FEDERAL COURT OF AUSTRALIA

Wilmink v Westpac Banking Corporation [2015] FCAFC 17

IN THE FEDERAL COURT OF AUSTRALIA | |

First Appellant PETER PAALVAST Second Appellant | |

AND: | Respondent |

DATE OF ORDER: | 23 FEBRUARY 2015 |

WHERE MADE: |

THE COURT ORDERS THAT:

2. The appellants pay the costs of the appeal.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 922 of 2014 |

ON APPEAL FROM THE FEDERAL COURT OF AUSTRALIA |

BETWEEN: | KEVIN WILMINK First Appellant PETER PAALVAST Second Appellant |

AND: | WESTPAC BANKING CORPORATION Respondent |

JUDGES: | FOSTER, YATES AND GLEESON JJ |

DATE: | 23 FEBRUARY 2015 |

PLACE: | SYDNEY |

REASONS FOR JUDGMENT

THE COURT:

1 This is an appeal from two decisions of a single judge of this Court (Wilmink v Westpac Banking Corporation [2014] FCA 872 (Wilmink (No 1)) and Wilmink v Westpac Banking Corporation (No 2) [2014] FCA 889 (Wilmink (No 2))).

2 Her Honour dismissed the appellants’ claim for damages against the respondent (“bank”) with costs.

3 The appeal was heard immediately before an appeal from the decision of another judge of this Court (Atkinson v Commissioner of Taxation [2014] FCA 1217).

