FEDERAL COURT OF AUSTRALIA

Queensland North Australia Pty Ltd v Takeovers Panel [2015] FCAFC 68

IN THE FEDERAL COURT OF AUSTRALIA | |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. Within 14 days of the date this judgment, the parties file and serve either:

(a) a joint proposed minute of order; or

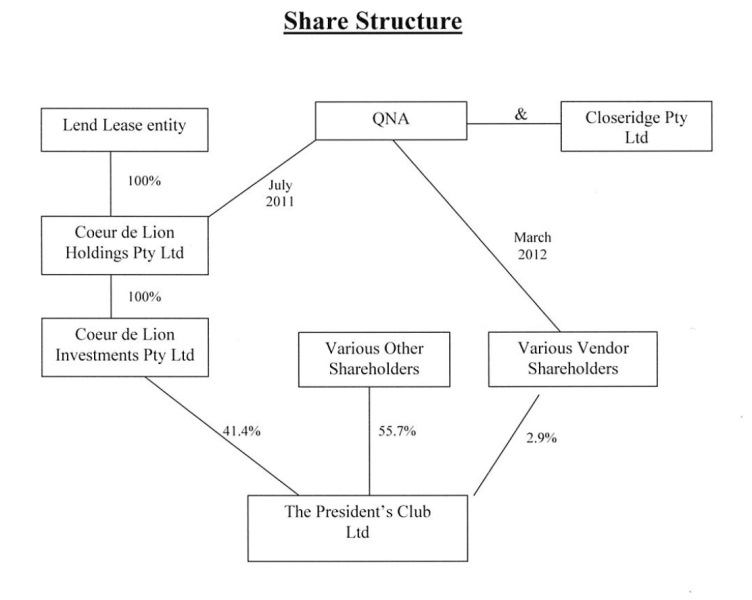

(b) in the event of disagreement, proposed minutes of order with short written submissions in support;

reflecting these reasons and the proposed orders of the Court, including as to costs;

2. Costs be reserved; and

3. There be liberty to apply.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

QUEENSLAND DISTRICT REGISTRY | |

GENERAL DIVISION | QUD 300 of 2014 |

ON APPEAL FROM THE FEDERAL COURT OF AUSTRALIA |

BETWEEN: | QUEENSLAND NORTH AUSTRALIA PTY LTD First Appellant CLOSERIDGE PTY LTD (ACN 010 560 157) Second Appellant CLIVE FREDERICK PALMER Third Appellant |

AND: | TAKEOVERS PANEL First Respondent THE PRESIDENT'S CLUB LIMITED (ACN 010 593 263) Second Respondent PRESIDENT, TAKEOVERS PANEL Third Respondent AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Fourth Respondent |

JUDGES: | DOWSETT, MIDDLETON & GILMOUR JJ |

DATE: | 22 May 2015 |

PLACE: | BRISBANE |

REASONS FOR JUDGMENT

THE COURT

1 This appeal is from orders of a judge of this Court, delivered on 5 June 2014, dismissing an application for judicial review of certain decisions and orders of the first respondent, the Takeover Panel (Panel): see Queensland North Australia Pty Ltd v Takeovers Panel (2014) 100 ACSR 358; [2014] FCA 591. Central to these was a declaration of unacceptable circumstances made by the Panel, pursuant to s 657A of the Corporations Act 2001 (Cth) (the Corporations Act), on 24 July 2012.

2 The appeal, for the reasons which follow, should be allowed.

3 It is convenient to set out the background to this matter substantially as described by the primary judge in the Reasons at [7]-[20], [22]-[28] and [38]-[40] without further attribution.

Shareholdings and offers

4 The President’s Club Limited (TPC) is an unlisted public company. Its capital is divided into 7,488 ordinary shares and five subscriber shares. The subscriber shares are irrelevant to this case.

5 TPC operates a timeshare scheme at the property previously known as the Hyatt Regency Coolum but now known as the Palmer Coolum Resort (the resort). TPC is the tenant under two leases, both dated 21 December 1988 and each for a term of 80 years over all the lots in The President’s Club Golf Community Titles Scheme and The President’s Club Tennis Community Titles Scheme (community titles schemes).

6 The constitution of TPC contemplated that each holder of ordinary shares in the company would hold one or more parcels of 13 ordinary shares, and would own an associated one-quarter interest as tenant in common in a lot (a Villa Interest) in either of the community titles schemes. The effect of a set of interlocking agreements was that a purchaser of one timeshare interest must become both:

a member of TPC, holding 13 shares; and

the registered proprietor of a corresponding one-quarter interest in either of the community titles schemes.

7 Purchasers of timeshare interests were also required to execute:

a deed poll, binding them, if they sold their Villa Interest, to sell the corresponding shares in TPC to the same person; and

an assignment of a letting pool agreement, under which their Villa Interest was made available with others as part of a pool.

8 At all material times Coeur de Lion Holdings Pty Ltd (Lion Holdings) was the sole shareholder of Coeur de Lion Investments Pty Ltd (Lion Investments), which in turn owns 3,107 or 41.4% of the shares in TPC. The appellants tendered a diagram at trial explaining the share structure of relevant entities, as follows:

9 On 31 January 2005, the Australian Securities and Investments Commission (ASIC) exercised its powers pursuant to s 601QA(1)(a) of the Corporations Act to conditionally exempt TPC and Lion Investments from registration as a managed investment scheme under Ch 5C of the Corporations Act. The exemption was provided on the basis that Lion Investments entered into a deed poll (the Deed Poll) whereby Lion Investments covenanted that it would not exercise more than 10% of its voting rights on any resolution other than:

in circumstances consented to in writing by ASIC; or

in relation to a resolution to wind up the scheme.

10 Clause 4.2 of the Deed Poll allowed Lion Investments to revoke the Deed Poll upon providing to ASIC and TPC at least 180 days prior written notice.

11 In July 2011, the first appellant, Queensland North Australia Pty Ltd (QNA) acquired 98% of the shares in Lion Holdings from Lend Lease. The remaining 2% of shares were acquired by the second appellant, Closeridge Pty Ltd (Closeridge). Both QNA and Closeridge are companies associated with the third appellant, Mr Palmer.

