] have forwarded an instruction to [Egan Valuers] in relation to a couple of issues. Items 1 & 2 of [Ms Gilbey’s] email seem to require no assistance from us.

However, item 3 requires confirmation of the current level of pre-sales.. [sic] Please find attached schedule which confirms that Lot 1 has been sold. We confirm that Warren Sizer has purchased this Lot.

41 The schedule was dated 28 October 2008, headed “Aqua - Villas Price List” and, like the June Price Schedule, in respect of every villa lot: (a) identified a “Land Component” and a “Building Contract Component”; (b) made reference to a figure said to represent “10% Deposit – Due at formal acceptance of Contract”; (c) referred to amounts for each villa lot said to represent “Settlement on Land - Approx Dec 2008” and “Settlement on Building contract - Approx May 2010”; and (d) had a “Status” column noting whether the villa lot was “Sold” (an appellation given to lots including the investors’ villa lots) or “Available” (being the balance of the lots to be sold). This document merits review in its native form and a copy of it (October Price Schedule) is reproduced as Schedule B to these reasons.

42 Minutes later, Mr Sheldrick sent to the Directors a copy of Ms Gilbey’s email and advised that Mr Smith was visiting the site the following Thursday (30 October). Mr Paganin’s response was to send an email to Mr Robertson as follows (AB4197):

[Mr Robertson],

You will need to manage this process with [Mr Smith] to get it over the line - thanks

43 Following the site visit, on 3 November 2008, Mr Smith sent a letter to Ms Gilbey advising his opinion that the “market valuation assessments within our original report”, that is, the First Valuation, were unchanged as at the date of his site visit, that is, 30 October 2008 (AB4215).

44 The response of Ms Gilbey, sent on the morning of 4 November 2008, was to write to Mr Smith in the following terms (AB4249):

Hi [Mr Smith]

Thanks for the updated valuation letter and the very quick turnaround.

After speaking to our credit, just wondering if you could amend the wording slightly in your letter to clearly state that:

i) [the Bank] can rely on the updated valuation for a period of 3 months from the date of inspection, and

ii) that we can rely on it for the purposes of mortgage security.

We also note that 25 of the pre-sales are not arms [sic] length as they are syndicate members involved in this deal and one is to the builder so, could you please confirm the valuation on this basis.

(Emphasis added)

45 Mr Smith then reissued the original version of his letter on 3 November 2008. The revisions are of some importance. Set out in the table below, on the left, is the original version of the letter of 3 November 2008 and, on the right, is the revised version (bearing the same date, but sent on 4 November 2008), which followed on from Ms Gilbey’s request to Mr Smith for the revised letter to “clearly state” that the Bank could rely on the Later Valuation “for the purposes of mortgage security” and “confirm the valuation on [the] basis” that 25 presales were not arm’s length.

Original Version (AB4215) | Revised Version (being the Later Valuation), bold in the original, the underlining identifies the changes (AB4233) |