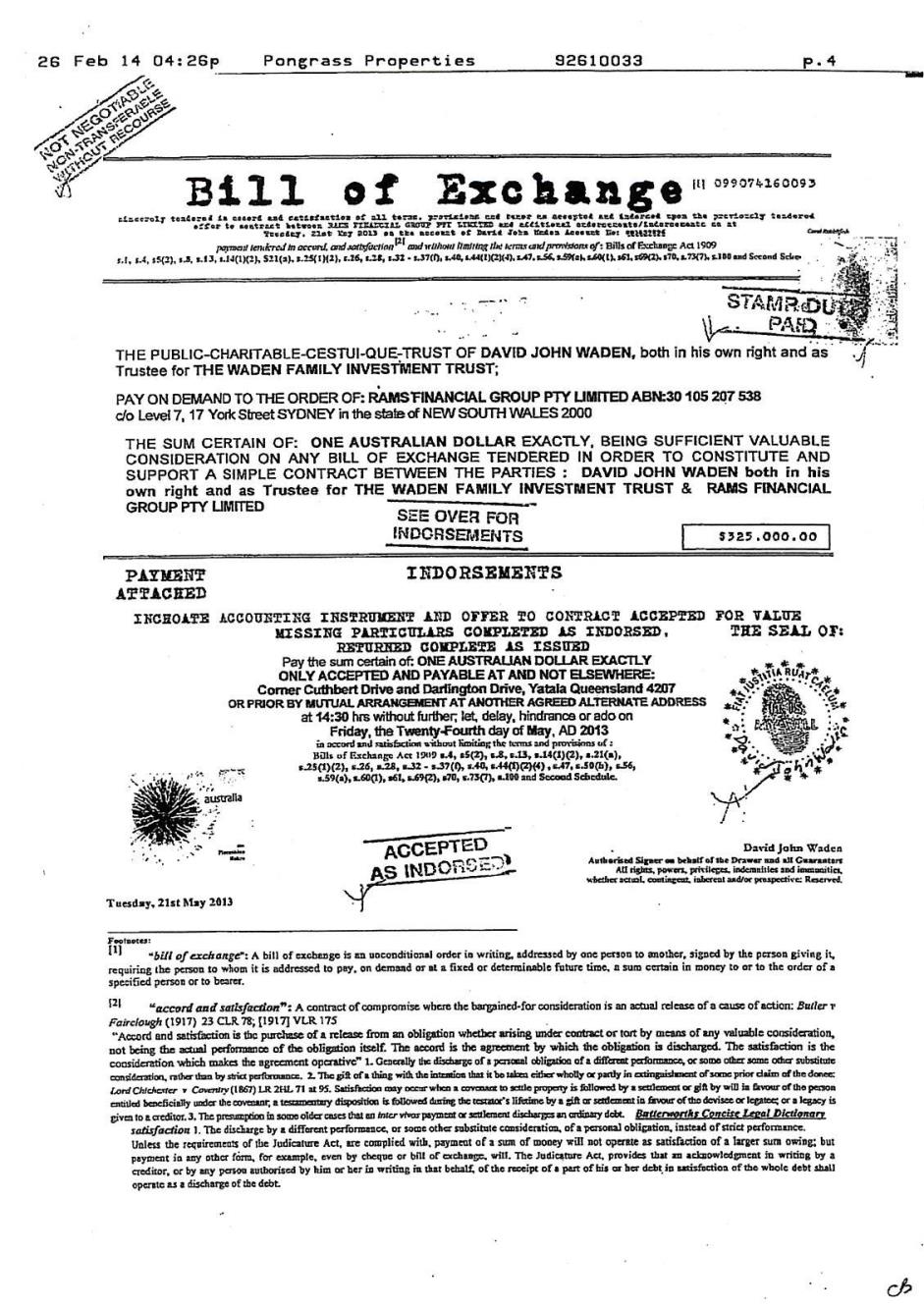

4 The claim is based upon an alleged default by the bank under a purported bill of exchange. The purported bill of exchange was created by a Mr Waden. The contention that the bank has any obligation under that document has no foundation. As appears from the Reasons in Atkinson v Commissioner of Taxation [2015] FCAFC 18, a similar claim based on a purported bill of exchange created by Mr Atkinson also has no foundation.

Background to the appeal

5 The primary judge set out the factual background to the appeal at paragraphs 1 to 7 of her Reasons for Judgment in Wilmink (No 1). There is no challenge to her Honour’s findings in those paragraphs. In summary:

(1) A Mr Waden as trustee of the Waden Family Investment Trust entered into a loan agreement with the bank through RAMS Financial Group Pty Ltd (“RAMS”), acting as loan originator. The loan was secured by a mortgage over real property and by a guarantee given by Mr Waden in favour of the bank. RAMS is a wholly owned subsidiary of the bank;

(2) The bank (by its solicitors) issued default notices dated 23 April 2012 to Mr Waden both in his personal capacity and in his capacity as trustee of the Waden Family Investment Trust and subsequently commenced proceedings in the District Court of Queensland seeking judgment for $313,563.55 being the amount of the loan plus interest, and possession of the security property;