12 By letter dated 15 September 2011, Lion Investments gave notice to ASIC and TPC that it intended to revoke the Deed Poll. The revocation took effect on or about 13 March 2012, following expiry of the 180 day notice period required by cl 4.2 of the Deed Poll. It followed that, on this date, the ASIC exemption ceased to apply. This revocation of the Deed Poll was included in the relevant “circumstances” by the Panel, but was treated as irrelevant. We observe that the revocation in any event took effect in mid-March 2012, more than two months prior to the application made by TPC to the Panel, to which we will later refer.

13 In or around March 2012, QNA acquired 221 additional shares in TPC (plus corresponding Villa Interests) being 2.9% of the shares in that company. This took QNA’s direct or indirect interest in TPC to approximately 44.3%.

14 On 14 March 2012, TPC held an extraordinary general meeting to consider amending its constitution to cap the voting power of Lion Investments at a meeting to 10%, effectively replicating the covenant in the Deed Poll previously entered by Lion Investments. The relevant resolution was not carried.

15 On 12 April 2012, QNA lodged a bidder’s statement with ASIC, proposing a bid for all shares in TPC and the corresponding Villa Interests. The bid was unconditional. The purchase price offered for each parcel of 13 shares and corresponding Villa Interest was $55,013 (being $1 per share for the 13 shares and $55,000 for the Villa Interest).

16 On 20 April 2012, ASIC wrote to QNA raising a number of concerns with the bidder’s statement, including inadequate disclosure, and a suspected ongoing contravention of s 606 of the Corporations Act. On 24 April 2012, QNA’s solicitors wrote to TPC advising that QNA did not intend to proceed with its bid. ASIC was notified of this decision by letter of the same date.

17 On 26 April 2012, ASIC advised QNA’s solicitors that, having regard to s 631(1) of the Corporations Act, ASIC considered the bid to have been made public through the lodgement of the bidder’s statement with ASIC. Accordingly, QNA could not withdraw its bid and was required to proceed with the offer within two months from the announcement.

18 On 11 May 2012, QNA sought an extension of time within which to lodge a supplementary and replacement bidder’s statement. On the same date ASIC granted the extension of time sought.

19 On 21 May 2012, QNA lodged a replacement bidder’s statement (replacement bidder’s statement). Again, QNA proposed to make an offer to purchase all the shares in TPC and all Villa Interests. On the front page of the replacement bidder’s statement was the following statement:

The bid being made is for both your shares and your Villa Interest. It is not possible to accept the bid in relation to your shares only or in relation to your Villa Interest only.

20 On page 1 of the replacement bidder’s statement there appeared the following statement:

While there is no formal stapling of your President’s Club Shares to your Villa Interest, it is likely that you have executed a deed poll that obliges you to sell your shares if you sell your Villa Interest to the same person. Also clauses 6(b) and 6(c) of the Constitution require that a member of President’s Club must own a Villa Interest and a member’s shareholding is limited to the number of Villa Interests owned.

21 Later in the replacement bidder’s statement there appeared the following statement:

Because the ASIC Deed Poll was still current at the time of the Acquisition and therefore QNA’s voting power was limited to 10% of persons who actually vote, QNA did not acquire voting power of more than 20% at the time of the Acquisition. Accordingly, QNA was not required to make a takeover offer for the remaining shares in President’s Club or otherwise comply with the takeover provisions of the Corporations Act.

As CDLI has revoked the ASIC Deed Poll (and the revocation became effective on 19 March 2012) QNA’s voting power is no longer restricted.

22 The “Acquisition” was defined in the replacement bidder’s statement as the transaction in July 2011 whereby QNA completed the acquisition from Lend Lease of 98% of the shares in Lion Holdings.

23 On 1 June 2012, the solicitors for QNA advised the solicitors for TPC that:

the replacement bidder’s statement would not be dispatched;

a further replacement bidder’s statement would be provided on 4 June 2012; and

QNA would propose further relief to ASIC to extent the dispatch period until 12 June 2012.

24 No further replacement bidder’s statement had been provided as of 26 June 2012 when TPC lodged an application with the Panel for a declaration of unacceptable circumstances pursuant to ss 657A and 657C(2) of the Corporations Act.

Declaration of Unacceptable Circumstances

25 The Panel on 24 July 2012 made a declaration of unacceptable circumstances in relation to the affairs of TPC pursuant to s 657A of the Corporations Act (the Declaration). We will refer to this, in detail, later in these reasons.

Orders of the Panel

26 In addition to making the Declaration in respect of the affairs of TPC, the Panel made the following orders pursuant to s 657D of the Corporations Act:

1. The Associated Parties must not exercise any voting rights that attach to the Acquisition Shares.

2. The Associated Parties must not make any further acquisitions of a relevant interest in shares in TPC, except:

a. with the consent of the Panel or

b. pursuant to acceptances under a takeover offer referred to in Order 4 or

c. the acquisition by Mr Clive Palmer of the shares corresponding to Lot 64 on BUP 8874 recently acquired by Mr Palmer from CDLI.

3. The Associated Parties must not dispose of, transfer or charge any of the Acquisition Shares, except:

a. with the consent of the Panel or

b. for a disposal or transfer pursuant to the acquisition by Mr Clive Palmer of the shares corresponding to Lot 64 on BUP 8874 recently acquired by Mr Palmer from CDLI.

4. Orders 1, 2 and 3 cease if all of the following requirements are met:

a. QNA or an associate of it makes offers for all the shares in TPC under a takeover bid that complies with chapter 6 and which meets the following conditions:

i. the terms are no less favourable than those set out in the original Bidder’s Statement lodged with ASIC on 12 April 2012

ii. the offer price is no less than $65,013 for each parcel of shares and the corresponding villa interest

iii. the offer period is no less than 2 months and

iv. ASIC has confirmed in writing to the proposed bidder that it is otherwise satisfied with the terms of the offer and the disclosure in the bidder’s statement. This confirmation is not to be construed as ASIC’s approval of the bidder’s statement and

b. no less than 50% of the offers made for shares not already held by the Associated Parties are accepted and

c. all the accepting shareholders have been paid.

