FEDERAL COURT OF AUSTRALIA

Crescent Funds Management (Aust) Ltd v Crescent Capital Partners Management Pty Limited [2017] FCAFC 2

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The appeal in NSD 517 of 2016 be dismissed.

2. The appellants in NSD 517 of 2016 pay the respondents’ costs of and incidental to that appeal to be taxed if not agreed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

NSD 567 of 2016 | ||

| ||

BETWEEN: | CRESCENT CAPITAL PARTNERS MANAGEMENT PTY LIMITED (ACN 108 571 820) First Cross-Appellant CRESCENT CAPITAL PARTNERS LTD (ACN 094 040 874) Second Cross-Appellant | |

AND: | CRESCENT FUNDS MANAGEMENT (AUST) LTD (ACN 144 560 172) First Cross-Respondent CRESCENT INVESTMENTS AUSTRALASIA PTY LTD (ACN 141 570 952) Second Cross-Respondent TALAL YASSINE | |

JUDGES: | GREENWOOD, EDELMAN AND MARKOVIC JJ |

DATE OF ORDER: | 12 january 2017 |

THE COURT ORDERS THAT:

1. The orders of the primary judge made on 23 March 2016 be varied to add an additional order, order 4(h), that by 10 February 2017 the parties have liberty to apply to a single judge of the Federal Court for orders by consent to vary the terms of orders 4(f) and 4(g).

2. The appeal in NSD 567 of 2016 otherwise be dismissed.

3. The appellants in NSD 567 of 2016 pay the respondents’ costs of and incidental to that appeal to be taxed if not agreed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

GREENWOOD J:

Introduction

1 In these proceedings the nine appellant entities and the tenth appellant, Mr Talal Yassine (as to Appeal NSD 517 of 2016), were the respondents in proceedings before the primary judge (Bennett J) in which the present respondents, Crescent Capital Partners Management Pty Limited (“CCPM”) and Crescent Capital Partners Ltd (“CCPL”) (described, together, by the primary judge as “Crescent Capital”), contended that the appellant entities engaged in misleading or deceptive conduct by using names, as part of their corporate titles, such as Crescent Funds Management, Crescent Investments, Crescent Consolidated, Crescent Financial, Crescent Foundation, Crescent Holdings and Crescent Super (described, together, by the primary judge as “Crescent Wealth”) in the provision of financial services and products with the result that the appellants had made representations, in trade or commerce, that they or their services and products were in some way connected with Crescent Capital and the services and products offered by Crescent Capital.

2 Crescent Capital also contended before the primary judge that the first and second appellants had engaged in misleading or deceptive conduct by using the mark “CRESCENT WEALTH” and “Crescent” and “Fund” names Crescent Wealth Superannuation Fund, Crescent Australian Equity Fund, Crescent Wealth International Equity Fund, Crescent Diversified Property Fund and Crescent Islamic Cash Management Fund as badges of identification and by using particular domain names.

3 The conduct was said to engage contraventions of ss 18 and 29 of the Australian Consumer Law (the “ACL”) contained in Schedule 2 to the Competition and Consumer Act 2010 (Cth) and ss 12DA and 12DB of the Australian Securities and Investments Commission Act 2001 (Cth) (the “ASIC Act”).

4 The primary judge notes that Crescent Capital abandoned its primary claims against Crescent Institute Limited (which is now the eighth appellant and was the eighth respondent before Bennett J): primary judge (“PJ”) at [2]; Crescent Capital Partners Management Pty Limited v Crescent Funds Management (Aust) Limited [2016] FCA 229.

5 In the principal proceedings, Crescent Capital contended that all of the (then) respondents and, in particular, Yassine Corporation Pty Ltd and Mr Yassine were accessories in the conduct contraventions of each of the other respondents (as persons involved in the contraventions for the purposes of s 12GF of the ASIC Act) and thus liable to remedial orders in favour of Crescent Capital.

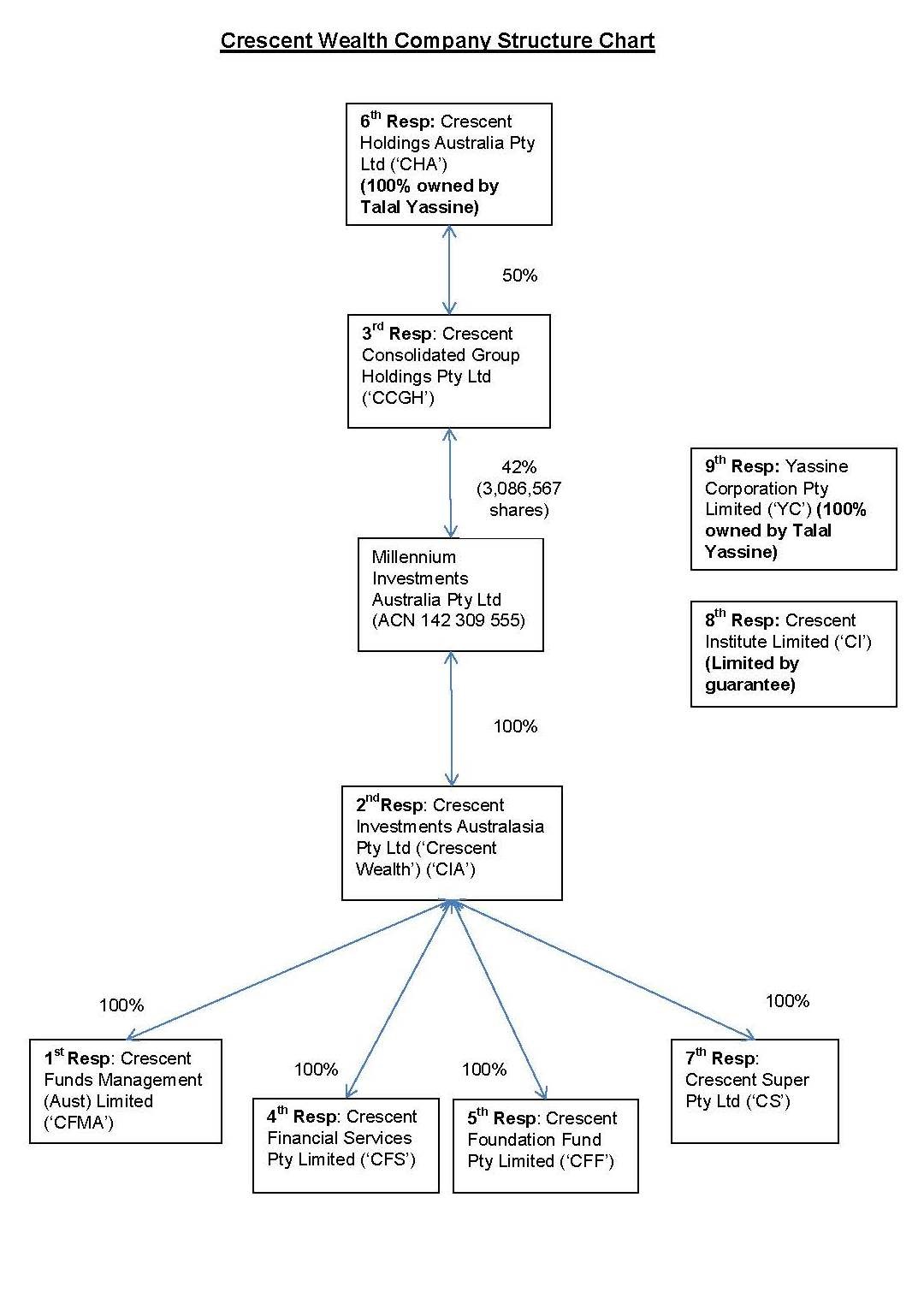

6 The Crescent Wealth entities contended that upon proper analysis the scope, focus and character of their activities were so differentiated from those of Crescent Capital that no likelihood arose of anyone being led into error by Crescent Wealth’s use of the company titles incorporating the words or names described at [1] of these reasons or the titles for Crescent Wealth’s four funds ([2] of these reasons) or by use of the mark “CRESCENT WEALTH” or “Crescent”.