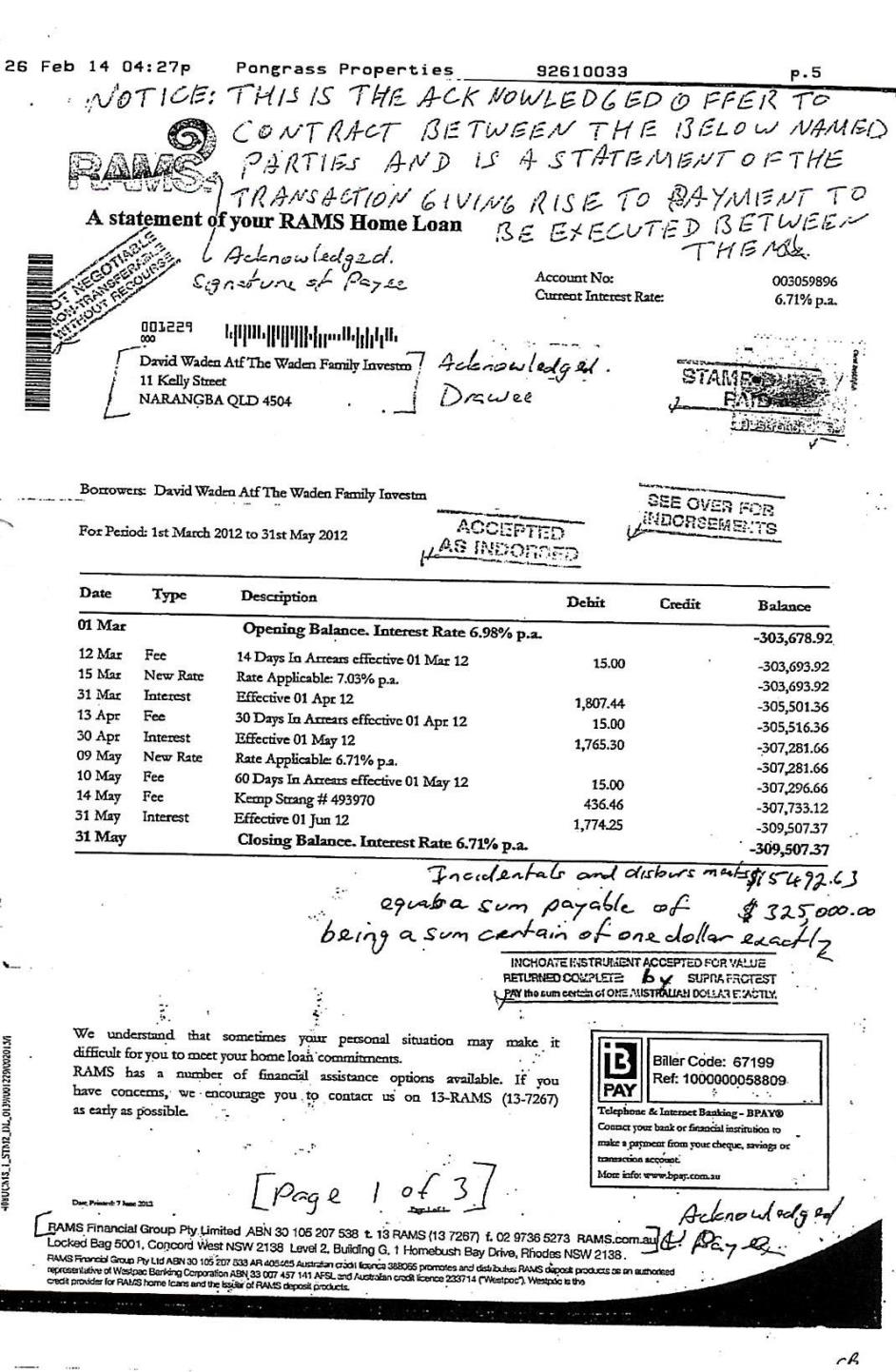

(3) RAMS sent Mr Waden a loan statement for the period 1 March 2012 to 31 May 2012 (“loan statement”);