5. If QNA or an associate proposes to make a takeover bid under Order 4:

a. QNA and its associates must ensure that the proposed bidder provides ASIC with all reasonable assistance requested by ASIC and

b. should ASIC be unable to settle terms or disclosure with the proposed bidder, either ASIC or the proposed bidder may refer the issue to the Panel for determination.

6. In these orders the following terms have the corresponding meaning:

Acquisition Shares 3,328 shares in TPC held:

(a) As to 3,107 shares, by CDLI or an associate and

(b) As to 221 shares, by QNA or an associate

Associated Parties CDLI, CDLH, Closeridge, QNA and each of their respective associates

CDLH Coeur de Lion Holdings Pty Ltd

CDLI Coeur de Lion Investments Pty Ltd

Closeridge Closeridge Pty Ltd

QNA Queensland North Australia Pty Ltd

TPC The President’s Club Limited

Grounds of review before primary judge

27 The grounds of application outlined in the amended originating application for judicial review filed by the appellants and relied on at the hearing were relatively lengthy. Materially, they are as follows:

1. …

2. …

3. …

4. The declaration of unacceptable circumstances and the decision to extend time were made in circumstances where there was a breach of the rules of natural justice.

5. Further, and in the alternative, in determining that the application was made in time the Panel made an error of law in construing s.657B(a) of the Act as referring to continuing circumstances and not to the occurrence of the circumstances represented by the acquisitions by QNA in July 2011 and March 2012.

6. Further, and in the alternative, the Panel made the decision to extend time when there was no evidence or other material to justify doing [so].

7. In making the declaration of unacceptable circumstances the Panel made an error of law in finding that the acquisition by QNA of 98% of the shares in Lion Holdings contravened s.606 of the Act.

8. The Panel made findings and acted upon them in making the declaration of unacceptable circumstances (arising out of the acquisition in July 2011) when there was no evidence or other material to justify doing [so.]

9. The declaration of unacceptable circumstances was an improper exercise of the power conferred on the Panel by the Act in that the Panel took into account irrelevant considerations (at paragraph 107 of its reasons).

9A. The Panel made an error of law by stating conclusions without identifying and providing reasons which set out the findings of fact and reference to the evidence on which those findings were based (in paragraph 107 of its reasons).

10. In making the declaration of unacceptable circumstances the Panel made an error of law in finding that the acquisition by QNA, in March 2012, of 221 shares in the President’s Club contravened s. 606 of the Act.

11. In making the declaration of unacceptable circumstances (arising out of the acquisition in March 2012) the Panel (at paragraph 108 of its reasons):

i. did not make any finding as to or identify the effect on the matters required by s657A(2) of the Act as preconditions to the making of the declaration;

ii. accordingly, the declaration was not authorized by the Act.

12. Alternatively, the Panel made findings and acted upon them in making the declaration of unacceptable circumstances (arising out of the acquisition in March 2012) when there was no evidence or other material to justify doing as to the effect that the circumstances have had, are having, will have or are likely to have on:

i. the control, or potential control, of the President’s Club;

ii. the acquisition, or proposed acquisition, by a person of a substantial interest in the President’s Club.

13. The Panel made a finding and acted upon it that the shares and villa interests were “effectively stapled” and could only be transferred together when there was no evidence or other material to justify [this finding].

14. In making the declaration of unacceptable circumstances and in the orders then made, the Panel made an error of law in concluding that it had jurisdiction to make orders which extended to villa interests.

15. The orders made by the Panel under s.657D of the Act were an improper exercise of the power because the nature of orders made was so unreasonable that no reasonable person could have so exercised the power and because the Panel failed to take into account the matters required by s.657D(2), and in failing to provide reasons which set out the findings of fact and reference to the evidence on which those findings were based.

16. Further the orders made by the Panel insofar as they are directed to entities other than the first and second applicants, and in particular the third applicant as an “associated Party” within the meaning of the Orders, were made in circumstances where there was a breach of the rules of natural justice and s.657D

17. The decision by the third respondent not to revoke the direction appointing Mr Ewen Crouch, as sitting President of the Panel, involved a breach of the rules of natural justice.

The appeal

28 Put shortly, the appellants contend that the appeal should be allowed because the primary judge erred:

(a) in failing to find that the application to the Panel, and its declaration of unacceptable circumstances, were out of time;

(b) if (a) is not accepted, in the various other respects outlined below including, most significantly, failing to find that the July 2011 acquisition was not a breach of s 606 of the Corporations Act.

29 The appellants have numbered the grounds to correlate to those which were before the primary judge and which we have set out above at [27].

30 The first and third respondents appeared for the purpose of submitting to such order as the Court may make but made no submissions on the merits.

Grounds 4, 5 and 6 – the time limitation points

31 Chapter 6 of the Corporations Act regulates takeovers. Its purposes are set out in s 602 and include the aim that takeovers should take place in “an efficient, competitive and informed market” as well as providing various protections for the interests of investors within that market.

32 These purposes, in terms, define the nature of the considerations at work in reaching a conclusion that circumstances in relation to the affairs of a company are unacceptable and that the public interest requires a certain form of regulatory intervention in the market: Attorney-General (Cth) v Alinta Limited (2008) 233 CLR 542 at [6] per Gleeson CJ.

33 Sections 657A(1) and (2) of the Corporations Act provide:

657A Declaration of unacceptable circumstances

(1) The Panel may declare circumstances in relation to the affairs of a company to be unacceptable circumstances. Without limiting this, the Panel may declare circumstances to be unacceptable circumstances whether or not the circumstances constitute a contravention of a provision of this Act.

Note: Sections 659B and 659C deal with court proceedings during and after a takeover bid.

(2) The Panel may only declare circumstances to be unacceptable circumstances if it appears to the Panel that the circumstances:

(a) are unacceptable having regard to the effect that the Panel is satisfied the circumstances have had, are having, will have or are likely to have on:

(i) the control, or potential control, of the company or another company; or

(ii) the acquisition, or proposed acquisition, by a person of a substantial interest in the company or another company; or

(b) are otherwise unacceptable (whether in relation to the effect that the Panel is satisfied the circumstances have had, are having, will have or are likely to have in relation to the company or another company or in relation to securities of the company or another company) having regard to the purposes of this Chapter set out in section 602; or

(c) are unacceptable because they:

(i) constituted, constitute, will constitute or are likely to constitute a contravention of a provision of this Chapter or of Chapter 6A, 6B or 6C; or

(ii) gave or give rise to, or will or are likely to give rise to, a contravention of a provision of this Chapter or of Chapter 6A, 6B or 6C.