7 All of the respondents before the primary judge are appellants in the present proceedings. It is necessary to say something, contextually, about the structure of the Crescent Wealth group of companies and their relationship one to the other. The primary judge described that matter at [73], [74] and [77] of her Honour’s reasons. In the diagram at [73] of her Honour’s reasons, the reference to “first respondent” and “second respondent” and so on, corresponds to first appellant and second appellant and so on in these proceedings (apart from Mr Yassine who is the tenth appellant in these proceedings). At [73], the primary judge set out the following diagram:

8 At [74] and [77], the primary judge notes these matters:

[74] It is agreed that there is no relevant distinction, for present purposes, between the first and second respondents. The parties were agreed that the first and second respondents could be treated as a single entity. The second respondent is the operating company of the Crescent Wealth business, while the first respondent is the responsible entity for that business. The business of Crescent Wealth was established in about 2010 by Mr Yassine, together with Mr Dandan and Mr Eid, although it only began trading under that name in around August 2011.

[emphasis added]

…

[77] The following facts seem to be agreed:

• The first respondent (CFMA) is the responsible entity that makes offers in Crescent Wealth funds to investors.

• The second respondent (CIA) is the operating company.

• The third and sixth respondents are holding companies and are, in effect, dormant. They do not engage in offers or supplies to investors. They are non-operating holding entities through which the founders of Crescent Wealth invested in Crescent Wealth. The third respondent has not been used to make any subsequent investments; does not offer, and has not offered, investment products or services to the public; and has not marketed itself to investors or potential investors. Accordingly, the third respondent has not engaged in any conduct directed at relevant members of the class of consumers, nor has it made any representations that could mislead or deceive such consumers.

• The fourth and seventh respondents are wholly owned by CIA. They are dormant and do not engage in any conduct, let alone the relevant conduct. They do not undertake any activities or hold any assets.

• The fifth respondent is a wholly owned, not-for-profit entity which makes charitable donations that serve to “cleanse” investments made through CFMA and CIA that do not comply with Sharia law, so as to ensure ongoing Sharia compliance; moneys are given through the Foundation to charity. The Foundation does not offer investment products or services to the public and plays no role in determining which funds are provided to it, nor does it have any control over the amount of funds distributed to it.

• The eighth respondent, the Crescent Institute, is, in effect, a networking group. It is the corporate incarnation of a networking group founded in the 1990s by Mr Yassine under the name “The Crescent Club”, while he was at University. It holds thought leadership and networking events on topics of interest to those of the Muslim faith and others in business and the wider community. Crescent Capital does not now seek any orders in respect of this party.

• The ninth respondent is a corporate vehicle for investments by the Yassine family.

• Mr Yassine is the tenth respondent. He is the co-founder and managing director of Crescent Wealth and the founder and now patron of the Crescent Institute.

The Declarations

9 In the result, the primary judge made the following declarations:

1. The First and Second Respondents [Crescent Funds Management (Aust) Limited and Crescent Investments Australasia Pty Ltd] have, by offering to provide, providing, advertising and marketing investment services and products, in Australia, in trade or commerce under and by reference to:

(a) the name and mark “CRESCENT WEALTH”;

(b) the corporate names Crescent Funds Management (Aust) Limited and Crescent Investments Australasia Pty Ltd;

(c) the fund names Crescent Wealth Superannuation Fund, Crescent Australian Equity Fund, Crescent International Equity Fund, Crescent Diversified Property Fund and Crescent Islamic Cash Management Fund; and

(d) the domain names crescentinvestments.com.au, crescentwealth.com.au, crescentfunds.com.au and crescentfunds.net.

engaged in conduct that was misleading or likely to mislead or deceive in contravention of s 12DA of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act).

2. The Tenth Respondent was knowingly involved in the conduct of each of the First and Second Respondents in contravention of s 12DA of the ASIC Act, identified in Order 1.

The Orders

10 The primary judge made the following order in relation to Crescent Wealth’s use of the titles of the first and second appellants, use of the names for the Funds using the word Crescent and use of the domain names:

3. The First and Second Respondents, by themselves, their servants or agents, be restrained from, in trade or commerce, offering to provide, providing, advertising or marketing in Australia any investment services or products under and by reference to:

(a) Crescent Funds Management (Aust) Limited;

(b) Crescent Investments Australasia Pty Ltd;

(c) any of the following names:

(i) Crescent Australian Equity Fund;

(ii) Crescent Diversified Property Fund;

(iii) Crescent Islamic Cash Management Fund;

(d) any of the following domain names:

(i) crescentinvestments.com.au;

(ii) crescentfunds.com.au; and

(iii) crescentfunds.net;

or any name substantially identical with the names in (a)-(d).

11 The primary judge made the following order concerning use of the term or mark “CRESCENT WEALTH”, qualified in the way set out at sub-paras (f) and (g) of Order 4:

4. The First and Second Respondents, by themselves, their servants or agents, be restrained from, in trade or commerce, offering to provide, providing, advertising or marketing in Australia any investment services or products under and by reference to:

(a) CRESCENT WEALTH;

(b) Crescent Wealth Superannuation Fund;

(c) Crescent Wealth International Equity Fund;

(d) the CRESCENT WEALTH business name;

(d) the domain name crescentwealth.com.au;

or any name substantially identical with the names in (a)-(e) without:

(f) including the Respondents’ logo and stating clearly and prominently, and reasonably proximately (eg not by way of footnoted text) to where any such name appears, including in any webpage, product disclosure statement, or advertising or promotional materials:

“Neither [CRESCENT WEALTH] nor any of its products is associated or affiliated with Crescent Capital Partners”,

and, in the case of a radio commercial, television, video advertisement, or promotional appearance also stating the same by way of a clear and prominent spoken statement of at least 6 seconds; or

(g) otherwise clearly distinguishing its business from the business carried on by the Applicants under the name Crescent Capital Partners.

The respondents’ challenge to Orders 3 and 4

12 The present respondents contend that the primary judge fell into error in framing Orders 3 and 4 because, first, having found that use of the mark “CRESCENT WEALTH” and the name “Crescent” in conjunction with words such as “investments” and “funds” was misleading or likely to mislead or deceive (the relevant cohort of consumers), the injunctions ought to have restrained any use of the terms “CRESCENT WEALTH” and/or “Crescent” in connection with investment services or products of Crescent Wealth (or any name “substantially identical” or “deceptively similar” to either of those names), not just the particular titles, fund names or domain names and second, the restraint in Order 4 ought to have been unqualified rather than, in effect, enabling use in conjunction with the notice or disclaimer, as framed.

13 The primary judge also made a series of consequential orders. It is not necessary to set out those orders in these reasons.

The findings of the primary judge and related documents and evidence

14 It is now necessary to address the findings of the primary judge before turning to the grounds of appeal. In doing so, I will also make reference to some of the documents in the Appeal Book (“AB”) to which the Court was taken in the context of the primary judge’s findings which are said to be explanatory of those findings.

15 CCPM, the present first respondent, has held a licence to provide financial advice, products and services since 24 November 2000 and CCPL, the present second respondent, has since 27 July 2004 been an authorised representative of CCPM. CCPM has, since November 2000, operated a business of managing “private equity funds”. CCPM selected the word “Crescent” because it derives from the Latin word “Cresco” which means to grow, expand or increase: PJ at [7]. Until September 2010, the Crescent Capital entities used a logo featuring a crescent shape and the words “CRESCENT CAPITAL PARTNERS”. Since then, the badge of identification has consisted of simply those words with bold emphasis given to “Crescent” as follows: PJ at [30]:

CrescentCapitalPartners

16 These words, in this form, have been used on invoices, stationery, promotional and marketing material: PJ at [7]. Since 28 November 2000, Crescent Capital has operated a website with the domain name crescentcap.com.au.

17 At [9], the primary judge said this as to Crescent Capital’s reputation:

Crescent Capital has established, and there is no real dispute, that as at and since the commencement of Crescent Wealth’s activities in 2010, it had and has a reputation and goodwill in the financial services and financial management industry in the name Crescent Capital, and is often referred to as Crescent. That reputation derives from its own activities, from its approaches to investors and financial advisors, as the recipient of awards and from its activities in raising money for investment in its funds (which include the use of promotional and marketing materials), as well as from media reports.