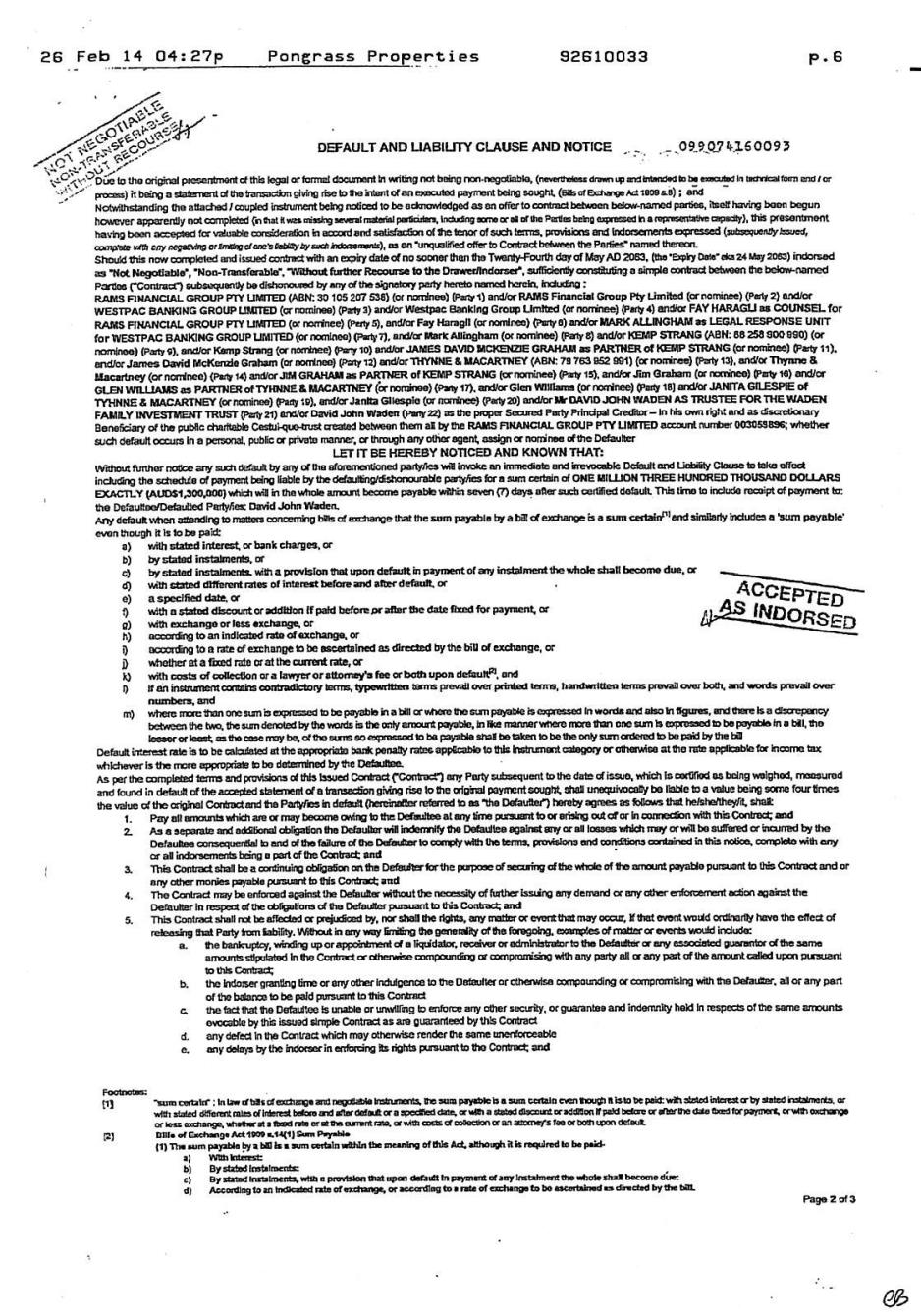

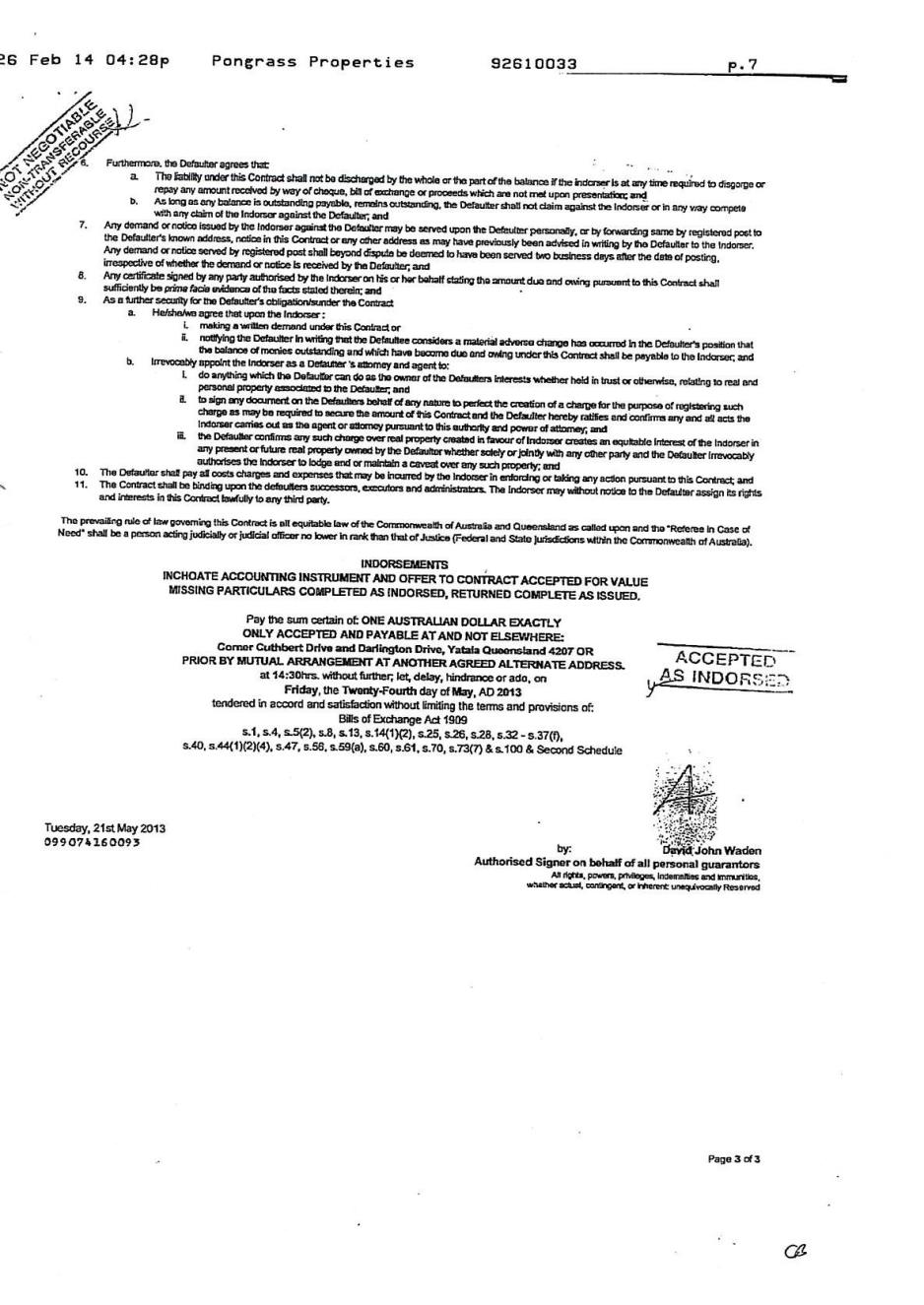

(4) Mr Waden filed a defence in the District Court proceedings in which he stated “On 21 May 2013, I paid to the plaintiff the sum of $325,000 by Registered Post which was the amount claimed in the statement of claim plus incidentals”. At the hearing before the District Court, Mr Waden claimed that he had paid the sum of $325,000 by way of a bill of exchange. A copy of the document relied upon by Mr Waden was attached to the primary judge’s Reasons and is also attached to our Reasons. The document comprises four pages, including the loan statement on which there are several handwritten annotations and stamps, together with other pages created by Mr Waden or on his behalf. The document contains a section entitled “Default and Liability Clause”. The latter section is claimed to impose an obligation on the bank to pay $1.3 million to Mr Waden in certain circumstances;

(5) On 2 December 2013, the rights created in Mr Waden by the Default and Liability Clause, if any, were allegedly assigned to Mr Wilmink as trustee of the Bangarra Trust;

(6) On 13 December 2013, a judge of the District Court ordered that the bank have summary judgment on its money claim and its claim for possession of the security property.

6 The appellants now assert an entitlement to damages against the bank in the sum of $1.3 million. The event of default is not clear. However, the underlying proposition is that, by RAMS’ act in issuing a loan statement, Mr Waden was enabled to impose upon the bank (through the creation of the purported bill of exchange) a liability for damages of $1.3 million. The appellants contend that their case is supported by the Bills of Exchange Act 1909 (Cth) (“Bills of Exchange Act”). As explained below, that proposition is unsound and must be rejected.

Parties to the appeal

7 As finally constituted, the appellants are the applicants in the proceeding below, Messrs Wilmink and Paalvast. Mr Paalvast appeared at the hearing of the appeal on his own behalf and purportedly on behalf of the Bangarra Trust. Mr Paalvast made both written and oral submissions.

8 Mr Wilmink did not appear at the appeal. Mr Paalvast said that he did not know the whereabouts of Mr Wilmink. Mr Paalvast submitted that Mr Wilmink had resigned as a trustee of the Bangarra Trust. In the absence of any satisfactory evidence of that fact, the Court declined to remove Mr Wilmink as an appellant.