The Panel may only make a declaration under this subsection, or only decline to make a declaration under this subsection, if it considers that doing so is not against the public interest after taking into account any policy considerations that the Panel considers relevant.

34 Section 657B and s 657C(3) of the Corporations Act respectively impose limits on the power of the Panel to make a declaration of unacceptable circumstances, and the competence of a party to apply for such a declaration. These sections provide:

657B When Panel may make declaration

The Panel can only make a declaration under section 657A within:

(a) 3 months after the circumstances occur; or

(b) 1 month after the application under section 657C for the declaration was made;

whichever ends last. The Court may extend the period on application by the Panel.

657C Applying for declarations and orders

…

(3) An application for a declaration under section 657A can be made only within:

(a) 2 months after the circumstances occurred or;

(b) a longer period determined by the Panel.

35 The Panel’s decision to extend time was first communicated to the parties in an email from Ms Nicole Graham of the Panel to the parties on 18 July 2012, when the parties were informed that:

The Panel has met and is minded to declare that unacceptable circumstances exist in relation to the affairs of President’s Club.

…

Extension of time

The Panel considers that the circumstances of the acquisitions by QNA in or around July 2011 and March 2012 are continuing. For the avoidance of doubt, the Panel has extended the time for the application to be made by President’s Club, under s657C(3)(b) to 26 June 2012.

36 In its decision the Panel stated:

[40] In our view, there are alleged in the application contravention of the Corporations Act which are ongoing circumstances. Alternatively, in case it should be necessary we extended the time for making the application to the date on which it was made (26 June 2012). On the alternative basis, we had one month within which to make a declaration, if one was to be made.

37 The primary judge held that the Panel's decision to extend time was contrary to the rules of natural justice, with the result that the application before it was out of time, and the Panel ought not to have conducted the proceedings, unless it was unnecessary to extend time because, as the Panel found, the relevant circumstances were “ongoing": Reasons at [48]-[51]. The respondents do not challenge her Honour's finding on the extension point. The pivotal question therefore is whether her Honour was correct in upholding the Panel's finding "that the unacceptable circumstances alleged by The President's Club were ongoing": Reasons [61].

38 The appellants contend that in referring to the time when "the circumstances occur" or "have occurred" as the starting point for the limitation periods, ss 657B(a) and 657C(3)(a) must be taken to mean "the circumstances which are the subject of a declaration by the Panel under s 657A occur/have occurred". They submit that her Honour's reasons overlook this point, in focussing instead on the general meaning of "circumstances" (Reasons at [62]-[66]), the language in s 657A(2) (at [67]-[69]), and the perceived need to consider the application before the Panel as to whether ongoing circumstances were alleged and whether they were identified by the Panel with sufficient certainty in its reasons (at [70]-[80]).

39 TPC contends, at the threshold, that this construction is not within grounds 4-6 of the amended originating application for judicial review. It submits that the closest ground of judicial review agitated was ground 5, which argued that the Panel had made an error of law in construing s 657B(a) of the Corporations Act as referring to continuing circumstances, not to the occurrence of the share acquisitions in July 2011 and March 2012. However, it submits that this was not argued by reliance on an interpretation of s 657B as referring to circumstances the subject of a declaration by the Panel, but rather on the footing that "the circumstances" in s 657B referred to an act or event, rather than to an ongoing state of affairs. It is this argument, it submits, that the primary judge is addressing at [63]-[66] of the Reasons. The appellants’ argument that the primary judge’s reasons overlook interpreting the section as referring to the circumstances the subject of the declaration made by the Panel is, it submits, incorrect. That the primary judge’s reasons do not address this interpretation, it contends, was because it was not put.

40 Accordingly TPC submits that the appellants should not be allowed to raise on appeal a new point, and one which is outside the grounds of judicial review.

41 We reject this first contention. The construction of s 657B(a) and, implicitly, s 657C(3)(a) contended for by the appellants was raised by ground 5 in a way which sufficiently ventilated these arguments of the appellants.

42 Nor do we accept that the matter was not argued before her Honour. The appellants’ written submissions at first instance outline this argument and counsel for the appellants raised this argument during the course of the hearing. There was no submission made by the respondents at first instance that the argument was outside the scope of the grounds. Indeed, counsel for TPC appeared to make the same argument in oral submissions.

43 TPC, as well as ASIC, then submit that the appellants’ interpretation of ss 657B(a) and 657C(3)(a) should be rejected because it requires adding into those sub-sections words that are not there: “which are the subject of a declaration by the Panel under s 657A”. It is contended by TPC that these words would limit the operation of the subsection, and are not necessary for achieving the purpose or object of the legislation: s 15AA of the Acts Interpretation Act 1901 (Cth).

44 It further submits that, for two reasons, there is no need to introduce those words. First, the expression “the circumstances” in s 657B of the Corporations Act has the same meaning as “unacceptable circumstances” in s 657A. Second, just what the unacceptable circumstances are, and the time of their occurrence, are matters to be determined by the Panel.

45 Whilst we accept these two propositions they do not advance TPC’s argument which is a man of straw. The appellants’ construction arises, not by the implication of additional words but, as we will explain, on a plain reading of those sections together with s 657A.

46 The primary judge at [73] concluded, wrongly in our view, that the terms of the Declaration were not confined to the specific transactions in which the relevant shares were acquired in July 2011 and March 2012.

47 As her Honour stated there, “[t]he Panel clearly considered that ‘the circumstances of’ those acquisitions were unacceptable”, and that “[i]n order to identify ‘the circumstances’ of those acquisitions it [was] necessary to have regard to the reasons of the Panel”.

48 The appellants submitted that the primary judge was entitled to have regard to the reasons of the Panel in order to appreciate what was intended by the Declaration. It is not necessary to resolve this question as, in our view, the terms of the Declaration are clear.