[emphasis added]

18 As the above words in italics emphasise, Crescent Capital’s reputation in the name “Crescent Capital” (often referred to simply as “Crescent Capital”) subsists “in the financial services and financial management industry” and is a reputation found “among the financial community” (PJ at [11]) as a “successful private equity fund manager” (PJ at [11]), for which it has won awards from the Australian Private Equity and Venture Capital Association Limited (for management buyouts in 2003 and 2014): PJ at [10]. The primary judge notes at [12] that Crescent Capital describes itself in the following way:

Crescent Capital operates a private equity funds management business. It raises money from investors and uses these funds either to invest directly into a business or to acquire the business and typically holds its investment for three to six years with the aim of improving and growing the underlying business, before selling it and returning the proceeds to investors (after Crescent Capital’s fees are paid). Crescent Capital raises money in a series of pools, called “funds”, and approaches new and existing investors and offers the opportunity to invest in (also called “subscribe to”) the new fund.

[emphasis added]

19 Crescent Capital raises money from investors to establish or constitute “funds”. Its first fund was raised from both “retail clients” and “wholesale clients”. The appellants say, as they did before the primary judge, that this distinction is significant in determining whether there is any likelihood of confusion (amongst the relevant consumer cohort) between the products or services provided by Crescent Capital and those of Crescent Wealth or confusion as to any relationship or association between the Crescent Capital entities and, particularly, the first and second appellants. The parties seem to agree that the formulation adopted by the primary judge of the factors that determine whether a person is a retail client or a wholesale client is correct for the purposes of these proceedings.

20 That being so, a client (investor) is a “wholesale client (investor)” where: the price of the financial product, or the value of the financial product to which the financial service relates equals or is greater than $500,000; or the financial product or service is acquired by a person who has previously provided a certificate from a qualified accountant stating that the acquirer has net assets of at least $2.5 million or a gross income for each of the last two financial years of at least $250,000; or the person is a professional investor. A “retail client (investor)” is a person who is not a wholesale client (investor): PJ at [14] and [15].

21 The primary judge at [16] identifies the following features of Crescent Capital’s business and particularly the business of raising money to constitute funds:

Other matters relevant to the description of Crescent Capital’s business are, put shortly:

• A fund is closed once the monetary target is reached or when some pre-determined period of time elapses.

• There is then a call on committed funds from investors, as Crescent Capital identifies suitable investments over a ten year life of the fund, being a business identified as capable of generating the required rate of return on investment.

• Crescent Capital specialises in acquiring or investing in small to medium sized, privately owned businesses.

• The businesses which Crescent Capital targets are usually located in Australia and New Zealand, with enterprise values between AUD$50 and $300 million.

• Crescent Capital has also acquired smaller Australian and New Zealand based businesses to integrate into an existing larger business. Sometimes smaller businesses are acquired as part of a ‘roll-up’ or aggregation strategy; for example, there was evidence that Crescent Capital had engaged in such activity in respect of dental practices with individual values of as little as $1 million.

• The businesses are operated with a view to sale or listing on the stock exchange.

• The business model requires Crescent Capital to take control of a company or group in which it invests and to offer value-added services to companies in which it invests, such as providing strategic advice and introducing alliance networks.

22 As to the Crescent Capital funds raised over time the primary judge said this at [16]:

• The first fund (Crescent I) raised $25 million in 2001, the second (Crescent II) $100 million in 2004, the third (Crescent III) $400 million in 2007 and the fourth (Crescent IV) $490 million in 2012. There is a further fund, Crescent V, the amount raised is confidential, but it is substantial.

• Since 2004, funds have been raised exclusively from wholesale investors.

• Returns are through long term capital appreciation rather than through immediate and regular payments of principal and interest. Investors’ money, once committed, is tied up for the life of the fund, viz. ten years.

• It engages in fund raising every three to four years, approaching both new and existing investors.

• Crescent Capital does not advertise to the general public. It does operate a website, of which only part is publicly accessible.

• Crescent Capital is frequently referred to in the financial media by reference to its name, Crescent Capital Partners, or simply as Crescent.

[emphasis added]

23 As to the Crescent Capital funds, the position then, based on the findings at [16] is this:

Fund | Year Fund Raised | Amount | Ten Year Horizon | Source of Funds |

Crescent I | 2001 | $25 million | 2011 | Retail and wholesale clients |

Crescent II | 2004 | $100 million | 2014 | Wholesale clients only |

Crescent III | 2007 | $400 million | 2017 | Wholesale clients only |

Crescent IV | 2012 | $490 million | 2022 | Wholesale clients only |

Crescent V | 2015 | Confidential | 2025 | Wholesale clients only |

24 The majority of the investors in these Crescent Capital Funds are superannuation funds or institutional investors: PJ at [17].

25 The minimum investment amount for the 2004 Crescent II Fund was $250,000: PJ at [17]. The minimum investment amount for the Crescent IV Fund is described by the primary judge at [17] as “substantially higher than $250,000”. The average amount invested by each investor in the Crescent IV Fund was “extremely high”: PJ at [17]. These matters of the prevailing minimum investment threshold for each Crescent Capital Fund are put in this elliptical way by the primary judge due to the confidential nature of the private placement prospectus issued to clients. Participation in each Crescent Capital Fund after the 2001 Fund “has, in effect, been by invitation”: PJ at [17].

26 The appellants contend that in determining the “hypothetical representative” of the relevant consumer cohort so as to determine whether relevant consumers are being, or are likely to be, misled by Crescent Wealth’s use of “CRESCENT WEALTH” and “Crescent” (in combination with other words or not), the very substantial minimum investment threshold for participation in Crescent Capital’s private equity investment funds (and particularly the Crescent IV and Crescent V Funds with their corresponding institutional and highly sophisticated investors), means that such an investor is not properly regarded as a hypothetical representative of the relevant consumer class due to Crescent Wealth’s focus of concentrating on “investors seeking to invest in low risk/low return Sharia-compliant superannuation and related investment products in traditional assets classes (not including private equity)”.

27 The appellants say that the primary judge’s reference at [16] (the second dot point) to the “rate of return” for funds invested with Crescent Capital is a reference to: “High returns are targeted: 25% per annum (pre tax, pre fees) over the medium term”: Growth Fund Prospectus, 28 November 2000; “18% per annum (pre tax, post fees)”: Prospectus 27 June 2001; “Target IRR [Internal Rate of Return] 25% per annum (pre fees)”: Private Placement Memorandum, AB, Part C, Tab 9.2, pp 259 and 426. Mr Lyon-Mercado, Crescent Capital’s Chief Financial Officer and Finance Director, describes Crescent Capital’s rate of return as about “20% per annum after fees”: para 29, affidavit 17 October 2014.

28 The appellants emphasise that at [16] (the third dot point), the primary judge observes that Crescent Capital specialises in acquiring or investing in small to medium-sized privately owned businesses. The private equity business investment method is described by Mr Lyon-Mercado in these terms in his affidavit:

14 Once a fund is closed, Crescent begins to seek out suitable businesses to buy or in which to invest. A suitable business is a business that Crescent identifies as being capable of generating the required rate of return on investment. Crescent usually targets businesses located in Australia and New Zealand with enterprise values of between A$50 million and A$300 million. Crescent also often acquires smaller businesses to integrate into one of its existing larger businesses, or acquires them as part of a “roll-up” strategy whereby it aggregates a number of smaller businesses to corporatise into a larger business. These smaller businesses may have values of significantly less than A$50 million. For example, Crescent is at present buying and aggregating dental practices, some of which have a value of as little as A$1 million.

…

16 Crescent continues to buy and invest in businesses until the fund is approximately 80% spent. Crescent will then operate the businesses in which it has invested, sometimes for several years, and attempt to increase their profitability by measures such as providing additional capital for expansion, enhancing management expertise, improving business operations, and, in some cases, growing the business through acquisitions.

17 Eventually, Crescent aims to sell the businesses to trade or financial buyers or to list them on a stock exchange. If businesses are listed on a stock exchange, the stock is sold by investment banks to their institutional and retail clients. Crescent often retains a small interest in the listed entity. The money from the sale or listing of the businesses is then returned to the investors in the relevant fund, after management and performance fees are paid to Crescent.

[emphasis added]

29 At [18], the primary judge characterised investment in Crescent Capital’s funds in this way:

Investment in Crescent Capital’s funds can be characterised as high risk, high return investment and requires long term commitment of funds with no certainty of returns. Investors, including prospective investors, can be characterised as highly sophisticated investors who consider investments carefully before proceeding. Many of those investors use expert advisers and many are large institutions or high net worth individuals.