Primary judge’s Reasons

9 Her Honour dealt with the proceeding on the papers.

10 She concluded that the purported bill of exchange was not a bill within the meaning of the Bills of Exchange Act and that the various provisions of that Act relied upon by the appellants to support their claim had no relevant operation. Her Honour found that the appellants’ “attempt to convert a ‘run of the mill’ bank statement into a bill of exchange [was] at best misguided; at worst, disingenuous”. Accordingly, there was no basis for the appellants’ claim for damages against the bank.

Grounds of appeal

11 The appellants’ amended Notice of Appeal specifies four grounds of appeal.

Grounds 1 and 3

12 The appellants contend that the primary judge erred in finding that “a Loan Statement was incapable of conversion to a bill of exchange as referred to in section 25” of the Bills of Exchange Act and that, as a result, s 50(1) had no application to the facts of this case. They also complain that her Honour’s findings contradicted the unrebutted evidence and demonstrated a misunderstanding of the relevant statutory provisions.

13 The finding of most relevance to these grounds of appeal, at [29] of her Honour’s Reasons, is:

… that the Loan Statement was not a bill of exchange under s 8(1) of the Act and, further, was incapable of conversion to a bill of exchange under s 25. Given that the Loan Statement was not and could never be a bill of exchange, s 50(1) could have no application.

14 Her Honour had also held at [27] that the relevant loan statement did not satisfy the conditions set out in s 8(1) of the Bills of Exchange Act and was, therefore, not a bill of exchange.

15 Section 8 of the Bills of Exchange Act provides relevantly:

(1) A bill of exchange is an unconditional order in writing, addressed by one person to another, signed by the person giving it, requiring the person to whom it is addressed to pay on demand, or at a fixed or determinable future time, a sum certain in money to or to the order of a specified person, or to bearer.

…

(3) An order to pay out of a particular fund is not unconditional within the meaning of this section; but an unqualified order to pay, coupled with:

(a) an indication of a particular fund out of which the drawee is to re-imburse himself or herself, or a particular account to be debited with the amount; or

(b) a statement of the transaction which gives rise to the bill;

is unconditional.