49 TPC submits that the expression “unacceptable circumstances” can embrace more than the facts of a contravention and may include the circumstances created by or arising from a contravention. This analysis is unhelpful. It tends to conflate what constitutes the “circumstances” and what the Panel may have regard to in deciding that those circumstances constitute “unacceptable circumstances”.

50 There is a clear delineation between the circumstances and the effect that they have had, are having, will have or are likely to have on the control or potential control of the company or the acquisition, or proposed acquisition, of a substantial interest in the company: s 657A(2)(a)(i) and (ii). Relevantly, in this case it is the effect of the circumstances which rendered them unacceptable circumstances. The circumstances are as described by the Panel in paragraphs 1-9 of the Declaration as follows:

CIRCUMSTANCES

1. The President’s Club Ltd (TPC) is an unlisted company with more than 50 members. Its capital is divided into 7,488 ordinary shares and 5 subscriber shares (the latter having no right to vote, to dividends or to participate in the net assets of the company on a winding up).

2. Coeur de Lion Holdings Pty Ltd (CDLH) owns all the shares in Coeur de Lion Investments Pty Ltd (CDLI). CDLI owns 3,107 shares in TPC (approximately 41.4%).

3. Ordinary shares in TPC are voting shares. They carry voting rights beyond those in the definition of ‘voting share’ in section 9. This is not changed by a deed poll entered by CDLI, revocable on 6 months’ notice and which has been revoked, in favour of the Australian Securities and Investments Commission as follows:

Where [CDLI] and its associates are not disqualified and excluded from voting their interests at a meeting, [CDLI] covenants that any voting rights held by [CDLI] and its associates or any operator, manager, promoter in relation to each Scheme, must not be exercised in excess of 10% of the votes that may be cast (after deducting any votes not cast by anyone or more members) on a resolution by members of the relevant Club other than:

a. in circumstances consented to in writing by the ASIC; or

b. in relation to a resolution to wind up the relevant Scheme.

4. In or around July 2011, CDLI:

a. was the holder of the shares.

b. had power to exercise, or control the exercise of, a right to vote attached to the shares, and/or

c. had power to dispose of, or control the exercise of a power to dispose of, the shares.

5. In or around July 2011, Queensland North Australia Pty Ltd (QNA acquired 98% of the shares in CDLH. The remaining 2% of the shares in CDLH were acquired by Closeridge Pty Ltd.

6. By reason of section 608(3)(a), or alternatively section 608(3)(b), in or around July 2011 QNA acquired a relevant interest in the shares in TPC that CDLI had a relevant interest in (first acquisition).

7. None of the exceptions in section 611 applied to the first acquisition. The first acquisition occurred in contravention of section 606.

8. Further in March 2012, QNA acquired 221 additional shares in TPC (2.9%) taking its relevant interest in TPC shares to approximately 44.4% (collectively, second acquisition). The second acquisition was the acquisition of a substantial interest in TPC.

9. The second acquisition occurred in purported reliance on item 9 of section 611. However, to the extent that item 9 was met, it was only by reason of the first acquisition, which contravened section 606.

51 The substance of the circumstances was that each of the first and second acquisitions, as defined, were made in contravention of s 606 of the Corporations Act.

52 It is s 657A(2)(a) which is central to this appeal. We have, for ease of reading, set out the terms of this provision:

(2) The Panel may only declare circumstances to be unacceptable circumstances if it appears to the Panel that the circumstances:

(a) are unacceptable having regard to the effect that the Panel is satisfied the circumstances have had, are having, will have or are likely to have on:

(iii) the control, or potential control, of the company or another company; or

(iv) the acquisition, or proposed acquisition, by a person of a substantial interest in the company or another company; …

(Emphasis added.)

53 Thus, circumstances may be unacceptable under s 657A(2)(a) having regard to their effect, past, present or their effect or likely effect in the future.

54 Accordingly, the effect or likely effect of the circumstances do not constitute part of the circumstances capable of being declared unacceptable circumstances. Indeed this distinction is expressed in the Declaration at paragraphs 10 and 11 reproduced below at [58] of these reasons.

55 The primary judge described the circumstances which were declared by the Panel to be unacceptable circumstances as follows:

[78] The acquisitions of shares in July 2011 and March 2012 were clearly, in the view of the Panel, contraventions of the Corporations Act. However as the reasons of the Panel also demonstrate, they were contraventions which:

• Were ongoing, in that the applicants continued to maintain a relevant interest in those shares.

• Had created a continuing state of affairs in respect of The President’s Club where the remaining shareholders were faced with a situation where QNA had achieved, and could continue to exercise, effective control of the company, without shareholder approval, or without the advantage of shareholders receiving an open bid.

• Had created a state of affairs where a takeover bid by QNA for the remaining shares would have ameliorated the situation faced by the shareholders, but QNA had failed to make the bid despite preparation of two bidder’s statements (one of which was revoked in May 2012), and that state of affairs was continuing.

56 Then, at [79] of the Reasons her Honour said that “(t)hese circumstances were clearly distinguished by the Panel from the effects of the circumstances to which the Panel had regard”.

57 Properly understood these were but some of the effects which arose for consideration by the Panel under s 657A(2)(a)(i) and (ii) and did not form part of the circumstances. It was these effects, amongst others, which led the Panel to declare those circumstances to be unacceptable circumstances. Accordingly, her Honour was in error in so characterising them.

58 That those circumstances, respectively constituted “unacceptable circumstances” is set out at paragraphs 10 and 11 of the Declaration as follows:

10. It appears to the Panel that the circumstances of the first acquisition are unacceptable having regard to:

(a) the effect that the panel is satisfied the circumstances have had, are having, will have or are likely to have on:

(i) the control, or potential control, of TPC or

(ii) the acquisition, or proposed acquisition, by a person of a substantial interest in TPC and

(d) The purposes of Chapter 6 set out in section 602 and

(e) Because they constituted, constitute, will constitute or are likely to constitute a contravention of a provision of Chapter 6.

11. Further it appears to the Panel that the circumstances of the second acquisition are unacceptable having regard to:

(a) the effect that the Panel is satisfied the circumstances have had, are having, will have or are likely to have on:

(i) the control, or potential control, of TPC or

(ii) the acquisition, or proposed acquisition, by a person of a substantial interest in TPC and

(b) the purposes of Chapter 6 set out in section 602.