[emphasis added]

30 Crescent Capital’s Private Placement Memorandum of October 2010 explains the risks in these terms: AB, Part C, Tab 9.2, pp 157 and 213:

RISK

An investment in the Fund should be regarded as speculative and will involve significant risks, due to the nature of the investments the Fund intends to make.

The Fund is not a suitable investment for persons unable to sustain a loss of all or part of the sum invested or who require certain or predictable income flows. Investors should have the financial ability and willingness to accept the risks and lack of liquidity which are characteristic of the investments described in this Private Placement Memorandum, for the entire term of the Fund.

In particular, the attention of prospective investors is drawn to the risk factors set out in Section 10 of this Private Placement Memorandum.

10. RISK FACTORS AND CONFLICTS

RISK FACTORS

Investment in the Fund entails a high degree of risk and is suitable only for Wholesale Investors who understand fully, and are capable of assessing, the risks of a private equity fund of this nature.

The Manager does not guarantee any level of return to investors and the historic performance of investments managed by the Manager or associate companies cannot be taken as an indication of the future performance of Crescent IV.

Prospective investors should consider carefully the factors below (amongst others) in making their investment decision. These risk factors do not purport to be a complete explanation of the risks involved in investing in the Fund. Prospective investors must read the entire Private Placement Memorandum and Constituent Documents, and must consult their own professional advisors, before deciding to invest in the Fund.

[emphasis added]

31 In a report dated June 2001, van Eyk Research (engaged by Crescent Capital) reviewed the first of Crescent Capital’s Growth Funds. As to the risk profile and diversification benefits of investing in Crescent Capital’s Fund, the report says this at pp 4 and 10 (pp 690 and 696 of the AB respectively):

At p 4

• Because private equity is less liquid and offers less information it has higher total risk than publicly traded equity. At the same time, due to the appraisal based valuation method, private equity has lower market-related risk. Due to its diversification benefits private equity deserves a place in a balanced portfolio. The tax advantaged structure of the Fund makes Crescent Capital Partners Growth Fund an attractive investment for a range of investors such as: DIY, master funds or pooled superannuation investors, institutional funds and high net worth individuals.

• The Crescent Capital Growth Fund is a suitable investment for a sophisticated investor who is comfortable with the risks involved and constraints of this investment. If an investor decides to invest in this vehicle we would recommend an allocation of up to 5% for a balanced fund investor and up to 10% for a high growth investor.

At p 10

Role of Private Equity in diversified Portfolios

Due to the low market risk, it follows [that] the correlation between private equity and other asset classes over the longer term periods is relatively low too. This points to considerable diversification benefits of investing in private equity as the overall portfolio risk can be reduced substantially.

The chart below illustrates the relative positioning of private equity and venture capital using 10 years annualised figures for equities and bonds. For private equity and venture capital we assumed a long term return of 20% and 25% and a volatility of 20% and 25% respectively. These numbers are generally in line with historical figures and in our opinion reflects the inherent risks of this asset class. As can be seen from the chart private equity/venture capital is expected to provide higher returns relative to listed markets accompanied with slightly highly volatility (for private equity) and a significantly higher volatility for venture capital.

32 The chart referred to by van Eyk Research at p 10 is a graph showing the “Risk Return Spectrum” as between private equity and venture capital on the one hand and traditional asset classes on the other hand. The conclusions emerging from the graph are set out in the quote from the report above at p 10. As to the graph which shows that private equity/venture capital is expected to provide higher returns relative to listed markets (and slightly higher volatility for private equity), Mr Lyon-Mercado accepted in cross-examination, that it was common “in the financial services industry” to distinguish between private equity and venture capital investments on the one hand and traditional asset classes on the other hand and that private equity and venture capital investments are distinguished from traditional asset classes by reason of their “high risks and high return profile”. Mr Lyon-Mercado also accepted that those differences mean that a “rational investor” seeking high returns through investing in private equity would not see listed securities, for example (as one traditional asset class), as a substitute for a private equity investment: T, p 99, lns 5-18.

33 At p 20, the van Eyk Research report concludes in these terms:

Overall, we believe that exposure to the Crescent Capital Partners Growth Fund is suitable for a sophisticated investor who is comfortable with the risks involved and the constraints of this investment. Should an investor decide to invest in this fund we recommend an allocation up to 5% for a balanced fund investor and 10% for a high growth investor.

34 In the questions put to Mr Lyon-Mercado about the differentiation between private equity investments and investments in traditional asset classes, Mr Lyon-Mercado was asked about distinctions drawn by members of the “financial services industry” and distinctions drawn by a “rational investor”. The appellants contend that when Mr Lyon-Mercado drew or accepted these distinctions, he was speaking of distinctions drawn by persons who would be likely to be interested in investing in private equity. The appellants contend that the findings of the primary judge at [18] that Crescent Capital’s Funds can be characterised as high risk/high return private equity investments requiring long term commitment with no certainty of returns means that this class of investments is not substitutable for investments in traditional asset classes and that, as a class of investment, Crescent Capital’s sequence of Funds represent private equity investments made by “highly sophisticated investors” who “consider investments carefully” before making an investment (as the primary judge found at [18]). Moreover, they say that many of these highly sophisticated investors who are thinking carefully about their investments before making an investment (and whether they will invest in a Crescent Capital Growth Fund), call in aid “expert advisers”. Many of these investors are “large institutions” or “high net worth individuals”: PJ at [18].

35 As to the use of advisers, the appellants emphasise the evidence given before the primary judge by Mr Michael Lukin, the Managing Partner of ROC Partners Pty Ltd (“ROC”), an organisation engaged by private equity investors to provide advice about investments in private equity funds. Mr Lukin gave evidence before the primary judge that private equity investments made by clients of ROC (as one class of investors) made “substantial” private equity investments and the investments were “relatively risky” compared to other asset classes. Partly, no doubt, for that reason, private equity investors, he says, seek advice from private equity investment advisers before making such investments. Mr Lukin says that about half of the investors making private equity investments use such an adviser and where the investment falls into other asset classes such as listed securities or property, ROC’s clients consult other advisers: T, p 162, lns 22-45. As to the other 50% making private equity investments, Mr Lukin said this in evidence at T, p 163, lns 1-10:

Q: And the balance tend to be larger investors with resources to analyse potential private equity investments in-house before making them?

A: Yes, although there are cases of smaller investors that will kind of – you know, high net worth groups and family offices that will kind of make investments on their own behalf.

Q: And they, too, will tend to have in-house experts who advise them on those investments; correct?

A: Yes, or they will rely on their own expertise.

Q: Yes. And in your experience, as a rule, private equity investors take considerable care before making their investments; correct?

A: Yes.

36 As to Crescent Wealth’s business, it too is “concerned with the making of investments”: PJ at [19]. It offers “Sharia compliant superannuation” through the Crescent Wealth Superannuation Fund and “additional managed investment products to the public”. It is a “wealth management business”: PJ at [19] and [20]. Crescent Wealth ensures that its Sharia compliant financial products accord with the “highest international standards of Sharia compliance” and it promotes itself as investing in, and providing financial services in connection with, Sharia compliant services and products: PJ at [20] and [21]. However, its Australian Financial Services Licence is not limited to those services and products. The primary judge put it this way at [21]:

… [Crescent Wealth] is authorised to provide financial services to retail and wholesale clients of any, or no, faith, including high net worth individuals and financial planners. Crescent Wealth’s marketing is directed toward the public at large, with a particular emphasis on retail investors of the Islamic faith. It does have a significant institutional investment, of $1.5 million, from Aon Hewitt, an Australian superannuation fund.

[emphasis added]

37 By the end of 2014, Crescent Wealth had funds under management of $70 million and 3,000 members. The primary judge notes that by the end of 2015 funds under management were expected to be between $150 million and $200 million: PJ at [22]. Crescent Wealth offers investments in four managed funds: Crescent Australian Equity Fund, Crescent Wealth International Equity Fund, Crescent Diversified Property Fund and Crescent Islamic Cash Fund. These funds are managed by third party managers such as the “Bank of London and Middle East” and “HSBC Amanah”: PJ at [23].