(4) A bill is not invalid by reason:

(a) that it is not dated;

(b) that it does not specify the value given, or that any value has been given therefore; or

(c) that it does not specify the place where it is drawn, or the place where it is payable.

16 Section 25 of the Bills of Exchange Act provides relevantly:

(1) Where a simple signature on a blank stamped paper stamped with an impress duty stamp is delivered by the signer in order that it may be converted into a bill, it operates as a prima facie authority to fill it up as a complete bill for any amount the stamp will cover, using the signature for that of the drawer or the acceptor or an indorser.

(2) And in like manner when a bill is wanting in any material particular, the person in possession of it has a prima facie authority to fill up the omission in any way he or she thinks fit.

17 The primary judge’s conclusion that the loan statement itself was not a bill of exchange within the meaning of the Bills of Exchange Act was plainly correct and is not challenged in the appeal.

18 The primary judge found that the loan statement was incapable of conversion to a bill of exchange because:

(1) It is not a “simple signature on a blank stamped paper”; and

(2) It is not “stamped with an impress duty stamp” apart from an Australian 5 cent stamp which either Mr Waden or the appellants appeared to have affixed themselves.

19 Mr Paalvast argued that the RAMS logo on the loan statement was a “simple signature”. We reject that argument.

20 The Macquarie Dictionary Online defines a signature relevantly to be:

1. a person's name, or a mark representing it, as signed or written by that person or by a deputy, as in subscribing a letter or other document.

21 Section 97 of the Bills of Exchange Act provides:

(1) Where, by this Act, any instrument or writing is required to be signed by any person, it is not necessary that he or she should sign it with his or her own hand, but it is sufficient if his or her signature is written thereon by some other person by or under his or her authority.

(2) In the case of a corporation, where, by this Act, any instrument or writing is required to be signed, it is sufficient if the instrument or writing be sealed with the corporate seal.

But nothing in this section shall be construed as requiring the bill or note of a corporation to be under seal.

22 In Muirhead v Commonwealth Bank of Australia (1996) 125 FLR 434, the Court of Appeal of Queensland held that, in the absence of any express provision or other indication to the contrary, s 97(1) of the Bills of Exchange Act is not to be taken to preclude signature by an agent. At 438, McPherson JA (Macrossan CJ and Davies JA agreeing on this issue) observed (quoting from Lord Denning’s dissenting judgment in Goodman v J Eban Ltd [1954] 1 QB 550) that the “great virtue of a handwritten signature…lies in the fact that no two persons write exactly alike, and so it carries on the face of it a guarantee that the person who signs has given his personal attention to it.” At 440, McPherson JA expressed approval of the statement in K Robson (ed) Riley’s Annotated Bills of Exchange Act and Cheques and Payment Orders Act that “signature” may perhaps be defined as the writing of a person’s name on a bill or notice in order to authenticate and give effect to some contract thereon. His Honour also referred to the United States Uniform Commercial Code definition of the term “signed” as including any symbol executed or adopted by a party with present intention to authenticate a writing, citing Brady on Bank Checks § 3.1, 4th ed (1969).

23 In Muirhead, McPherson JA also referred to the judgment of the Supreme Court of Ceylon, in Meyappan v Manchanayake [1961] LKCA 17; (1961) 62 NLR 529. In that case, the question was whether a cheque, upon the reverse of which had been placed a stamp of the name of the firm, had been signed by the firm. Samsoni J said (at 532):

The correct view, I think, is that unless there is added to the name so stamped a signature of a person verifying the so-called signature to show that it was placed there with the authority of the firm, the document cannot be regarded as validly signed. No case has gone so far as to hold that the mere stamping of the name of a firm, be it a company or a partnership, on a document is a valid signature by that firm.

24 In the context of s 25, the words “simple signature” refer to a mark which indicates that the document bearing the mark may be converted into a bill. In this case, there is nothing to indicate that the logo on the loan statement was intended to have that function. The mere reproduction of the logo on the loan statement, without more, does not perform that function and there is no other evidence suggesting that it was intended to perform that function. Accordingly, we agree with the primary judge that the loan statement does not satisfy the requirement in s 25 of “a simple signature on a blank stamped paper”. It follows that the loan statement was not a document capable of being converted into a bill of exchange.

25 Section 50(1) provides:

Subject to the provisions of this Act, a bill must be duly presented for payment. If it be not so presented, the drawer and indorsers shall be discharged.