(Emphasis added.)

59 These declarations reflect the reasons of the Panel at [103], [107] and [108].

60 The Declaration expressly states under each of paragraphs 10 and 11 that the “circumstances” of the first and second acquisitions are “unacceptable” having regard to the “effect” of the circumstances.

61 We take the expression “the circumstances of” employed by the Panel in each of those paragraphs of the Declaration as meaning, as we have earlier explained, that in substance the “circumstances” for the purposes of s 657A were the “first acquisition” and the “second acquisition” being the share acquisitions made in July 2011 and March 2012, respectively each made in contravention of s 606 of the Corporations Act. Then, as the Declaration makes clear, the two circumstances were each declared to be unacceptable circumstances “having regard to”, amongst other things, the effect which the Panel was satisfied that those circumstances have had, are having, will have or are likely to have on the control or potential control of TPC, or the acquisition or proposed acquisition, by a person of a substantial interest in the TPC.

62 Section 657B provides for when the Panel can make a declaration. The first time limit under subs (a) is that which is within three months after “the circumstances” occur. Likewise, the time limit for making an application provided for under s 657C(3)(a) is two months after “the circumstances” have occurred.

63 We are of the opinion that “the circumstances”, in each case, are those which, as the appellants submit, are the subject of the declaration of unacceptable circumstances, namely, as the Declaration at paragraphs 10 and 11 makes clear, the circumstances of the first and second acquisitions, respectively.

64 In order for the time limitations under ss 657B and 657C to operate effectively the relevant circumstances must be capable of being identified as having arisen at a particular time. Whether those circumstances will be declared as unacceptable circumstances is a matter for decision and declaration by the Panel.

65 TPC and ASIC argue that the circumstances were ongoing or continuing circumstances. We do not agree. The first and second acquisitions in contravention of s 606 of the Corporations Act occurred on identifiable dates. Those were the relevant circumstances.

66 Section 657B(a) is in terms that the Panel can only make a declaration under s 657A within three months “after the circumstances occur”. Section 657C(3)(a) provides that an application for a declaration under s 657A can be made only within two months “after the circumstances have occurred”.

67 The expressions “occur” and “have occurred” are distinguishable from “are occurring” or “have been occurring”, the latter of which in each case is what TPC and ASIC in substance contend is open.

68 Those expressions, in our opinion, mean “come to exist” and “came to exist” respectively, or “arise” and “arose”.

69 That the effects of the circumstances (the acquisition of the shares in breach of s 606) are continuing does not render the circumstances as continuing to “occur” or as continuing to “have occurred”.

70 The legislative scheme contemplates applications to the Panel being made, as well as the making of declarations by the Panel, within relatively short periods of time following the occurring of the particular “circumstances”. The policy reasons which underpin the purposes of Ch 6 set out in s 602 and to which we have referred point, together with the limitation periods found in ss 657B and 657C, to the timely disposition, in short compass, of such applications.

71 In that context it cannot be thought that the Parliament intended the expressions “after the circumstances occur” and “after the circumstances have occurred” to be capable of being reset on a daily basis with each new day being the starting point for the calculation of the time limits imposed. Such a construction would strain against the policy objectives and, far from being timely, very long periods of time could elapse between the first “occurring” of the circumstances and their continuing occurrence, without offending the time limits. During such extended periods the market would be operating on a basis which might later be the subject of regulatory intervention by the Panel.

72 Such an approach does not meet the commercial imperatives, including timeliness, found in the legislative scheme.

73 In this case the latest of the share acquisitions occurred in March 2012 and accordingly, time had expired by the time of TPC’s application in June and the Panel's Declaration in July. The time limits set by ss 657B and 657C(3) cannot be extended by relying on the ongoing effects of the circumstances found to exist or to have existed.

74 TPC and ASIC also seek to characterise the appellants’ construction as leading to impracticality because in proceedings before the Panel it will inevitably address the time limitations imposed by s 657B section before making a declaration under s 657A; consequently, there will be no declaration of unacceptable circumstances at the time the Panel comes to apply s 657B.

75 We reject this submission. As the appellants correctly submit, this submission overlooks the reality that limitation periods often cannot be determined prior to findings on the facts underlying an asserted cause of action, so that limitation questions rarely justify summary determination of proceedings: see Wardley Australia Limited v State of Western Australia (1992) 175 CLR 514 at 533. The asserted facts in this case are that certain circumstances were said to exist and were such that the Panel should declare them to be unacceptable circumstances. Before the discretion to extend time may be exercised under s 657C(3) those circumstances require to be proved. There may be a factual contest. There is no difficulty, in that situation, for the Panel first resolving the factual questions and thereafter determining whether or not to extend time under s 657C(3). The legislative scheme here does not suggest a different approach.

76 Accordingly, for these reasons, we have concluded that the primary judge erred in failing to find that the application to the Panel and its declaration of unacceptable circumstances were each made out of time. Contrary to her Honour’s finding at [48], it was necessary for time to be extended in each case. As her Honour found, the Panel’s decision to extend time was contrary to the rules of natural justice.

77 The appeal, upon these grounds, should be allowed.

Ground 7 — s 606 of the Corporations Act

78 Section 606 (relevantly) states:

Prohibition on certain acquisitions of relevant interests in voting shares

Acquisition of relevant interests in voting shares through transaction entered into by or on behalf of person acquiring relevant interest

(1) A person must not acquire a relevant interest in issued voting shares in a company if:

(a) the company is:

(i) a listed company; or

(ii) an unlisted company with more than 50 members; and

(b) the person acquiring the interest does so through a transaction in relation to securities entered into by or on behalf of the person; and

(c) because of the transaction, that person’s or someone else’s voting power in the company increases:

(i) from 20% or below to more than 20%; or

(ii) from a starting point that is above 20% and below 90%.

Note 1: Section 9 defines company as meaning a company registered under this Act.

Note 2: Section 607 deals with the effect of a contravention of this section on transactions. Sections 608 and 609 deal with the meaning of relevant interest. Section 610 deals with the calculation of a person’s voting power in a company.

Note 3: If the acquisition of relevant interests in an unlisted company with 50 or fewer members leads to the acquisition of a relevant interest in another company that is an unlisted company with more than 50 members, or a listed company, the acquisition is caught by this section because of its effect on that other company.

…

(Emphasis added)

79 The appellants accept that QNA indirectly acquired a “relevant interest” (as referred to in s 606(1) and as defined in s 608). The key issue in this ground of appeal primarily concerns whether there was an increase in someone’s “voting power”. If that is found to be the case, the next question is whether that increase was “because of the transaction”.

Voting Power and relevant interest

80 The term “voting power” is defined in s 610 (relevantly) as follows:

Voting power in a body or managed investment scheme

Person’s voting power in a body or managed investment scheme

(1) A person’s voting power in a designated body is:

x 100

where:

person’s and associates’ votes is the total number of votes attached to all the voting shares in the designated body (if any) that the person or an associate has a relevant interest in.

total votes in designated body is the total number of votes attached to all voting shares in the designated body.

Note: Even if a person’s relevant interest in voting shares is based on control over disposal of the shares (rather than control over voting rights attached to the shares), their voting power in the designated body is calculated on the basis of the number of votes attached to those shares.

Counting votes

(2) For the purposes of this section, the number of votes attached to a voting share in a designated body is the maximum number of votes that can be cast in respect of the share on a poll…

…

(Emphasis added)

81 Section 9 defines “Voting share”:

voting share in a body corporate means an issued share in the body that carries any voting rights beyond the following:

(a) a right to vote while a dividend (or part of a dividend) in respect of the share is unpaid;

(b) a right to vote on a proposal to reduce the body’s share capital;

(c) a right to vote on a resolution to approve the terms of a buy-back agreement;

(d) a right to vote on a proposal that affects the rights attached to the share;

(e) a right to vote on a proposal to wind the body up;

(f) a right to vote on a proposal for the disposal of the whole of the body’s property, business and undertaking;

(g) a right to vote during the body’s winding up.

82 Section 608(1) provides as follows in relation to “a relevant interest”:

A person has a relevant interest in securities if they:

(a) are the holder of the securities; or

(b) have power to exercise, or control the exercise of, a right to vote attached to the securities; or

(c) have power to dispose of, or control the exercise of a power to dispose of, the securities.

It does not matter how remote the relevant interest is or how it arises. If 2 or more people can jointly exercise one of these powers, each of them is taken to have that power.

83 Section 610 was intended to measure voting control (for the purposes of the takeover provisions of the Corporations Act) by reference to voting power (that is, the number of votes controlled, rather than the number of voting shares held). The Explanatory Memorandum to the Corporate Law Economic Reform Program Bill 1998 (Cth), which proposed s 610, stated (p 45 at [7.17]) that:

… Voting power will be calculated by identifying any share that either the person or an associate has a relevant interest in and determining how many votes are attached to those shares as a proportion of the total number of votes. Given the possibility that the number of votes attached to a share may vary, the number of votes to be counted is:

- the number that may be cast on the election of a director, or

- if no votes are cast for the election of a director — the number that may be cast on the amendment of the constitution (proposed subsection 610(2)).

…

(Emphasis added)

84 The question in this appeal is to determine the operation of s 610(2) in the context of Chapter 6, and in particular the operation of s 606.

85 As we have already indicated, the purpose of Chapter 6 is broadly concerned with ensuring that acquisition of voting power occurs in “an efficient, competitive and informed market” (s 602(a)) and to that end, as set out in s 602(b), that shareholders and directors (among others):

(i) know the identity of any person who proposes to acquire a substantial interest in the company, body or scheme; and

(ii) have a reasonable time to consider the proposal; and

(iii) are given enough information to enable them to assess the merits of the proposal

…

86 It follows that proposed substantial acquisitions must be disclosed. One of the reasons for that disclosure requirement is in aid of protecting shareholders (particularly smaller ones) who may be disadvantaged by a change in control, and may otherwise not have an opportunity to sell their shares.

87 It is essential that armed with the disclosure, affected others can take appropriate and timely action. However, in circumstances where a shareholder had an unfettered ability to increase a shareholding from, say, 19% to 80% (or even a compulsory acquisition threshold) under cover of a third party agreement, such affected others would be deprived of the opportunity to take appropriate and timely action – an outcome which would be antithetical to the purpose of the Chapter. Further, third party contracts are or can be transient, making consideration of them, in the context of the purpose of Chapter 6, potentially misleading as to true control. The above indicates that the term “voting power” in Chapter 6 should be understood as referrable to the constitution of the relevant company.

88 The appellants argue that the word “attached” is effectively defined in s 610(2) as “the maximum number of votes that can be cast in respect of the share on a poll”. However, the purpose of s 610(2) is not to provide a definition of the word “attached” but to cover a situation where the number of votes may vary, as articulated in the Explanatory Memorandum (p 45 at [7.17]). Subsection 610(2) simply refers to the maximum number of votes which a person is entitled to in respect of the share, which is the relevant number for the counting of votes “attached to all voting shares” in the calculation of “voting power” under s 610(1).

89 The words “attached to” in s 610(2) (and ss 606 and 608) are to be understood, in their natural meaning, by reference to the corporate compact made under the company’s constitution.

90 Whilst in a different context, in HNA Irish Nominee Ltd v Kinghorn (2010) 78 ACSR 553; [2010] FCAFC 57 at [37], the Full Court made the following observation as to the concept of “rights attached”:

It is a long hallowed usage in this field of discourse to speak of the bundle of rights conferred on a shareholder by the corporate compact between the members of a company as the “rights attached” to that member’s share: see Greenhalgh v Arderne Cinemas Ltd [1946] 1 All ER 512 esp at 515-516; White v Bristol Aeroplane Co [1953] 1 Ch 65 at 70 and 75.

91 Similarly, the words “votes attached” can be naturally understood to refer to the votes conferred under the corporate compact, or constitution of a company, which usually prescribes voting rights which vary across all the shares issued. For instance, voting rights attached to preference shares are almost invariably restricted.

92 Therefore, the Deed Poll’s existence and the covenant therein by Lion Investments that it would not exercise more than 10% of its voting rights other than in limited circumstances (which are not presently relevant) does not affect the number of “votes attached” under TPC’s constitution, and therefore has no impact on the statutory scheme.