38 At [23], the primary judge describes (and finds) the investment method bears these characteristics:

… The proportion of an investor’s superannuation contributions invested in each Crescent Wealth product depends on the investor’s choice between “growth”, “balanced” and “conservative” investment options. The products are designed for, and available to, retail investors. They are low risk and low return, especially when compared to the returns expected from Crescent Capital’s funds. Returns are distributed regularly and the superannuation product has no minimum investment requirement; the other managed investment products each have a minimum requirement for direct investment of $5,000, subject to a discretion to accept lower investment amounts. Funds can be withdrawn by an investor at any time.

[emphasis added]

39 As to the emphasis that Crescent Wealth places upon the Sharia compliant financial products (and services) it offers, the primary judge observes at [24] that funds controlled by Crescent Wealth are not invested in entities that engage in “non-permissible” activities according to the Islamic faith. Crescent Wealth’s Investment Choice Guide for superannuation investments, for example, describes non-permissible investments as gambling, sale or manufacture of weaponry and the sale and manufacture of alcohol, tobacco and adult material. Depending upon the asset class, certain assets might be regarded as suitable investments even though a “small proportion” of the entity’s revenue is derived from non-permissible investments provided that the proportion falls within the limits set by the Accounting and Auditing Organisation for Islamic Financial Institutions (“AAOIFI”). The Crescent Foundation Fund Pty Limited (the fifth appellant) plays a role of “cleansing” any income derived from receipts of “interest” (by receipting those payments and making corresponding donations to Australian charities) so as to ensure that Crescent Wealth remains Sharia compliant: PJ at [25]. Crescent Wealth’s efforts to ensure that its products remain Sharia compliant “are, indeed, extensive”: PJ at [26]. Crescent Wealth has adopted a number of “distinctive procedures” to ensure ongoing compliance with Islamic financial principles. They include a review of investments by the Shariah Supervisory Board (the “SSB”) comprised of Islamic experts and scholars and ensuring that investments comply with the rulings of SSB.

40 As to these matters, the primary judge at [27] and [28] finds:

27. I accept that adherence to Islamic investment principles is a core component of Crescent Wealth’s business and investment strategy. Moreover, it is apparent, and I accept, that Crescent Wealth has established a reputation in relation to Sharia compliant financial products.

28. Crescent Wealth’s superannuation offering is its primary product, with 80% to 90% of the funds under management by Crescent Wealth attributable to superannuation. Nevertheless, Crescent Wealth also accepts investments into the managed investment products directly. Such investment accounts for the remaining 10% to 20% of the funds it manages.

[emphasis added]

41 As to these matters, the appellants emphasise that 80% to 90% of Crescent Wealth’s business is Sharia compliant superannuation and that the superannuation funds are invested in the four funds according to the options exercised by the investor. The superannuation monies might be invested in Australian ASX listed securities (the Crescent Australian Equity Fund); securities listed on international stock exchanges (the Crescent Wealth International Equity Fund); real property (the Crescent Diversified Property Fund); and, cash instruments such as bonds (the Crescent Islamic Cash Fund). The remaining 10% to 20% of Crescent Wealth’s business is made up of direct investments into one or more of those four funds.

42 Crescent Wealth uses the following logo:

43 Crescent Wealth operates a series of domain names incorporating either “Crescent” or “Crescent Wealth”.

44 At [56] and [57], the primary judge notes (and finds) the following differentiating factors and similarities between Crescent Capital and Crescent Wealth:

56 As at the present, there are a number of matters that differentiate the two parties, including:

The products provided.

The logos associated with the respective businesses.

The class of consumers to whom the products are provided.

The nature of the investments offered.

The persons or institutions to which the products are marketed.

The emphasis by Crescent Wealth on Sharia compliant products.

57 There are also a number of similarities, including:

The use of “Crescent” with respect to offerings.

Domain names.

45 The findings of the primary judge, not surprisingly, emerge out of the way in which the contentions of the parties were framed having regard to the state of the evidence. The primary judge notes that the “concern” of Crescent Capital was “largely directed” to the “future conduct” of Crescent Wealth in expanding beyond “its existing consumer base” which “already includes institutional investors”. Crescent Capital contended that Crescent Wealth operated through fund managers and was diversifying into higher risk property investments and might diversify into private equity investments: PJ at [58]. As to the core points of differentiation, Crescent Wealth contended that there was no evidence before the primary judge of “any realistic prospect” of Crescent Wealth entering the “private equity field” and no evidence that Crescent Capital intends to commence Sharia compliant lending. As to these matters of differentiation, the primary judge at [60] finds that Crescent Capital has agreed with some specific investors to limit investments from its funds to “ethical investing” including some limitations consistent with “aspects of Sharia law” and “other limitations” sought by “an investor” that do not fall within the description of either Sharia law compliant or ethical investing.

46 The primary judge observes at [60] that notwithstanding that Crescent Capital has not engaged in “fully Sharia compliant investing” (although it has engaged in ethical investing and on occasions ethical investments consistent with Sharia law), “it cannot be said that Crescent Capital has decided to remove itself from offering Sharia compliant investments”. Notwithstanding the retention of the possibility of offering Sharia compliant lending, the primary judge concludes (finds), also at [60], that “there is no evidence to suggest that Crescent Capital intends to offer superannuation products or any products other than private equity investments” [emphasis added]. The primary judge also concludes at [60] that Crescent Capital’s retention of the possibility of “offerings to retail investors” of products and financial services (whether Sharia law compliant or otherwise) does not suggest any intention to do so especially having regard to the “nature and amounts of investment progressively [made into] the Crescent Funds since Crescent I” [emphasis added].

47 At [61], the primary judge finds:

There is no evidence that Crescent Capital, as a private equity firm, will offer superannuation products or that Crescent Wealth will set up a private equity business.

[emphasis added]

48 That finding is subject to an immediate qualification by the primary judge drawing upon Crescent Wealth’s apparent recognition or acceptance that as Crescent Wealth grows, “it may attract wholesale investors” and “it is likely that any separation that can be said to presently exist in the class of investors in the respective funds will diminish” [emphasis added]. At [63], the primary judge concludes that the “neat division” between “classes of consumers” within the financial services industry and in the fields of funds or investment management into “retail investors” and “wholesale investors”, between “unsophisticated” and “sophisticated” investors and between those who invest in “private equity” investments and those who do not, is “artificial” and fails to recognise that “fund managers and investors may make investments across many different asset classes and in order to balance their portfolio and to maximise returns” [emphasis added].

49 Consistent with that view of commercial engagement across many different asset classes, the primary judge at [63] notes that Crescent Wealth “already” operates across four of the five identified asset classes: cash, fixed interest, property and shares.

50 The primary judge at [63] accepts Crescent Capital’s contention that “investors”, as “consumers in this industry” do not “necessarily or practically” restrict themselves to one class of investment or to one offeror of investment opportunities, whether within an asset class or across asset classes.

51 The primary judge also finds that consumers/investors would experience “difficulty of obvious separation” between the funds of Crescent Capital and those of Crescent Wealth having regard to the use of “Crescent” in the various fund titles: PJ at [65]. The Crescent Capital Funds are described as Crescent Growth Fund (or Crescent I) and Crescent II, III, IV and V. Crescent Wealth uses the term “Crescent Wealth” in the title of the Superannuation Fund and the International Equity Fund. It uses the term “Crescent” in three of the other funds.

52 At [69], the primary judge concludes that “Funds management”, as a term, is not confined, in the minds of investors (consumers), to any particular class of asset investment and both Crescent Capital and Crescent Wealth operate funds by reference to the term “Crescent”.

53 At [69], the primary judge makes this finding:

I accept that persons making investments, in particular investments of the quantum invested in Crescent Capital’s funds, would take care in the object of that investment and, at present, there is a difference in the nature of the investments that [the] parties offer.

[emphasis added]

54 The primary judge finds that that difference, however, is not decisive because investors do not necessarily “restrict themselves to a single asset class” and Crescent Wealth has (and is) diversifying “within and across asset classes” and has (and is) expanding the amount of funds under management, which has the effect of attracting investors “beyond the ‘mum and dad’ category that presently provides much of its superannuation investment”: PJ at [69]. It followed, for the primary judge, at [69] that:

There is sufficient likelihood of investors and those advising them being misled or deceived or confused by Crescent Wealth’s offerings into believing that Crescent Wealth’s funds are those of Crescent Capital or are part of, or associated with, or managed by, or connected to Crescent Capital.