Dear Madam, RE: VALUATION – 605 (LOT 100) BUSSELL HIGHWAY, BROADWATER, WA 6280 PROPOSED “AQUA RESORT” We refer to your email request dated 28 October 2008 to: 1. Update/extend the date of our original valuation of 1 June 2008 2. Confirm that the Foreshore Reserve (to be ceded to Shire of Busselton) does form part of the valuation 3. Confirm current level of presales We confirm that we have undertaken an inspection of the property on 30 October 2008 with a view to providing a revision of our valuation assessment. At the time of inspection buildings were being/had been demolished and civil works were underway (refer attached photographs). We have been provided with an updated presale schedule from Ibex Capital (copy attached) indicating one further sale since our original valuation. Proposed Lot 1 has been sold at list price however, as with our original assessment, a copy of the contract has not been provided. We recommend that [the Bank] obtain copies of the presale contracts to confirm their authenticity as liability for our valuation is extended subject to these contracts being confirmed as arm’s length. Although recent economic events have adversely affected the demand for property in WA, the extend [sic] of presales within the subject project and an anticipated 11 month selling period for the remaining 12 lots should secure the profitability of the project. We also note that the majority of presales are based on significant individual investments in the original land acquisition syndicate. We have attached a revised “Gross Realisation” assessment which takes into account the additional presale. Having revisited the site and reviewed the original valuation assessment we are of the opinion that the market valuation assessments within our original report are unchanged as at 30 October 2008. We point out, however that the original assessment was undertaken on the assumption that all purchasers would include the plunge pool option in the contracts. We recommend that adjustments be made to the “As if Complete” assessments if purchase contracts are found to vary from this assumption. The original valuation was undertaken in accordance with the Draft Strata Plan and Condition 28 of the letter of Planning Consent (Shire of Busselton) whereby the proposed Foreshore Reserve is Vested in the Crown and ceded free of cost. We confirm that no value has been attributed to the Foreshore Reserve of 1,688m2 in our valuation assessment. We trust this advice is sufficient for your requirements and advise that this letter is subject to the Assumptions, Conditions and Limitations contained in our original report. This advice should be read in conjunction with our original report. Yours faithfully BLAKE SMITH A.A.P.I DIRECTOR, EGAN NATIONAL VALUERS (WA) CERTIFIED PRACTISING VALUER LICENSED VALUER No. 530 FOR THE STATE OF WESTERN AUSTRALIA Appendices St George Bank Request Revised “Gross Realisation” Schedule Revised Price List Photographs | Dear Madam, RE: VALUATION – 605 (LOT 100) BUSSELL HIGHWAY, BROADWATER, WA 6280 PROPOSED “AQUA RESORT” We refer to your email request dated 28 October 2008 to: 1. Update/extend the date of our original valuation of 1 June 2008 2. Confirm that the Foreshore Reserve (to be ceded to Shire of Busselton) does form part of the valuation 3. Confirm current level of presales We confirm that we have undertaken an inspection of the property on 30 October 2008 with a view to providing a revision of our valuation assessment. At the time of inspection buildings were being/had been demolished and civil works were underway (refer attached photographs). We have been provided with an updated presale schedule from Ibex Capital (copy attached) indicating one further sale since our original valuation. Proposed Lot 1 has been sold at list price however, as with our original assessment, a copy of the contract has not been provided. We recommend that [the Bank] obtain copies of the presale contracts to confirm their authenticity as liability for our valuation is extended subject to these contracts being confirmed as acceptable to the bank. Although recent economic events have adversely affected the demand for property in WA, the extend [sic] of presales within the subject project and an anticipated 11 month selling period for the remaining 12 lots should secure the profitability of the project. We also note that the majority of presales are based on significant individual investments in the original land acquisition syndicate. We have attached a revised “Gross Realisation” assessment which takes into account the additional presale. Having revisited the site and reviewed the original valuation assessment we are of the opinion that the market valuation assessments within our original report are unchanged as at 30 October 2008. We point out, however that the original assessment was undertaken on the assumption that all purchasers would include the plunge pool option in the contracts. We recommend that adjustments be made to the “As if Complete” assessments if purchase contracts are found to vary from this assumption. The original valuation was undertaken in accordance with the Draft Strata Plan and Condition 28 of the letter of Planning Consent (Shire of Busselton) whereby the proposed Foreshore Reserve is Vested in the Crown and ceded free of costs. We confirm that no value has been attributed to the Foreshore Reserve of 1,688m2 in our valuation assessment. We trust this advice is sufficient for your requirements and advise that this letter is subject to the Assumptions, Conditions and Limitations contained in our original report. This advice should be read in conjunction with our original report. We confirm that [the Bank] can rely on this advice for mortgage security purposes. This valuation is current as at the date of valuation only. The value assessed herein may change significantly and unexpectedly over a relatively short period (including as a result of general market movements or factors specific to the particular property). We do not accept liability for losses arising from such subsequent changes in value or market conditions. Without limiting the generality of the above comment, we do not assume any responsibility or accept any liability where this valuation is relied upon after the expiration of 3 months from the date of valuation, or such earlier date if you become aware of any factors that have any effect on the valuation. Yours faithfully BLAKE SMITH A.A.P.I DIRECTOR, EGAN NATIONAL VALUERS (WA) CERTIFIED PRACTISING VALUER LICENSED VALUER No. 530 FOR THE STATE OF WESTERN AUSTRALIA Appendices St George Bank Request Revised “Gross Realisation” Schedule Revised Price List Photographs |

46 These communications on 3 and 4 November 2008 are, to use the expression of Senior Counsel for the appellants, the ‘culmination’ or final point of the dealings between Egan Valuers (through Mr Smith) and the Bank (through Ms Gilbey), being the point at which the Bank made it explicit that it knew about the investor presales being non-arm’s length dealings but, in that context, made a direct enquiry of Egan Valuers as to the valuation provided and asked, in terms: can the Bank rely? The response of Egan Valuers stated that the Bank could rely. Indeed, on appeal, the contention advanced was that the conclusions of the primary judge that the Valuations were rendered inoperative or did not become operative because of the Presales Qualifications cannot be reconciled with this final exchange, expressly confirming, following direct enquiry, the suitability of reliance upon the Later Valuation for the purposes of mortgage security.