93 It follows from the above that the second question as to whether the voting power increased “because of the transaction” is easily answered. QNA’s voting power increased from 0% to over 40% as a direct result of the one transaction in July 2011 when it acquired the shares in Lion Investments.

94 We make a separate observation.

95 The Panel referred both to Lion Investments’ (and therefore QNA’s) power to exercise, or control the exercise of voting rights which are the subject of the first acquisition, and to the power to dispose of, or control the exercise of a power to dispose of the shares. In its reasons at [85] the Panel held that Lion Investments had a relevant interest “constituted by [the] power to dispose of the shares”. The Panel proceeded on the same basis with respect to QNA’s second acquisition (which did not involve Lion Investments).

96 Even if the Deed Poll deprived Lion Investments (and therefore QNA) of its power to exercise or authorise the voting rights attached to Lion Investment’s shares, this does not mean that Lion Investments (and therefore QNA) was deprived of its power to dispose of, or control the power to dispose of, the shares. The acquirer would obtain the shares with voting rights. That fact reinforces the view that at all material times, Lion Investments (and therefore QNA) had power to exercise or control the voting rights. Any other view would suggest that Lion Investments could give more than it owned.

Grounds 9A – Adequacy of reasons

97 Section 657A(6) of the Corporations Act imposes a statutory obligation on the Panel to provide written reasons for its declaration of unacceptable circumstances. This obligation is enhanced by s 25D of the Acts Interpretation Act 1901 (Cth) which provides:

Where an Act requires a tribunal, body or person making a decision to give written reasons for the decision, whether the expression “reasons”, “grounds” or any other expression is used, the instrument giving the reasons shall also set out the findings on material questions of fact and refer to the evidence or other material on which those findings were based.

(Emphasis added.)

98 The statutory obligation to provide reasons must be applied having regard to the materiality and significance of particular findings on material questions of fact: see, for example, Willis v Repatriation Commission (2012) 202 FCR 323 at [17]–[18] and Repatriation Commission v Holden (2014) 142 ALD 267 (Holden) at [77].

99 As the primary judge noted, the role of the Panel as a specialist expert administrative body, its powers and duties under the Corporations Act, and the nature of the matters with which it deals all heavily impact upon its approach to decision-making.

100 The Panel did make findings of fact, but such findings of fact made by the Panel were closely intertwined with value judgments and opinions reached by the Panel as an expert body in relation to the legal rights and obligations of parties.

101 The Panel was considering an application for a declaration of unacceptable circumstances in which it was alleged that QNA had acquired a relevant interest in voting shares in contravention of s 606 of the Corporations Act, and against a background where QNA had also failed to progress a takeover bid for the remaining shares in the company. This is a matter of judgment for the Panel in light of the material before it including the submissions of the parties.

102 The primary judge was not satisfied that the reasons for the decision of the Panel failed to disclose any facts upon which the Declaration was based, nor was she persuaded that the Panel was merely asserting the matters of which it was required to be satisfied without pointing in its reasons to supporting factual foundations. We agree.

103 The Panel summarised the relevant facts in over 30 paragraphs of reasons, and then later discussed those facts. The conclusions reached by the Panel in [107]–[108] of its reasons, must be read in the context of the broader discussion of the Panel in those reasons.

104 There were adequate reasons for conclusions concerning s 657A(2)(a), (b) and (c) individually, based upon the Panel’s approach to s 606. So long as the Panel’s reasons were adequate in relation to one subparagraph of s 657A(2), this would support the Declaration made by the Panel. There are adequate reasons in the various paragraphs leading up to [98] of the Panel’s reasons for the conclusion that the July 2011 acquisition contravened s 606, which was the primary basis of the Declaration (see [107] of the Panel’s reasons and the preceding paragraphs [103]–[106]).

105 In relation to the second acquisition in March 2012, it was contended by the appellants that there was no attempt by the Panel in its reasons to identify that the addition of another 2.9% of the shares acquired made any relevant material difference to the extent of control exercised by QNA over the company. We reject this submission for the same reasons as the primary judge: see [176] – [183] of the Reasons.

106 At [110] of its reasons the Panel states:

[110] It appears to us that the circumstances of QNA’s subsequent purchases in reliance on the ‘creep’ provision in item 9 of section 611 are unacceptable. While they may not have involved a contravention, reliance was, in our view, based on a contravention (namely, the initial acquisition). The subsequent acquisitions consolidated QNA’s control of TPC. Moreover, had the initial acquisition been made by a takeover bid, the subsequent acquisitions would have occurred in circumstances in which the shareholders had information and a reasonable and equal opportunity to participate in any benefits. As it happened, the shareholders sold their shares (and villa interests) to QNA at different prices.

(Emphasis added, footnotes omitted.)

107 In forming this view, the Panel also had regard to the decision of Emmett J in Brierley Investments Ltd v Australian Securities Commission (1997) 78 FCR 255. In that case his Honour noted at 262:

A very small proportion of the issued share capital of a company might be material or significant in particular circumstances.

108 In light of our conclusion on the time limitation points, we do not need to further consider this aspect of the appeal. It may be that even if the criticisms as to the inadequacy of reasons were accepted, the Panel’s decision would not necessarily be set aside. Other relief could be granted depending on the circumstances including directing the Panel (if still in existence) to provide further reasons: see Holden at [84]–[93].

Conclusions

109 There has been a lengthy passage of time since the events forming the subject of the Panel hearing occurred. This may suggest that the matter should not be remitted to the Panel. However, we do not know what has transpired in the market since then. It is by no means clear that remitting the matter to the Panel would be futile.

110 In our view the matter should be remitted to the Panel to be considered and determined according to law. In view of our conclusions on the operation of s 606, the Panel should now consider whether an extension of time to bring the application should be granted.

111 The appropriate orders of the Court would seem to be that the appeal be allowed, the orders of the primary judge be set aside, the decision of the Panel be set aside, and the matter be remitted to the Panel to be heard and determined according to law. We will give the parties the opportunity to file and serve within 14 days a joint minute of order reflecting these reasons (including as to costs) or in the event of disagreement, short written submissions in support of the orders sought.

I certify that the preceding one hundred and eleven (111) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justices Dowsett, Middleton & Gilmour. |