[emphasis added]

55 The primary judge concluded at [70] that the point of distinction between the circumstances prevailing in Anchorage Capital Partners Pty Ltd v ACPA Pty Ltd (2015) 115 IPR 67 (a case involving large, highly sophisticated, discerning institutional investors) and the circumstances relevant to the activities of Crescent Capital and Crescent Wealth, is that Crescent Wealth “is not aiming its activities at highly sophisticated investors, such that less sophisticated consumers might well be misled” [emphasis added].

56 The primary judge at [70] accepted that the relevant consumer is not, in all the circumstances, “necessarily a sophisticated one”.

57 In the result, the primary judge concluded that the first and second appellants had engaged in conduct that was misleading or deceptive or likely to mislead or deceive by reason of their use of “Crescent Wealth”; the names of the funds; the use of the domain names and the use of the name “Crescent” together with generic words such as “investments” and “funds” and similar such words. That followed for the primary judge because such use is likely to lead investors to believe, wrongly, that such funds, products or services of Crescent Wealth are those of, or associated with, Crescent Capital: PJ at [89]. However, the primary judge also concluded that the contravening conduct, as found, did not mean that all use of the word “Crescent” either alone or in association with other words or in conjunction with a disclaimer, would result in investors/consumers being misled. The primary judge found that Mr Yassine was involved in the contraventions of the first and second appellants. The present respondents failed to make good their case against the present third to ninth appellants.

The grounds of appeal

58 The appellants contend that the primary judge fell into error in finding that the first and second appellants had engaged in misleading or deceptive conduct (or conduct likely to mislead and deceive), principally having regard to the following four considerations. First, the relevant class of consumers, they say, is made up of investors seeking to invest in low risk/low return Sharia compliant superannuation and related investment products in traditional asset classes which do not include private equity investments. Second, Crescent Capital has no reputation in the names and marks “Crescent”, “Crescent Capital” and “Crescent Capital Partners” other than a reputation amongst the Australian financial community as a successful private equity fund manager. Third, Crescent Wealth (by the first two appellants) and Crescent Capital were not, and were not likely to be, engaged in a common field of activity because: (a) Crescent Wealth did not conduct and had no intention of conducting a private equity business; and, (b) Crescent Capital only conducts a private equity business and has no intention of conducting any other business. Fourth, persons considering investments offered by Crescent Wealth and investments offered by Crescent Capital would take care in “the object of their investment” and would view online information or receive documentation showing the logo of Crescent Wealth (if their offering) or the logo of Crescent Capital (if their offering): Ground 1.

59 The appellants say that the primary judge fell into error in finding that there was a likelihood of investors (not being “mum and dad” investors), and those advising them, being misled or deceived or confused by the conduct of Crescent Wealth into believing that Crescent Wealth’s funds were those of Crescent Capital or associated with or managed by or connected to Crescent Capital: Ground 2.

60 The appellants say that the primary judge erred by concluding that there was a likelihood that “less sophisticated” consumers might be misled by the conduct of Crescent Wealth (Ground 3) and erred by failing to find that the relevant class of consumers comprised investors seeking to invest in low risk/low return Sharia compliant superannuation and related investment products in traditional asset classes not including private equity: Ground 4.

Considerations

61 The appellants emphasise a number of features of the Crescent Wealth Funds which, they say, differentiate the activities of Crescent Wealth from the investment activities of Crescent Capital.

62 First, 80% to 90% of Crescent Wealth’s business activity is concerned with the investment of superannuation monies in and across the four Sharia compliant managed investment funds. The remaining 10% to 20% of its activities are concerned with direct investments into and across those funds. Thus, 100% of its business activities for investors are concerned with Sharia compliant investing.

63 Second, investments in the funds are designed for and available to retail investors and the superannuation product has no minimum investment requirement. The minimum investment threshold for direct investment into any one of the Funds is $5,000: PJ at [23].

64 Third, the investments are low risk/low return investments: the superannuation investments target 2% to 4% above the inflation rate; the Australian Equity Fund targets a return of 6.8%; the International Equity Fund targets “capital growth over the long term with total return [after fees] above the MSCI World Islamic [ex-Australia] Index expressed in AUD [unhedged]”; the Diversified Property Fund targets a return 3% above the Reserve Bank of Australia (“RBA”) cash rate; and the Islamic Cash Fund (a cash management fund) targets a return “above” the RBA cash rate.

65 Fourth, the funds distribute returns regularly.

66 Fifth, investments can be withdrawn at any time.

67 Sixth, the Crescent Wealth Funds are managed by third party professional managers rather than Crescent Wealth as it says that it does not have the expertise to manage investment funds.

68 Seventh, all of the funds are Sharia compliant funds.

69 The appellants contrast these seven features with those that, they say, characterise the Crescent Capital investments and thus the focus of Crescent Capital’s activities (and those investors with whom it engages).

70 First, Crescent Capital opens funds (every three to five years) and raises from investors a target fund amount or keeps the fund open for investment for a set time and then closes the fund.

71 Second, by this method, it offers highly sophisticated investors an opportunity, through the Funds, to make private equity investments: a fundamentally different class of investments, they say, to that offered through the Crescent Wealth Funds.

72 Third, funds are invested for the 10 year life of the particular Fund.

73 Fourth, the business model involves investing fund monies in small to medium enterprises by taking equity, engaging directly in the conduct of the undertaking to lift proper performance and then securing a trade sale or a listing of relevant securities on an exchange.

74 Fifth, the required rate of return is significant.

75 Sixth, the required rate of return is high because the investments are high risk.

76 Seventh, private equity investments are a way in which highly sophisticated investors diversify their investments across a portfolio of investments and private equity investments are only suitable as a small percentage of a sophisticated investor’s total portfolio.

77 Eighth, the traditional or main asset classes for investment are said to be cash, fixed interest, property and shares whereas private equity investments in non-listed entities are regarded as investments in “alternative” assets with returns which differ from investments in traditional asset classes and which “provide diversification”. The appellants say that this characterisation of traditional asset classes on the one hand and alternative assets (including private equity investments) on the other hand, and, diversification advantages for an investor’s total investment portfolio can be seen in the text of the AON Master Trust document (AB, Tab 9.1, p 1141) and the van Eyk Research Report. As to the Trust document, it recognises that: “Alternative assets would be expected to have a pattern of returns that differs from traditional assets and thus they are expected to provide diversification”.

78 The appellants’ emphasis on this feature of private equity investments as compared with traditional asset classes is inherently difficult. Although the point is advanced to seek to demonstrate differentiation in the focus and investment activities of Crescent Capital (and its dedication to serving and offering private equity opportunities to investors) from the focus and investment activities of Crescent Wealth, the point necessarily recognises (supported by the material) that those investors looking to invest in funds enabling of private equity investments (with the possibility of high returns counter-balanced against corresponding high risks) are likely to be doing so as part of a diversification strategy to balance a portfolio of investments where the private equity investment might make up a small proportion of an investor’s portfolio of asset classes comprising a mixture of the “main asset classes” and “alternative assets” including private equity investments and other alternative assets: market mutual funds, hedge funds, commodities and infrastructure.

79 If the underlying investment methodology of those persons who invest in private equity is to secure balance and diversification across a portfolio of investments (including the main asset classes), those investors who engage with Crescent Capital on the discrete and singular issue of the merits of investing in one of its private equity focused funds, are likely to see, engage with or otherwise deal with other financial service and product providers focused upon the main asset classes. Those other providers might well include Crescent Wealth and its four Funds (even though such an investor may not be looking for Sharia compliant investments).

80 The appellants contend that investors who engage with Crescent Capital are highly sophisticated, careful, inquiring and discerning investors who would not be misled, or be likely to be misled, should they engage with Crescent Wealth because the investment offerings of Crescent Wealth (which do not include any aspect of private equity investment) are so fundamentally different from the private equity investment offerings of Crescent Capital that any such investor would not fall into a false view that the service and product offerings of Crescent Wealth were those of Crescent Capital or that Crescent Wealth was associated in some way, shape or form with Crescent Capital. That follows, it is said, also because private equity investments are distinguished from other types of investments and not substitutable for them.