C.5 Conclusions as to the Conduct of Egan Valuers and Mr Smith

47 Reference was made in [33] above to the key passages of his Honour’s judgment where he characterised the conduct of Egan Valuers and Mr Smith. Read literally, it might be thought that these passages elide two matters which are separate: the analysis of assessing whether conduct is misleading or deceptive (a question of fact objectively determined: see Campbell at 341-342 per Gummow, Hayne, Heydon and Kiefel JJ), with the distinct issue of causation which, in many cases, is determined by reference to answering whether individual reliance is established. The appellants made a similar point by submitting that the primary judge conflated two questions: (a) what did the valuations communicate to the Bank; with, (b) what use did the Bank make of the valuations?

48 Read fairly, however, no such error is evident. The primary judge, in this part of his reasons, was making clear that there was no subjective evidence of the Bank to detract from the conclusion otherwise available that the Bank knew the true position involving the Syndicate (a contextual matter relevant to the assessment of the relevant conduct). On the question of characterisation (as distinct from reliance), his Honour was also making the point that no evidence was called from the recipient on the question of fact as to whether particular conduct was misleading or deceptive. Although it is true that the characterisation of conduct as misleading or deceptive is objective, it is uncontroversial that subjective evidence that an erroneous conclusion was formed is admissible and may be persuasive in establishing that the conduct was misleading or likely to mislead, as may evidence of acts or omissions resulting from erroneous belief: see Global Sportsman Pty Ltd v Mirror Newspapers Ltd (1984) 2 FCR 82 at 87 per Bowen CJ, Lockhart and Fitzgerald JJ. The primary judge was noting that this type of evidence from a Bank officer was not adduced.

49 More generally, no error is demonstrated in the primary judge’s conclusion that the “As if Complete” value was a statement of opinion which was expressed as being held on the basis of the assumptions and subject to the qualifications set out in the Valuations. One such assumption was that there were presales as set out in the “Gross Realisation ‘As if complete’” table. The statement of opinion as to value conveyed that the opinion was held on the basis of certain express assumptions and qualifications. Read as a whole, what Egan Valuers and Mr Smith were communicating was that the Bank ought to satisfy itself as to the correctness of the assumptions. Given it was expressly stated that the presale contracts had not been sighted, viewed as a whole and contextually, a communication to the recipient was being made that the opinion as to value may be unreliable unless the presale contracts were verified or were authentic.

50 This is what the primary judge meant in concluding that the qualification and disclaimer in clauses 12 and 13 of the First Valuation (see [35] above), which were incorporated into and repeated in the Later Valuation (see [45] above), had the result that the Valuations (which standing alone may have been misleading) could not be characterised as such when the full context of the communication and surrounding circumstances were taken into account.

51 The important circumstances that his Honour correctly took into account have been referred to in Section C.1 above, but two contextual matters which support the primary judge’s characterisation of what was communicated merit emphasising here: first, the fact that the Bank can be taken to be a financially literate and commercially sophisticated recipient of property valuation services; and secondly, given the findings as to the Bank’s knowledge, the terms of the Valuations which were made subject to the Presales Qualifications were inconsistent with what the Bank knew was the true state of affairs in the sense that, as his Honour found at [229], it was “obvious Mr Smith believed [the presale contracts] existed and his valuations had been given on this basis”. The Bank, given the unchallenged findings of the primary judge, must be taken as knowing that no such contracts existed.

52 The conclusion of the primary judge rested on the basis that the Presales Qualifications or assumption had been conveyed and that the statement of opinion in the Valuations must be assessed in this context. Given the need to have regard to all the relevant circumstances, it would be erroneous to characterise the Valuations as conveying an opinion as to value divorced from the qualifications to that opinion and the assumptions upon which it was based. Correctly, the primary judge was cognisant that not only is the assessment of the impugned conduct determined by reference to all the relevant surrounding facts and circumstances but that it invites error to look simply at isolated parts of the conduct (such as the fact of the representation as to value of a particular amount on a particular basis): see Campbell at 341-342, Butcher at 625 [109], and [29] above.