26 Since there was no bill, her Honour was correct in concluding that s 50(1) had no application.

27 This is sufficient to dispose of ground 1 of the appeal. However, we also note that s 25 requires the relevant paper to be delivered “by the signer in order that it may be converted into a bill”. Even if the loan statement was signed, there was no evidence before the primary judge that it was delivered to Mr Waden with the intention of being converted into a bill of exchange. At the hearing of the appeal, Mr Paalvast argued that the loan statement was not expressed in a manner which excluded this intention. Further, he argued, if the bank did not have the relevant intention, it should have said so at the time and place nominated on the document and referred to at paragraph 4 of the primary judge’s Reasons. That argument is unsustainable. Mr Paalvast’s written submissions amply demonstrate that Mr Waden attempted to create a bill of exchange out of a loan statement, without reference to the bank. The bank never had any intention that the loan statement should be converted into a bill of exchange and the mere act of presenting the bank with a “filled up bill of exchange” did not cast any legal obligation upon the bank to deny an intention which it had never had or expressed.

28 At paragraph 15 of the appellants’ written submissions, Mr Paalvast sets out the propositions that he submits should have been adopted by the primary judge. However, none of those propositions survive scrutiny for the following reasons. Proposition (a) is that the loan statement was converted into a bill of exchange. For the reasons given above, this proposition cannot be accepted. Proposition (b) includes the claim that the loan statement is a “statement of a transaction” within the meaning of s 8(3)(b) of the Bills of Exchange Act. This contention is not raised by the Notice of Appeal but, in any event, does not assist the appellants because the loan statement does not “give rise” to any bill of exchange. Proposition (c) assumes the existence of a bill of exchange, and thus does not assist the appellants’ case. Proposition (d) merely describes the loan statement, albeit in contentious terms. The loan statement does not on its face require any payment. Propositions (e) and (f) assume the applicability of s 25 of the Bills of Exchange Act.

29 At paragraph 17 of the appellants’ written submissions, Mr Paalvast identifies five pieces of evidence said to have been unrebutted “or not properly considered”. The first item is a submission rather than evidence, the proposition being that Mr Waden had authority to “fill up” the “inchoate instrument” he received. For the reasons given above, s 25 conferred no authority on Mr Waden because he did not receive a document answering the description in s 25(1). The next propositions describe what Mr Waden did to create and deal with the purported bill of exchange. Precisely what Mr Waden did is of no moment because, whatever he did, he did not do it with the authority of the bank and therefore he was unable by any means to convert the loan statement into a bill of exchange affecting the bank.

30 We do not read the balance of the appellants’ written submissions to add materially to the case raised by ground 3 of the notice of appeal.

31 In reaching our conclusion, we do not find it necessary to consider the judgment in Bertola v Australian and New Zealand Banking Corporation [2014] FCA 609.

Grounds 2 and 4

32 In grounds 2 and 4 of the amended notice of appeal, the appellants complain that the primary judge denied them procedural fairness by hearing the proceeding on the papers.

33 Section 20A of the Federal Court of Australia Act 1976 (Cth) provides:

(1) This section applies in relation to any civil matter coming before the Court in the original jurisdiction of the Court.

(2) The Court or a Judge may deal with the matter without an oral hearing (either with or without the consent of the parties) if satisfied that:

(a) the matter is frivolous or vexatious; or

(b) the issue or issues on which determination of the matter depends have been decided authoritatively in the case law; or

(c) determination of the matter would not be significantly aided by an oral hearing because:

(i) there is no real issue of fact relevant to determination of the matter; and

(ii) the legal arguments in relation to the matter can be dealt with adequately by written submissions.

34 On 27 June 2014, the primary judge conducted a directions hearing in the matter at which the question of whether an oral hearing of the proceeding would be held was raised. Mr Paalvast was present at the hearing. Her Honour expressed the view that “this could well be a matter that could be determined on the papers and I think it could well be helpful to have that happen”. Her Honour said that she was “not quite clear as to exactly what the case is” for the applicants and she wanted to see “a clear, concise, five page maximum, written submission that sets out [the applicants’] case”. The following exchange then took place:

HER HONOUR: It would be a lot easier for you to do, I think, in writing, than perhaps orally. If I need further assistance, I will let you know and I will call an oral hearing. If I feel that I don’t need further assistance because I understand the argument that you put in writing, then I will make that decision on the papers. Are you content with that course?

MR PAALVAST: I will be, yes.

35 There was some discussion about submissions in reply which finished with the following exchange:

HER HONOUR: Two weeks for your written submissions in answer and then a further seven days for you to put on a maximum of two pages in reply, if you need to. Okay. If you don’t need to, you can notify my associate that you don’t wish to file any further material.