81 Finally, the appellants say that an important point of differentiation is that none of the investments Crescent Capital has offered in its various funds are Sharia compliant and although in its fourth fund, Crescent Capital adopted a “responsible investment policy” (avoiding investments in entities producing, for example, tobacco products), the policy did not compel Sharia compliant investments by its funds: banking, insurance and other financial services remained available investments. The appellants says that although a responsible lending policy might be regarded as a policy of making “ethical investments” there is “a world of difference” between ethical investments on the one hand and Sharia compliant investments on the other hand.

82 In fact, the appellants say that the private equity character of Crescent Capital’s sequence of funds (and particularly, relevantly, its most recent two funds), coupled with the notion that an investor in those funds needs to be “a very large institution or an ultra-wealthy individual to participate” (as counsel for Crescent Wealth puts it), renders Crescent Capital’s investors, as a cohort, a very narrow silo of investors “entirely differentiated” from the things Crescent Wealth does: never the consumer twain shall meet.

83 It is now necessary to examine aspects of the material in a little detail. I do so by means of a confidential schedule to these reasons which will be published to the parties but not otherwise.

84 Crescent Capital’s monthly report for July 2006 to investors for its second fund sets out a list of investors in that fund and the magnitude of their investments. There are 12 identified investors (apart from the last two lines on the list), 11 of which are institutions. On any view, their “Committed Capital” and drawn-down or “Contributed Value” is very substantial: see Confidential Schedule, Box 1. The last two lines on the list are described as “Other Crescent Related Investors” and “Other Crescent Fund I Investors/Friends of Crescent”. These last two categories on the list represent persons connected with Crescent Capital and investors who had invested in the first fund and continue to participate in later funds due to their participation at the outset. The appellants say that as to these last two groups of investors, there is simply no prospect of anyone being misled by Crescent Wealth’s use of the name “Crescent Wealth” or “Crescent” because these investors are “utterly aware” that Crescent Wealth is not Crescent Capital and are similarly aware of how Crescent Capital differs from Crescent Wealth.

85 In March 2012 the “Monument Group”, engaged by Crescent Capital to seek out investors, published a report in relation to the fourth fund. The total number of “Limited Partners” is set out at Confidential Schedule, Box 2. The total investment commitments are set out at Confidential Schedule, Box 3. The investing group is relatively small and the commitments are very substantial. Page 15 of that document sets out a list of investors in Crescent Fund IV which identifies the institutional investors and a group described as “individuals” and another group called “General Partner”. These two groups are persons associated with Crescent Capital or partners in Crescent Capital. As before, the appellants say that no investor in either of these two groups could possibly be misled by reason of Crescent Wealth’s use of “Crescent Wealth” or “Crescent”.

86 As to Crescent Fund V, the minimum investment is very substantial: see Confidential Schedule, Box 4. The minimum investment for Crescent Fund IV was the same amount and expressed in the same way. The minimum investment for Crescent Fund III was also significant: see Confidential Schedule, Box 5. Contextually, the minimum investment in Crescent Fund II was $250,000: PJ at [17]. The appellants say that if it is correct to say that a prudent investor places about 5% to 10% of their investments in private equity high return/high risk investments (as a portfolio balancing exercise) then the total portfolio of each investor making the minimum investment in Crescent Fund IV and Crescent Fund V would, theoretically, be in the range set out in Confidential Schedule, Box 6 which means that the numbers in Confidential Schedule, Box 7 would be invested in other assets. The appellants say that the true character of Crescent Capital’s private equity investment activity is reflected in the circumstance that the minimum investment threshold for Crescent Funds IV and V and the likely magnitude of particular investments made into those funds made it necessary for Crescent Capital to establish (for Crescent Fund IV, for example) an electronic data room of documents to enable investors to conduct a due diligence process much along the lines of an acquisition.

87 The appellants say that none of this characterises Crescent Wealth’s investment services or products.

88 As to Crescent Wealth’s presentation of itself to investors, the appellants say that its Facebook pages use the logo at [42] of these reasons very extensively and extensive emphasis is given to the Islamic compliant character of its investments. For example, the screen shot at AB Tab 5.1, p 50 uses the logo, next to the words:

Professional Development

New Course

Islamic Wealth for Professionals

89 Also at AB Tab 5.1, p 50 the following text occurs next to the logo:

Join us for our next

ISLAMIC SUPER

INFO SESSION

90 Similar references occur in the Facebook screenshots at AB Tab 5.1, pp 49, 52, 54 and 56.

91 All of the Facebook screenshots at Tab 5.1 make extensive use of the logo and extensive reference to the relationship between Crescent Wealth Investments and conformity with Halal or Islamic principles. So too does the website. The screenshots at AB Tab 22 show extensive use of the logo throughout; prominent references to “Australia’s First Islamic Wealth Manager”; a description “About Us” in these terms: “Crescent Wealth is Australia’s first ultra-ethical wealth manager, offering a superannuation fund as well as a series of managed funds that invest into socially responsible assets based on Islamic investment principles”; details about each of the Board members of The Crescent Wealth Australian Advisory Board, under the heading (and logo): “Australia’s First Islamic Wealth Manager”; details about the members of The Crescent Wealth Global Advisory Board under the same heading (and logo); and details about the members of The Crescent Wealth Shariah Supervisory Board (under and by reference to the same heading and logo).

92 The advertising and brochure material relating to the superannuation product emphasises the logo, prominently describes the product as “Islamic Superannuation” and describes Crescent Wealth much in the same terms as the Facebook and website screenshots.

93 Large APN Billboards prominently display the logo, the words “Islamic Superannuation” and the question: “Is your Super Halal? Ours is.”

94 The Product Disclosure Statement (“PDS”) for the Crescent Wealth Superannuation Fund displays the logo and tells the reader, apart from a range of required information, the following:

1. About Crescent Wealth Super

Crescent Wealth is Australia’s first dedicated Ultra Ethical wealth manager offering an innovative suite of investment products. As a pioneer with specialist expertise in a dynamic new sector, we offer all Australians and attractive alternative in socially responsible investing.

…

3. Benefits of investing with Crescent Wealth Super

The Fund is designed to allow you to save and accumulate your superannuation based on Islamic investment principles.

5. How we invest your money

Under Ultra Ethical investing, certain social and moral considerations, which are in accordance with Islamic investment principles, are taken into account in determining the investment objectives of the underlying funds in which the Fund invests. For example, investment and assets which may give exposure to income from gambling, adult material, alcohol or weaponry is avoided. These principles are highly relevant to the acquisition of assets in the underlying funds.

95 The asset classes making up the Crescent Balanced Investment Option, as described in the PDS, are: Australian Shares, International Shares, Property and Cash and Fixed Income. The appellants say that none of the marketing material conveys any suggestion of an association with a private equity firm named Crescent Capital.

96 In these proceedings, the appellants, plainly enough, must demonstrate error on the part of the primary judge. In the principal proceeding, the respondents claimed damages under s 12GF of the ASIC Act (apart from claims under the ACL) for loss suffered by reason of contended contraventions of s 12DA and s 12DB of the ASIC Act. Although those provisions are well known, it should be noted that s 12DA contains a statutory prohibition upon a person, in trade or commerce, engaging in conduct, in relation to financial services, that is misleading or deceptive or likely to mislead or deceive. Section 12DB contains a statutory prohibition upon a person, in trade or commerce, in connection with the supply or possible supply of financial services, or in connection with the promotion, by any means, of the supply or use of financial services; making a false or misleading representation that services are of a particular standard, quality, value or grade; or making a false or misleading representation that services have sponsorship, approval, performance characteristics, uses or benefits; or making a false or misleading representation that the person making the representation has a sponsorship approval or affiliation.

97 The trial was confined to the question of whether the appellants had engaged in contravening conduct.

98 As already noted, the primary judge found contraventions by the first and second respondents by conduct consisting of use of “CRESCENT WEALTH”, the names of Crescent Wealth’s Funds, use of domain names and use of “Crescent” coupled with words such as “investments” and “funds”: PJ at [71] and [89].

99 Declaration 1, explanatory of the conduct, is framed in terms of contraventions of s 12DA of the ASIC Act. Orders 3 and 4 are restraining injunctions which give remedial expression to the contraventions. Orders 5 and 7 are mandatory corrective orders. Order 6 restrains Mr Yassine from aiding the first and second appellants from engaging in any conduct which would not comply with Orders 3 and 4.

100 Crescent Wealth’s conduct is directed to “the public at large” with a particular emphasis on retail investors of the Islamic faith: PJ at [21].

101 In Campomar v Nike International (2000) 202 CLR 45 (“Campomar”), the Court (all seven Justices: Gleeson CJ, Gaudron, McHugh, Gummow, Kirby, Hayne and Callinan JJ) observed that the question that arose in that case (as it does in this case) was whether there was a “sufficient nexus” between the conduct and the “contended misconceptions” (or contended deceptions) in the mind of others: Campomar, [98].

102 The appellants here contend that there is no nexus sufficient to support the contraventions or the relief granted against the appellants (and particularly the first and second appellants) by the primary judge.

103 The question cannot be considered “in the abstract”: Campomar, [99]. Regard must be had to the particular circumstances of the case: Campomar, [99]. Whether the conduct amounts to a representation is a question of fact to be decided against the background of “all the surrounding circumstances”: Campomar, [100]. Where, as in this case, the conduct consists of contended representations to the “public at large or to a section thereof”, the issue of the “sufficiency of the nexus” between the conduct (or apprehended conduct) and the misleading, or likely misleading, of persons acquiring (purchasing) the service (or products) is to be approached at a “level of abstraction” (Campomar, [101]) not present in the case of an express untrue representation made to a specific identified individual: a direct linear representation.

104 The “level of abstraction” finds expression in the “entry” into the inquiry of the “ordinary” (Mason J, Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd (1982) 149 CLR 191 at 210 (“Puxu”) or “reasonable” (Gibbs CJ, Puxu at 199) members of a cohort or class of prospective users of the service (Campomar, [102]) to which particular “characteristics” can properly be “objectively” attributed having regard to the “circumstances of the case” including all the surrounding circumstances: Campomar, [102], [99], [100].

105 Where the persons in question are members of a cohort or class to which the conduct in question was directed “in a general sense” (Campomar, [103]), it is necessary to “isolate”, by some “criterion”, a “representative member” of that cohort (Campomar, [103]) and the “inquiry” (as to the sufficiency of the nexus), is to be undertaken with respect to “this hypothetical individual” so as to determine “why the misconception has arisen” (or is likely to arise if no remedy is granted): Campomar, [103].

106 The “heavy burden” imposed by the statutory norm reflected in s 52 of the Trade Practices Act 1974 (Cth) (which is the statutory norm reflected in s 12DA of the ASIC Act and s 18 of the ACL) suggests that where the effect of the conduct on a cohort or class of persons is in issue, the statutory prohibition “must be” regarded as contemplating the effect of the conduct on “reasonable members of the class”: Campomar, [103].

107 In the case of mass-marketed products for general use such as sportswear and perfumery products, the Court in assessing the “likely reactions” of ordinary or reasonable members of the class of prospective purchasers may well give little weight to “assumptions” by persons whose reactions are “extreme” or “fanciful”: Campomar, [105]. These proceedings do not involve mass-marketed consumer products such as athletic footwear or perfumery. The proceedings do involve, however, financial products and services extensively marketed by Crescent Wealth by brochures, billboards, Facebook pages and webpages to persons seeking or likely to be seeking investment services especially in relation to prudent superannuation investments in respect of a number of asset classes.

108 The proper analysis required of the primary judge in this case involved isolating, by some criterion supported by the evidence in all the circumstances, a hypothetical representative member of the class to whom the conduct was (and is) directed and then testing why the contended misconceptions arose or were likely to arise by reason of the use of “Crescent Wealth”, “Crescent”, the domain names, the Fund names and the company titles.

109 In assessing the reactions or likely reactions of ordinary or reasonable members of the relevant class of persons, the Court would be likely to give little weight to assumptions by persons whose reactions were extreme or fanciful. Reasonable or ordinary members of the class would be likely to bring an inquiring mind to the assessment of the investment products and services of Crescent Wealth promoted to the class. The sufficiency of the nexus between conduct and the misleading (or deception) of the class, tested against the hypothetical reasonable or ordinary member, is not made good simply because the conduct causes such a person to be confused or caused to wonder about issues of connection, source or origin between the products of Crescent Wealth and those of Crescent Capital. The question for the Full Court is whether the primary judge applied the correct method or test (that is, whether error is demonstrated) and whether, in undertaking the assessment according to that test (if correctly identified) the primary judge reached a conclusion open on the evidence notwithstanding that minds might legitimately differ about the application of the correct test in all the circumstances of the case.

110 In Campomar, their Honours put it this way at [107]:

In [the relevant circumstances of the case], looking at the matter objectively, there was nothing capricious or unreasonable or unpredictable in [the primary judge’s] conclusion that the [relevant conduct] was likely to mislead or deceive members of the public into thinking [erroneously that the relevant product was in some way promoted, distributed or sponsored by Nike International].

[emphasis added]

111 There are a number of difficulties with the contentions of the appellants.

112 First, having regard to the principles identified by the primary judge at [38] and [39] and the primary judge’s observations at [63] to the effect that investors do not necessarily or practically restrict themselves to one class of investment, or to one offeror of investment opportunities (whether within an asset class or across asset classes), and the observations at [70] that the relevant consumer is not, in the circumstances, necessarily a sophisticated one, it seems clear enough that the primary judge fully appreciated the test to be applied and, in all the circumstances of the case, identified a hypothetical representative of a class of investors against which the sufficiency of the nexus was to be tested.

113 Second, Mr Yassine explains in his affidavit of 16 February 2015 and in his oral evidence that AON Hewitt (a wholesale investor) invested $1.5 million with Crescent Wealth (for management rather than a capital investment in any of the companies) shortly after Crescent Wealth commenced business and before Crescent Wealth Superannuation Fund was established. He explained that the investment was a matter of “sheer serendipity” (T, p 218, ln 16) arising out of the good relationship subsisting between Ms Sengupta for AON Hewitt and Mr Omran for Crescent Wealth. Mr Yassine gave evidence that the investment at February 2015 had a current value of $1.57 million: T, p 218, lns 4-10. Notwithstanding those circumstances, Mr Yassine accepted that Crescent Wealth “would welcome another investment now into Crescent Wealth’s funds if it came along”: T, p 218, lns 18-19. Moreover, Mr Yassine accepted that he would have welcomed such an investment “any time in between 2011 and now” (T, p 218, lns 21-22) and that, from the time of setting up Crescent Wealth’s funds, he (and therefore Crescent Wealth) “[was] happy to receive investments from high net worth individuals into the funds as long as they [investors] agreed to invest in [the] Sharia compliant investments we offered”: T, p 218, lns 24-31. Mr Yassine also accepted that it remained an aim of the Crescent Wealth Superannuation Fund to “target higher net worth clients, through superannuation” and Crescent Wealth aimed, “absolutely”, to “target financial planners and professional groups”: T, p 218, lns 37-41.

114 Third, AB, Tab 10.21, is a document which bears the title “Crescent Wealth Superannuation Fund Investment Committee – 12 November 2014”. Page 7 of that document (p 246 of the AB) contains a page marked “Direct marketing”. It sets out amended sales targets for 2014 and a series of bullet points related to “marketing efforts for the quarter”. As to direct marketing, the document says this:

• Amended sales targets for 2014 of $65m+. Discussions still advancing with Investment Platforms and Financial Planner groups eg. AMP, Yellow Brick Road and AON

• Increase in Average member balance every quarter; currently at approximately $27,500 an increase from $23,000 the quarter before.

…

[emphasis added]

115 As to the marketing efforts for the quarter, the document says this:

• Marketing efforts have been targeting higher net worth clients. This has meant targeting financial planners and professional groups.

…

[emphasis added]

116 Apart from these matters, the marketing document identifies that Crescent Wealth is continuing to “leverage” its existing partnerships with community groups; engage in event sponsorships in tandem with Islamic groups; continue its digital media advertising through Facebook and Youtube; continue with “regular Mosque drops around Sydney”; and adopt targeted efforts to “cover Islamic schools in NSW and VOC via school visits”.

117 As to the matters at [114] and [115] of these reasons, it seems clear enough that Crescent Wealth’s marketing efforts have been targeting higher net worth clients, financial planners and professional groups and the likelihood is that some of the individuals within that group would be wholesale investors.