53 With different assumptions, it seems obvious that the expression of opinion as to value would change. Indeed, perhaps surprisingly, no expert opinion evidence was adduced considering the counterfactual where the presale contracts existed, as Mr Smith assumed. Mr Smith gave evidence in cross-examination that the Valuations were unaffected by the existence of the presales and hence these made no difference to his valuations, but this evidence was rejected by the primary judge (see [219]-[221]) and no party to the appeal suggested that his Honour’s approach in this regard was otherwise than correct. Senior Counsel for the appellants accepted that, on the state of the evidence, the question as to whether the Valuations would have been incorrect in this counterfactual was impossible to answer (T 21-2).

54 No error has been shown in how the primary judge dealt with the way the case was pleaded and presented below. This is not, however, the end of the matter. As noted above, the case on appeal was directed to the terms of the Later Valuation and the dealings immediately prior to it being provided to the Bank. More particularly, the case on appeal was directed to the fact that the Later Valuation was sent following an express request to confirm the Later Valuation “for the purposes of mortgage security” and notwithstanding the non-arm’s length nature of 25 of the presales.

55 This case was not dealt with, in terms, by the primary judge, but this is hardly surprising given the way the case was presented below. Notably, as is clear from the relevant parts of the SOC (extracted at [34] of the primary judge’s reasons), there was no express pleading that Egan Valuers and Mr Smith engaged in misleading or deceptive conduct because in the context of a specific query from the Bank, they represented on 4 November 2008 that the Later Valuation was accurate, reasonably based and could be used for the purposes of mortgage security, notwithstanding the fact that 25 presales were not arm’s length sales. The attempt was made to ‘shoehorn’ this case on appeal into the only impugned representation made by Egan Valuers and Mr Smith pressed on appeal: that they represented to the Bank that the “As If Complete” value of the Resort as at the time of the Valuations was $69,856,500, but that the value was “substantially less than that”: see SOC [40(f)], [41(g)].

56 It hardly needs to be stated that although this appeal is in the nature of a rehearing (Minister for Immigration and Multicultural Affairs v Jia Legeng [2001] HCA 17; (2001) 205 CLR 507 at 533 [75] per Gleeson CJ and Gummow J), the task of the Court on such an appeal is the correction of error: CDJ v VAJ [1998] HCA 67; (1999) 197 CLR 172 at 201-202 [111] per McHugh, Gummow and Callinan JJ. One cannot identify error in the primary judge’s reasoning in circumstances where the much more refined case on appeal was not the way the case was pleaded in the SOC and presented below. For whatever reason, a misleading and deceptive conduct case was not pleaded that Egan Valuers and Mr Smith represented on 4 November 2008 that the Later Valuation was accurate, reasonably based and could be used for the purposes of mortgage security (and that this representation was falsified because it could not be used for the purposes of mortgage security).

57 Despite this, even if we are incorrect and it was thought that the case on appeal was open to be run on the pleading, despite having some attraction, the refined argument ultimately fails for the same reasons identified by the primary judge in rejecting the case as run below. What was communicated by Egan Valuers and Mr Smith was an opinion but it was an opinion based on the Presales Qualifications and all the other assumptions and qualifications that came with it. The representation that the Bank could rely on the Later Valuation for “mortgage security purposes” must be assessed in a way that is not divorced from what the whole communication conveyed, including the Later Valuation’s qualifications and the bolded recommendation that the Bank obtain copies of the presale contracts to confirm their authenticity “as liability for our valuations is extended subject to these contracts being confirmed as acceptable to the [Bank]”.

58 Although this communication was made after the Bank had made reference to the fact that the presales to investors were not at arm’s length, his Honour referred, at [77]-[78], to Mr Smith’s evidence that the Bank’s advice to him that the investors’ transactions were not arm’s length did not affect the substance of the Later Valuation, but Mr Smith remained concerned to ensure the contracts existed, and left it to the Bank to be so satisfied. Mr Smith also said (and the primary judge accepted) that he used bold type when making the Presales Qualifications in the Later Valuation as this particular aspect of the communication was a matter of importance and he wanted to ensure the Bank understood that he had not sighted any of the presale contracts.

59 The primary judge’s conclusions that the Valuations and, in particular, the Later Valuation, was not misleading and deceptive has not been shown to be erroneous. Having rejected Ground 1 (that the primary judge erred in failing to find that Egan Valuers and Mr Smith engaged in misleading or deceptive conduct), this conclusion is not only dispositive of the case against those respondents, but also the misleading or deceptive conduct case against the Directors (as narrowed on appeal). Despite that, in deference to the other arguments advanced by the appellants, we will deal with them.

D THE BANK AND RELIANCE

D.1 A Preliminary Matter: Reliance and Causation

60 As noted above, the causation case against Egan Valuers and Mr Smith, put in its simplest terms, was that:

(a) Egan Valuers and Mr Smith engaged in contravening conduct by providing misleading Valuations;

(b) the misleading Valuations (or at least the Later Valuation) were relied upon by the Bank to advance the Facility;

(c) the provision of the Facility allowed the Resort development to proceed;

(d) as a consequence of the Resort development proceeding, the investors, including the appellants, suffered loss and damage.

61 Hence the causal pathway for the appellants is dependent upon the reliance of the Bank on conduct properly characterised and then found to be misleading. This ‘indirect’ reliance (that is, through a third party) is the way the essential question of causation is addressed: Campbell at 351-352 [143] per Gummow, Hayne, Heydon and Kiefel JJ. The causation case is none the worse for this. It is well established that s 82 of the TPA provides a statutory cause of action for compensation to a person who suffers loss or damage by contravening conduct and does not stipulate any particular manner in which the loss or damage must be suffered. In Janssen-Cilag Pty Ltd v Pfizer Pty Ltd (1992) 37 FCR 526, Lockhart J held that there is no requirement that damages can be recovered only where the applicants rely directly upon the contravening conduct. A further illustration of the same point, in a scenario not entirely dissimilar to the present, can be seen in Australian Breeders Co-operative Society Ltd v Jones (1997) 150 ALR 488 at 529-530, where the Full Court (Wilcox, Lee and Lindgren JJ) found causation was established where, but for a misleading valuation, a third party would not have completed a transaction, with the consequence that the applicant investors would not have made the investments which occasioned their claimed loss.

62 Given that third party reliance by the Bank is a necessary element in their causation case, the primary judge’s finding that such reliance was not established was a further finding fatal to the claim of the appellants. Before assessing this finding, it is important to stress a subtle but important point: as was made clear at [30] above, the initial step for the primary judge was to identify precisely what representations the Valuations, being statements of opinion, entailed, that is, to identify the conduct to be characterised: see Campbell at 321 [32]-[33] per French CJ. In rejecting the allegation that the impugned conduct should be stigmatised as misleading and deceptive, the primary judge characterised the opinions as to value as being subject to the Presales Qualifications (being the advice “that the Bank needed to satisfy itself as to the existence of the relevant presale contracts”: at [234] and [293]). The topic to which we now turn is not whether the Bank relied on the conduct as the primary judge characterised it (an expression of opinion, subject relevantly to the Presales Qualifications) but rather, whether the Bank factually relied, in a material way, on a pleaded representation that the “As If Complete” value of the Resort, as at the time of the Valuations, was $69,856,500.

D.2 The Finding as to a Want of Reliance and the Evidence

63 In finding that the appellants did not establish that the Bank relied on the representations as to value (see [232]), the primary judge made a number of references to the fact that no Bank officers had been called or to a lack of evidence as to reliance: see [233], [235] and [349].

64 Although no Bank officers were called by any party, contemporaneous documents, being the internal business records of the Bank which detailed the Bank’s ratiocinations and decision-making in considering and approving the Facility, were in evidence.

65 These contemporaneous documents were admissible because those documents contained representations which, if accepted as reflecting the Bank’s decision-making, could rationally affect (directly or indirectly) the assessment of the probability of the existence of a fact in issue, being the Bank’s reliance on the impugned conduct: see s 55 of the Evidence Act 1995 (Cth) (EA). The hearsay rule (see s 59 of the EA) did not apply to the documents (insofar as they contained representations) given the apparent acceptance of all parties (as they were admitted without objection) that the relevant business records were created by Bank officers who had, or might reasonably be supposed to have had, personal knowledge of the relevant representations: see s 69 of the EA.

66 Not only was no objection taken to admissibility, no application was made to limit the use to be made of the evidence. It is also notable, in circumstances where specific complaint is made by Egan Valuers and Mr Smith that the makers of representations were not called to give evidence, that no request was made in relation to the evidence of previous representations contained in documents, pursuant to s 167 of the EA, for the appellants to call, as witnesses, the Bank officers who made the previous representations relied upon. Of course, if a request of this type had been made and refused, an application could have been made (s 169(1) of the EA) that the representations relied upon in the business records to prove reliance should not have been admitted. Irrespective of the making of an anterior request, an application could have been made at the time of tender by the respondents for discretionary exclusion under s 135 of the EA, or limitations as to use of the representations under s 136 of the EA. The respondents took none of these steps and, as a consequence, the evidence admitted in the business records was admitted, and was admitted for all purposes.

D.3 Consideration of Evidence as to the Bank’s Reliance

67 As the appellants submitted, the documents in evidence demonstrate the way in which the Bank used and relied upon the representation as to value in the First Valuation in considering, and then giving, indicative approval to the Facility. No reference was made in the reasons of the primary judge to these documents (including the approval document of 16 September 2008 and the previous submission documents). The appellants also submitted, correctly, in relation to the Later Valuation, that the 10 November 2008 letter of offer and the internal bank drawdown documents demonstrate express reliance upon the existence of the representations as to value contained in the Valuations, in the sense that the fact of the representations as to value (at an acceptable level) were a material cause of the Bank deciding to lend and proceed with the Facility. Further reference is made to these documents at [83]-[84] below. What is apparent from the contemporaneous record makes intuitive sense: why were the Valuations obtained unless the representations as to value conveyed in them were to be relied upon by the Bank?

68 The submissions made on behalf of Egan Valuers and Mr Smith fall into the error of suggesting that the question of reliance dealt with by the primary judge was to be decided by reference to what evidence might possibly have been adduced by the appellants from Bank officers, rather than by an analysis of the evidence relevant to Bank reliance that was adduced.

69 Properly analysed, the only possible relevance of the fact that the appellants did not call a Bank witness was if: (a) there was some insufficiency in the evidence of reliance by the Bank on the representations as to value in the contemporaneous business records (which there was not); or (b) some sort of inference could be drawn, unfavourable to the appellants, by reason of the failure to call such a witness. This latter contention is unsustainable as the relevant witnesses were no more in the camp of the appellants than they were in the camp of any other party to the proceeding.

70 Leaving aside the issue of the characterisation of the impugned conduct which we have already addressed above, the relevant question to be addressed in this part of the case was: upon analysis of the admitted evidence and any inferences properly drawn from that evidence, was reliance by the Bank on the representations as to value in the Valuations proved in accordance with s 140(1) of the EA?

71 As French CJ, Gummow, Hayne, Crennan, Kiefel and Bell JJ explained in Australian Securities and Investments Commission v Hellicar [2012] HCA 17; (2012) 247 CLR 345 at 412 [165]-[166]:

Disputed questions of fact must be decided by a court according to the evidence that the parties adduce, not according to some speculation about what other evidence might possibly have been led. Principles governing the onus and standard of proof must faithfully be applied. And there are cases where demonstration that other evidence could have been, but was not, called may properly be taken to account in determining whether a party has proved its case to the requisite standard. But both the circumstances in which that may be done and the way in which the absence of evidence may be taken to account are confined by known and accepted principles...

Lord Mansfield's dictum in Blatch v Archer [(1774) 1 Cowp 63 at 65; 98 ER 969 at 970] that “[i]t is certainly a maxim that all evidence is to be weighed according to the proof which it was in the power of one side to have produced, and in the power of the other to have contradicted” is not to be understood as countenancing any departure from any of these rules…

(Emphasis in original)

72 Blatch v Archer has no work to do in the present circumstances. The business records of the Bank establish reliance by the Bank. Although we have not found error in his Honour’s identification and characterisation of what representations the statements of opinion made by Egan Valuers and Mr Smith entailed (and that they were relevantly subject to the Presales Qualifications), this is not to say that we agree with the primary judge that there was a failure by the appellants to adduce sufficient evidence to prove the fact in issue that the Bank relied upon the Valuations to the extent that they contained a representation that the “As If Complete” value of the Resort at material times was $69,856,500.

E ADDITIONAL ISSUES AS TO CAUSATION

73 Proof of Bank reliance is not, however, to be confused with proving causally related loss. Although proof of reliance was necessary, it was not sufficient. The argument of the appellants proceeded, in effect, on the basis that if Bank reliance was proved, so was causation, contending that but for the contravening conduct “[t]he Resort would not have been built because funding would not have been obtained to enable that to occur. That is not speculative, but is the only reasonable inference”.

74 As the primary judge explained (at [386]), the case below was that the appellants lost the chance of selling the Resort land in circumstances where the Resort never would have been developed (some additional costs were also claimed in relation to the recovery of legal costs and part of this claim is dealt with separately below). Sale of the Resort land was the only option if appropriate finance terms were not obtained, and such terms could never have been obtained if a ‘correct’ Resort valuation of $45.5 million had been proffered in the counterfactual. Although the appellants were not the owners of the Resort land, as the primary judge recorded at [389]-[390], the case below was that, if necessary, the investors would have called a Syndicate meeting and would have obtained the requisite 75% vote (mandated by the Joint Venture Agreement) in order to obtain a sale of the Resort land.

75 In rejecting this case, his Honour found as follows:

(a) the evidence led by the appellants below did not put the Court in a position to value the lost chance (in accordance with the principles explained in Sellars v Adelaide Petroleum NL (1994) 179 CLR 332) (see [411]);

(b) there was “insufficient evidence” to conclude whether the Bank would have granted finance or as to what “commercially would have happened” with the Bank in the counterfactual (see [417]);

(c) there was a failure to lead evidence of the value of the Resort land as at the date that it was alleged it would have been sold and as to how long it would have taken to sell it (see [411] and [414]);

(d) there was uncertainty around what decisions would have been made if the future of the Resort project had been put to investors for a vote (including as to possible attempts to obtain alternative finance or to advance a redesign of the project) (see [409] and [414]); and

(e) there was uncertainty as to how long the process of consideration of alternative options would have taken and uncertainty as to the Syndicate costs that would have been properly incurred in the relevant counterfactual (see [409] and [414]).

76 More specifically, at paragraph [417]-[418] his Honour noted:

[T]he Court cannot easily infer that, if the alleged misleading and deceptive conduct had not occurred, the Bank would simply not have granted the finance. The possibilities of further valuation assessments by the Bank, negotiation over finance, including as to the scale of the development, would all have been in play and there is insufficient evidence, to my mind, for the Court to decide what then commercially would have happened. While it is one thing for the Court to be referred to the indicative terms proposed by the various banks, to which the applicants made reference, those proposals of finance were limited to the express propositions put to those banks for financing.

Further, I do not consider the evidence allows me to conclude, having regard to the reasonably complex terms of the joint venture agreements, that the requisite percentage of 75% or more of all the syndicate members would have voted to adopt the default position and thereby have caused the land to be sold. That was an option, but I do not consider it appropriate to say, on the Sellars approach, that that chance was realistically lost. There is insufficient evidence to indicate that there was a real chance that the default position would have been obtained, contrary to the submissions of the applicants in that regard. The point is that the default position was not at the election of the six applicants, but was at the election of at least 75% of the 23 syndicate members. To know whether that chance was lost, the Court would need to be apprised of much more evidence than it has received concerning the position that the syndicate members more generally might have adopted. The Court does not feel confident in coming to a view about that, including by making a generous inference. The position as to what might have happened within the syndicate but for the allegedly deceptive conduct is quite uncertain on the evidence led by the applicants.

77 On appeal, the submission of the appellants was that it was evident from the contemporaneous business records that, but for the representations as to value in the Valuations, it was a practical certainty that the Bank would not have provided the Facility. It was further asserted that it was entirely speculative, and contrary to the compelling inferences, for it to be suggested that the Resort would have been built on the basis of a correct, $45.5 million “As If Complete” valuation. Given the whole purpose was for the investors to obtain a villa in the Resort, if it had not been built, it was axiomatic that the Resort land would have been sold.

78 In response, Egan Valuers and the Bank supported the primary judge’s reasoning extracted at [76] above and stressed that this was not a simple loss of a chance case where the appellants owned the Resort land and could control it. What the appellants enjoyed was a bundle of rights as set out in the relevant Syndicate agreements that governed the joint venture and there was an insufficiency of evidence from which it could be inferred that in the counterfactual the investors would have immediately agreed to abandon the project and sell the Resort land without further careful, detailed consideration of other options.

79 It is plain from Sellars that a breach of s 52 of the TPA may give rise to an entitlement to statutory compensation under s 82 of the TPA for loss of a chance or opportunity, and that the loss of opportunity may constitute loss or damage for the purposes of s 82. It is also clear from Sellars and the many cases that have applied it, that in order for a claimant to recover damages for loss of opportunity, the claimant must prove, on the balance of probabilities, that the contravening conduct caused “the loss of a commercial opportunity which had some value (not being a negligible value)”, the value of that loss “being ascertained by reference to the degree of probabilities or possibilities”: see Sellars at 355 per Mason CJ, Dawson, Toohey and Gaudron JJ (original emphasis).

80 The primary judge’s reasoning that there were no damages proved had as its starting point the notion that there was an insufficiency of evidence to prove the Bank’s intentions and decision-making in relation to the Resort in the counterfactual. It seems clear that this factor weighed heavily in his Honour’s explicit conclusion at [417] that “the Court cannot easily infer that, if the alleged misleading and deceptive conduct had not occurred, the Bank would simply not have granted the finance”. This was allied to a finding (again at [417]) that there was “insufficient evidence” as to what the Bank would have done commercially in the counterfactual.

81 This conclusion seems to rest, at least in part, on the earlier criticism that there was a failure to adduce evidence from Bank officers. In circumstances where his Honour did not analyse the contemporaneous documentation of the Bank and consider what inferences were available to be drawn from that documentation, those available inferences were not assessed and, with respect to the primary judge, this caused the Sellars analysis to miscarry.

82 Although we express no final view, on an analysis of the contemporaneous documentary evidence that was adduced, it is arguable, contrary to his Honour’s findings, that the appellants had established, in the counterfactual, that there was no basis at all to think that the Bank would have granted finance, and there was sufficient evidence as to what the Bank would have done commercially (that is, not proceed).

83 For example, and without seeking to be exhaustive, the following can be drawn from the documents in evidence:

(a) the offer of the Facility was made subject to the explicit covenant that “[a]fter practical completion of the works at the Project, you must ensure that at all times the LVR (as determined by us) for the facility does not exceed 50%”; further, the Bank emphasised that the “Borrower must repay that portion of the total amount owing or alternatively provide additional security acceptable to us to ensure that the abovementioned ‘LVR’ and ‘LCR’ are maintained to our satisfaction at all times” (AB4271) (emphasis added);

(b) the Bank “Approved” LVR was 50% (AB4695);

(c) LVR less than 50% was described by the Bank as “strong” (AB2101 (incorrectly described as ‘LCR’ in this document), 3270, 3576); indeed, in its Property Investment Cam dated 15 August 2008 (AB3251-76), having considered the “As If Complete – fully constructed” value in the First Valuation, the Bank’s analysis was “Max static LCR does not exceed at 53.3%, on completion LVR 47.7%, and ROC is a sound 58.4%” and, under the heading “RECOMMENDATION” (original bolding), approval was recommended, including on the basis of these figures (AB3273);

(d) in the Advance Application, prepared by Ms Gilbey and recommended by Mr Pearce, the Bank explicitly noted in the terms of the “Other Conditions” that “You must ensure that at all times the LVR does not exceed 50%” and that at all times the “LVR is to be acceptable to us determined under this Facility Offer” (AB3556-7);

(e) in the ‘Final Decision’ approval document (AB3577), the Bank referred to the “security property which will have a value of $67.785M on-completion” (emphasis added); that is, the Bank relied upon the valuation of the security in the First Valuation.

84 The apparent effect of these documents is that the Bank offered the Facility on the basis that the LVR would not exceed 50%, and that the Bank had satisfied itself that an LVR below 50% was confirmed by the representations as to value in the Valuations. A change in the valuation integer (to what his Honour found would have been the correct figure) is of such proportions as to have a dramatic impact on the LVR. Taken as a percentage of $45.5 million, the Facility offered by the Bank (of $32.3 million) would have amounted to an LVR of 71% in rounded figures. When this is appreciated, the suggestion that there was simply no evidentiary basis for concluding the Bank would have declined to proceed is, with respect, difficult to sustain.

85 Although his Honour also found that other finance alternatives may have been open to the investors, and accepted the respondents’ submissions as to uncertainty around voting and decision-making by investors, it is a challenge to conceive any realistic scenario, in the absence of a valuation that suggested that the development was viable, other than the Resort land being sold. Moreover, it is arguable, if it was accepted that the contemporaneous business records demonstrate that the Bank would not have touched the Resort development if it had been valued at $45.5 million, that other potential financiers would have reached a similar conclusion. If this is correct, it is arguable the appellants lost some value (not being a negligible value) of a chance to sell the Resort land and minimise their losses.