MR PAALVAST: Okay.

HER HONOUR: But if you do, then you will have a further seven days in which to put on two pages in reply.

MR PAALVAST: Yes.

HER HONOUR: And then I will have a look at that and let the parties know if I need any further assistance.

MR PAALVAST: That sounds fair and reasonable.

36 Mr Paalvast then expressed the following concern:

MR PAALVAST: The only concern I have, as a layman, is that sometimes we’ve been putting in submissions and they have been ignored totally.

37 After some more interchange, there was the following:

HER HONOUR: If it will be helpful to the court, if you wish to file the relevant pages of the authorities that you rely upon highlighted, that would be of assistance and it doesn’t count as part of your five pages.

MR PAALVAST: That’s what I was after. Thank you.

38 Having regard to the transcript set out above, we reject Mr Paalvast’s contention at paragraph 8 of his written submissions that the appellants “never agreed to any hearing proceeding on the papers”.

39 After submissions were filed in accordance with her Honour’s directions, her Honour notified the parties on 18 August 2014 that she intended to deliver judgment on 19 August 2014 (Wilmink (No 2) at [1]). By email sent to the Court at 2:15am on 19 August 2014, Mr Paalvast said that “[o]n reflection, I would appreciate the opportunity to be present in court when and before judgment is due and hopefully to be able to make some final oral submissions.”

40 Her Honour’s Reasons reveal that she was satisfied that determination of the matter would not be significantly aided by an oral hearing because the requirements of s 20A(2)(c) were satisfied. This is not a case where it was necessary to assess credibility or differing versions of events. The questions concerned the proper characterisation of the purported bill of exchange, including the proper construction of the Bills of Exchange Act. In our view, it was open to her Honour to conclude that an oral hearing was not required.

41 In our view, the primary judge did not deny Mr Paalvast procedural fairness in delivering her judgment without an oral hearing. Mr Paalvast accepted on 27 June 2014 that the primary judge could decide whether to hold an oral hearing by reference to the written submissions. His email dated 19 August 2014 makes it clear that he was seeking to change his position, after being notified that the judgment would be delivered that day.

42 Mr Paalvast submitted that an oral hearing would have permitted the appellants to clarify that the “Waden debt” had been “discharged if not extinguished as a matter of ‘adequacy of consideration’: with a lawfully negotiated bargained for consideration, payment legitimately tendered under the doctrine of ‘accord and satisfaction’ to the tenor accepted, being certified as being one of…”. In our view, this clarification of the appellants’ contentions would not have advanced their case. Even assuming that state of affairs, the appellants’ argument was bound to fail because the purported bill of exchange was not a bill of exchange.

43 Having been given an opportunity to file submissions in reply, and having chosen not to do so, procedural fairness did not require Mr Paalvast to be given an opportunity to make oral submissions.

44 From her Honour’s observations at [33] and [37] of her Reasons in Wilmink (No 1), we also conclude that her Honour was satisfied that the matter was either frivolous or vexatious. That satisfaction provided a further reason why her Honour was entitled to proceed without an oral hearing.

45 Accordingly, grounds 2 and 4 of the appeal fail.

Costs

46 The appeal will be dismissed with costs.

Other matters

47 At the hearing of the appeal, Mr Paalvast described the conduct underlying the appellants’ claim as “extremely cheeky”. That euphemism is inapt, because it fails to recognise the significant costs involved to both the bank and the Court of litigating the claim. Before the hearing in this Court, Mr Paalvast was on notice that the primary judge had regarded the claim as between misguided and disingenuous. He was aware that a similar argument was rejected by the Federal Magistrates Court in Deputy Commissioner of Taxation v Sproule [2012] FMCA 1188 and that the learned Federal Magistrate had described Mr Sproule’s proposed use of a bill of exchange as “either a complete misunderstanding of the use of the instrument or some cynical ploy to avoid the debt”. He was aware that a similar claim had been dealt with summarily in Bertola. He was aware that Jagot J had described submissions on a similar argument in Atkinson as “obscure, impenetrable, hopeless nonsense” and that she had ordered that those proceedings be dealt with without an oral hearing because she was satisfied that the matter was frivolous and vexatious. The limited resources of the Court should not have been spent on the disposition of this appeal.

48 The Court will refer this proceeding and certain other proceedings to the Registrar to consider whether to apply for a vexatious proceedings order.

I certify that the preceding forty-eight (48) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justices Foster, Yates and Gleeson. |

Associate: