FEDERAL COURT OF AUSTRALIA

Wenkart v Pantzer [2013] FCAFC 81

| IN THE FEDERAL COURT OF AUSTRALIA | |

| BETWEEN: | THOMAS RICHARD WENKART Appellant |

| AND: | WARREN PANTZER - FORMER TRUSTEE OF THE ESTATE OF THOMAS RICHARD WENKART First Respondent HAPDAY HOLDINGS PTY LIMITED (ACN 001 185 253) Second Respondent |

| AND BETWEEN: | WARREN PANTZER – FORMER TRUSTEE OF THE ESTATE OF THOMAS RICHARD WENKART Cross-Appellant in the First Cross-Appeal |

| AND: | THOMAS RICHARD WENKART First Cross-Respondent in the First Cross-Appeal HAPDAY HOLDINGS PTY LIMITED (ACN 001 185 253) Second Cross-Respondent in the First Cross-Appeal |

| AND BETWEEN: | HAPDAY HOLDINGS PTY LIMITED (ACN 001 185 253) Cross-Appellant in the Second Cross-Appeal |

| AND: | THOMAS RICHARD WENKART First Cross-Respondent in the Second Cross-Appeal WARREN PANTZER – FORMER TRUSTEE OF THE ESTATE OF THOMAS RICHARD WENKART Second Cross-Respondent in the Second Cross-Appeal |

| DATE OF ORDER: | |

| WHERE MADE: |

THE COURT ORDERS THAT:

1. By 9 August 2013, Warren Pantzer file and serve Short Minutes of Declarations and Orders which he proposes in order to give effect to the Reasons for Judgment of the Full Court published this day together with a Written Submission of no more than six (6) pages in length in which he explains the basis for his proposed declarations and orders (including all necessary calculations) and supports that proposal to the extent that he may be advised.

2. By 23 August 2013, Dr Wenkart and Hapday Holdings Pty Limited (Hapday) each file and serve a Written Submission of no more than six (6) pages in length in which they make such submissions as they may be advised in answer to Mr Pantzer’s submissions and proposed declarations and orders.

3. By 27 August 2013, Mr Pantzer file such Reply Submission (if any) as he may be advised to make in answer to Dr Wenkart’s and Hapday’s submissions, such submission not to exceed three (3) pages in length.

4. Thereafter, the form of Declarations and Orders is to be determined on the papers.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

| NEW SOUTH WALES DISTRICT REGISTRY | |

| GENERAL DIVISION | NSD 26 of 2011 |

| ON APPEAL FROM THE FEDERAL COURT OF AUSTRALIA |

| BETWEEN: | THOMAS RICHARD WENKART Appellant |

| AND: | WARREN PANTZER - FORMER TRUSTEE OF THE ESTATE OF THOMAS RICHARD WENKART First Respondent HAPDAY HOLDINGS PTY LIMITED (ACN 001 185 253) Second Respondent |

| AND BETWEEN: | WARREN PANTZER – FORMER TRUSTEE OF THE ESTATE OF THOMAS RICHARD WENKART Cross-Appellant in the First Cross-Appeal |

| AND: | THOMAS RICHARD WENKART First Cross-Respondent in the First Cross-Appeal HAPDAY HOLDINGS PTY LIMITED (ACN 001 185 253) Second Cross-Respondent in the First Cross-Appeal |

| AND BETWEEN: | HAPDAY HOLDINGS PTY LIMITED (ACN 001 185 253) Cross-Appellant in the Second Cross-Appeal |

| AND: | THOMAS RICHARD WENKART First Cross-Respondent in the Second Cross-Appeal WARREN PANTZER – FORMER TRUSTEE OF THE ESTATE OF THOMAS RICHARD WENKART Second Cross-Respondent in the Second Cross-Appeal |

| JUDGES: | DOWSETT, MCKERRACHER AND FOSTER JJ |

| DATE: | 30 JULY 2013 |

| PLACE: | SYDNEY |

TABLE OF CONTENTS

| [1] | |

| THE SETTING FOR THE PROCEEDINGS BELOW (NSD 7051 OF 2002) | [23] |

| A BRIEF HISTORY OF THE PROCEEDINGS BELOW (NSD 7051 OF 2002) | [47] |

| The Early Period | [47] |

| The Trustee’s Motion to Enforce the Charge over the Paddington Property and the Subsequent Applications | [71] |

| THE RELEVANT JUDGMENTS OF BRANSON J | [120] |

| Branson No 1 | [120] |

| Branson No 2 | [129] |

| Branson No 3 | [148] |

| THE JUDGMENTS OF FLICK J | [156] |

| Flick No 1 | [156] |

| Flick No 2 | [160] |

| Flick No 3 | [183] |

| Flick No 4 | [193] |

| THE ISSUES IN THE APPEAL AND THE CROSS-APPEALS | [194] |

| Dr Wenkart’s Appeal | [194] |

| The Trustee’s Cross-Appeal | [198] |

| Hapday’s Cross-Appeal | [206] |

| THE MEANING AND EFFECT OF THE CONSENT ORDERS DATED 11 MARCH 2002 | [211] |

| DR WENKART’S APPEAL | [242] |

| Issue 1—No Debt to Support an Order for the Appointment of a Trustee for Sale | [242] |

| Dr Wenkart’s Submissions | [242] |

| Hapday’s Submissions | [252] |

| The Trustee’s Submissions | [253] |

| Discussion | [256] |

| Issue 2—Was the Trustee’s Remuneration Finally Fixed at the Annulment Meeting | [294] |

| Issue 3—The Trustee’s Entitlement to Post-Annulment Remuneration and Expenses | [303] |

| Issue 4—Unreasonable Conduct | [310] |

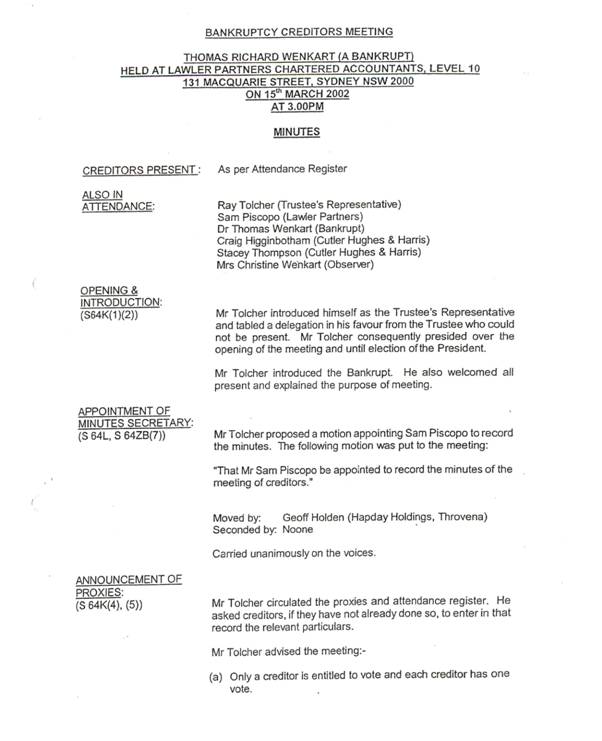

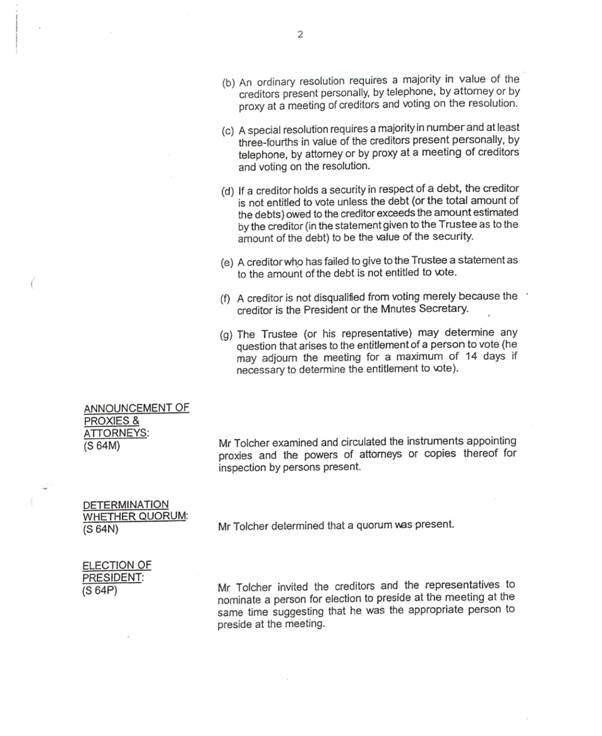

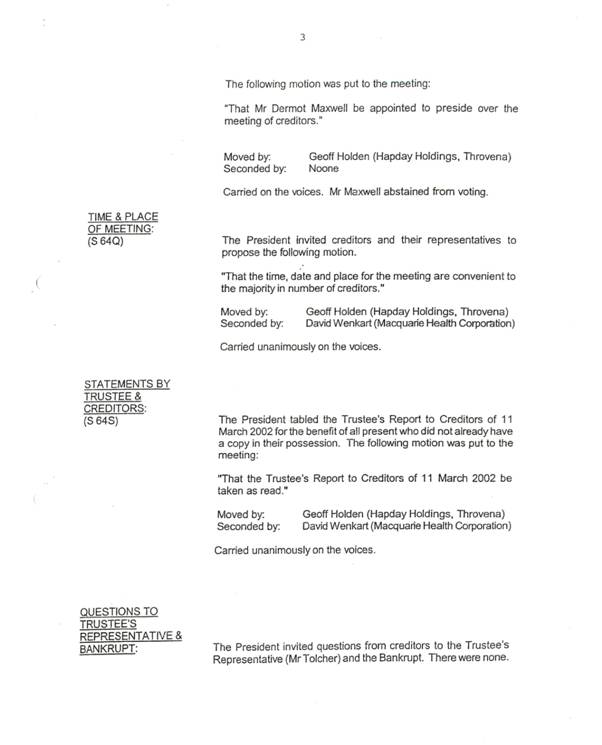

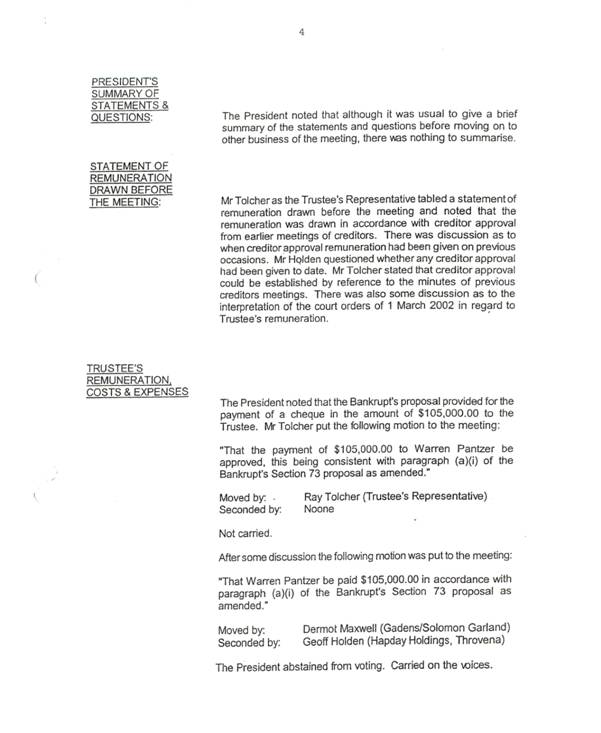

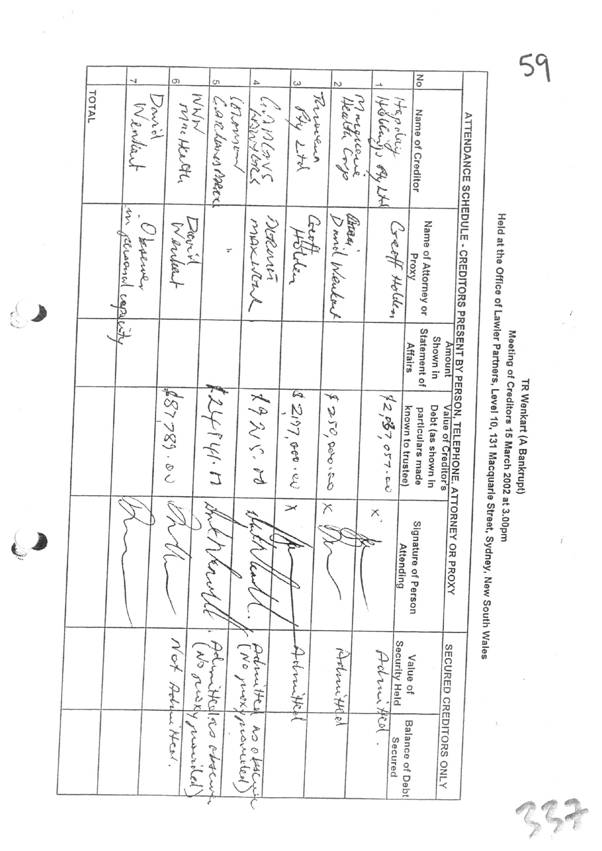

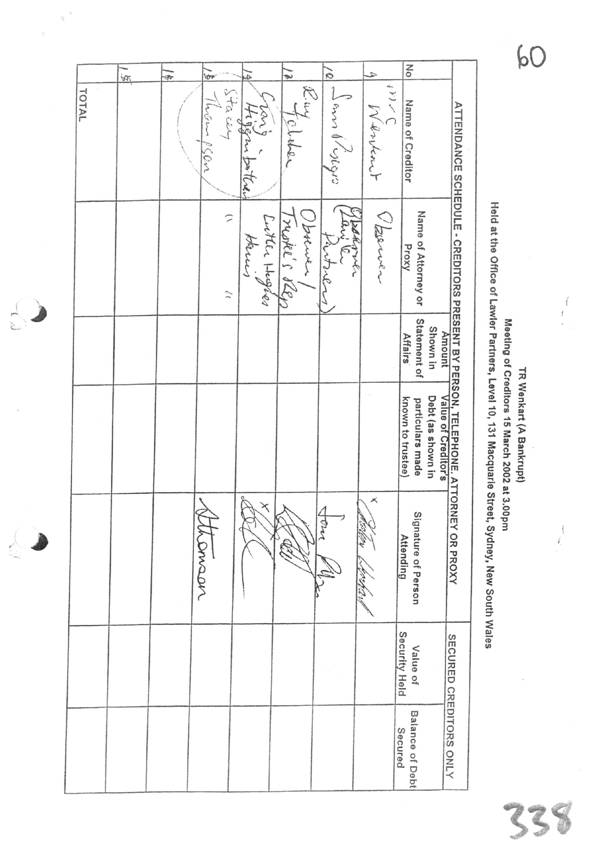

| Issue 5—The Trustee’s Failure to Prove his Entitlements | [312] |

| Issue 6—The Procedural Errors and Delays | [332] |

| Issue 7—Declaratory Relief | [340] |

| THE TRUSTEE’S APPLICATION TO REOPEN | [345] |

| OTHER MATTERS | [347] |

| Interest | [347] |

| Costs | [351] |

| The Proceeds of Sale Issue | [356] |

| CONCLUSIONS | [359] |

REASONS FOR JUDGMENT

THE COURT:

Introduction

1 The estate of Dr Thomas Richard Wenkart, who is the appellant in the present Appeal (NSD 26 of 2011) and the first cross-respondent in both of the Cross-Appeals, was sequestrated on 28 October 1999 by order of this Court.

2 Warren Pantzer, a Chartered Accountant, was appointed as Dr Wenkart’s trustee in bankruptcy. Mr Pantzer is the first respondent in Dr Wenkart’s Appeal, the cross-appellant in the First Cross-Appeal and the second cross-respondent in the Second Cross-Appeal. We shall hereinafter refer to Mr Pantzer as the trustee.

3 The other party to the matters presently before this Full Court is Hapday Holdings Pty Limited (Hapday). Hapday is a corporation associated with Dr Wenkart. At all relevant times, Hapday held a first registered mortgage over a residential property known as “47 Union Street, Paddington, NSW” (the Paddington property). At all relevant times, Dr Wenkart was the registered proprietor of the Paddington property. The Paddington property was charged by Dr Wenkart in favour of the trustee in order to secure Dr Wenkart’s obligations under an arrangement reached with the trustee on 11 March 2002.

4 Hapday is the second respondent in the appeal, the second cross-respondent in the First Cross-Appeal and is the cross-appellant in the Second Cross-Appeal. As already mentioned, the cross-respondents in the Second Cross-Appeal are Dr Wenkart and the trustee.

5 Dr Wenkart’s bankruptcy was annulled on 15 March 2002 (the annulment date) by resolution of his creditors passed on that day (see s 73(4) and s 74(5) of the Bankruptcy Act 1966 (Cth) (the Bankruptcy Act)).

6 During Dr Wenkart’s bankruptcy, the trustee was involved in litigation concerning several proofs of debt which he had rejected and the recovery of payments made by Dr Wenkart which the trustee contended were preferences. Throughout the bankruptcy, the trustee was advised and represented by the law firm, Cutler Hughes & Harris (CHH). CHH ceased acting for the trustee immediately after the annulment meeting. For some time thereafter, Sally Nash & Co acted for the trustee.

7 As at the annulment date, the trustee claimed:

(a) Approximately $220,000 as unpaid trustee’s remuneration. In the period up to late December 2000, the trustee had already paid various amounts to himself and to the firm of accountants with which he was associated out of the bankrupt estate of Dr Wenkart. The total of those amounts was $226,454.70.

(b) Approximately $260,000 as unpaid trustee’s costs, charges and expenses. We shall refer to these types of outlays as trustee’s expenses. The amount of $260,000 (approx) was claimed as unpaid fees and disbursements due to CHH. As was the case in respect of the trustee’s own remuneration, in the period up to late December 2000, the trustee had made a number of payments to CHH and to Counsel retained by CHH on his behalf. Those payments totalled $249,942.29.

8 By late December 2001, Dr Wenkart was very keen to have his bankruptcy annulled. On 18 January 2001, he had submitted a concrete compromise proposal to the trustee pursuant to s 73 of the Bankruptcy Act. This followed an earlier proposal which he had submitted on 9 March 2000. By late December 2001, he had settled with his creditors but had not accepted the trustee’s claims concerning the trustee’s unpaid remuneration and expenses. In the period from late October 2001 to early March 2002, CHH and Hunt & Hunt, the law firm retained by Dr Wenkart and his corporate associates, had exchanged correspondence and had had discussions in an endeavour to resolve the trustee’s claims. Those exchanges and discussions had not produced an agreement.

9 As at early March 2002, Dr Wenkart and his corporate associates were well aware that the trustee had no funds in his hands with which to pay his unpaid remuneration and expenses.

10 On 15 February 2002, Dr Wenkart wrote directly to Beaumont J requesting that his Honour compel the trustee to call a meeting of his creditors for the purpose of considering his annulment proposal. His Honour treated this correspondence from Dr Wenkart as the filing of an initiating process. The proceeding thereby commenced was allocated plaint No. NSD 7051 of 2002. Proceeding NSD 7051 of 2002 (the proceedings below) is the proceeding in which all of the orders which are challenged in the present Appeal and in the two Cross-Appeals were made.

11 On 1 March 2002, Beaumont J made orders requiring the trustee to convene a meeting of Dr Wenkart’s creditors by no later than 15 March 2002.

12 On 11 March 2002, Beaumont J noted an agreement which had, by then, been reached among Dr Wenkart, Hapday and the trustee. That agreement provided that, post-annulment, Dr Wenkart would assume personal responsibility for the payment of the trustee’s lawful entitlement to remuneration and expenses and that Dr Wenkart’s obligation to do so would be secured by an equitable charge granted by him over the Paddington property.

13 At noted at [5] above, on 15 March 2002, by resolution of his creditors, Dr Wenkart’s bankruptcy was annulled.

14 The annulment of Dr Wenkart’s bankruptcy triggered a series of disputes between Dr Wenkart and the trustee concerning the trustee’s conduct in administering Dr Wenkart’s estate and the remuneration and expenses which he claimed for administering that estate. Those disputes have been ongoing since 2002. The litigation between Dr Wenkart and the trustee since 2002 has been confined to attempts by the trustee to be paid his remuneration and expenses (both in respect of his administration of the estate during the period of the bankruptcy and in respect of his recovery attempts post-annulment) and Dr Wenkart’s unwavering resistance by any and all means available to him (whether reasonable or not) to making any payments whatsoever to the trustee. Despite its confined scope and subject matter, the litigation between Dr Wenkart and the trustee post-annulment has so far led to the delivery of 19 judgments by single judges of this Court, three judgments by Full Courts of this Court and one set of reasons and a Certificate by a Registrar of this Court. There have been two applications to the High Court for special leave to appeal, one of which was discontinued and the other of which was refused. This litigation was justifiably described as “scandalous” by Flick J at 642–643 [5]–[6] in his judgment delivered on 13 August 2010 (Wenkart v Pantzer (2010) 269 ALR 641; [2010] FCA 866).

15 Dr Wenkart has taken every point available to him to challenge the trustee’s claims for remuneration and expenses. He has attempted to compel the trustee to tax his remuneration under the Bankruptcy Act and the Bankruptcy Regulations 1996 (Cth) (the Bankruptcy Regulations) and to require CHH to tax its unpaid fees and disbursements pursuant to s 167 of the Bankruptcy Act.

16 On 31 October 2002, having not received satisfaction from Dr Wenkart, the trustee filed a Notice of Motion in the proceedings below. By that Notice of Motion, the trustee sought the appointment of himself as trustee for the sale of the Paddington property and ancillary relief. That Notice of Motion was subsequently ordered to stand as a Cross-Claim for substantive relief in the proceedings below.

17 The filing of the trustee’s Cross-Claim spawned a plethora of litigation. In three judgments delivered in 2007 and 2008, Branson J endeavoured to bring this unfortunate litigation to an end. Her Honour did not succeed in doing so.

18 By four judgments delivered in 2009 and 2010, Flick J brought the proceedings below to an end. On 24 December 2010, his Honour made the following orders:

THE COURT:

1. Declares that the First Respondent is lawfully entitled to be paid the sum of $173,079.71 by the Applicant.

2. Orders that the Applicant pay interest on the sum of $173,079.71 from 16 September 2008 pursuant to section 51A of the Federal Court of Australia Act 1976 (Cth), such interest calculated as $32,682.75.

3. Subject to the order made in paragraph 11 of these orders, orders that the Applicant pay 90% of the First Respondent’s costs of these proceedings as taxed on a party/party basis (noting that this order does not vary existing orders of this Court as to costs).

4. Orders that judgment be entered for the First Respondent against the Applicant in the sum of $205,762.46, including interest.

5. Declares that upon the issue of a certificate of taxation by a taxing officer under section 167 of the Bankruptcy Act 1966 and/or Bankruptcy Regulation 8.09 in respect of any claim for remuneration in relation to the estate in bankruptcy of the Applicant for the period after 21 October 2003, the First Respondent will be lawfully entitled to payment of such amounts.

6. Declares that upon the issue of a certificate of taxation by a taxing officer under section 167 of the Bankruptcy Act 1966 and/or Bankruptcy Regulation 8.09 in respect of legal services provided by Cutler Hughes & Harris to the First Respondent in relation to the estate in bankruptcy of the Applicant (such legal services not being the subject of the certificate of taxation issued on 17 February 2003), the First Respondent will be lawfully entitled to payment of such amounts.

7. Declares that upon the issue of a certificate of taxation by a taxing officer under section 167 of the Bankruptcy Act 1966 and/or Bankruptcy Regulation 8.09 in respect of legal costs and other expenses incurred by the First Respondent in relation to the estate in bankruptcy of the Applicant since 21 October 2003 not covered by the orders in paragraphs 3 and 11 of these orders, the First Respondent will be lawfully entitled to payment of such amounts.

8. Orders pursuant to Order 37 of the Federal Court Rules and section 30 of the Bankruptcy Act 1966, as amended, in aid of the order and agreement made on 11 March 2002 in these proceedings, that if the judgment entered pursuant to the order in paragraph 4 of these orders is not satisfied within 28 days of entry:

8.1 David Young, official liquidator be appointed as trustee (“the trustee”) for sale of the whole of the land and improvements in certificate of title folio identifier G/33817 known as 47 Union Street, Paddington (“the property”) for the purpose of realising the property to enable payment to the First Respondent of the amounts to which the First Respondent is lawfully entitled to payment or becomes lawfully entitled on the issue of certificates of taxation.

8.2 Directs that the Second Respondent and the Applicant forthwith deliver to the trustee for the purpose of the sale of the property certificate of title folio identifier G/33817 and a discharge of mortgage 3965299 in registrable form.

8.3 Orders that the Applicant forthwith give the trustee vacant possession of the property.

8.4 Orders that a writ of possession of the property issue 28 days after the date of this order.

8.5 Orders that the trustee have the following powers:

(a) To sell the property by public auction after marketing it for not less than 4 weeks in a manner recommended by a real estate agent retained by the trustee to procure the sale of the property.

(b) To set a reserve.

(c) To negotiate with the two highest bidders if the property is passed in at the public auction.

(d) To sell by private treaty (or public auction again) if the property is passed in and there is no negotiated sale.

(e) To act and do all things in a manner appropriate to a trustee for sale in the marketing and sale of the property.

(f) To sign a transfer and all other documents required to convey good title to the property.

(g) To forthwith deduct and pay from the proceeds of sale:

(i) the commission and other expense of any real estate agent retained by the trustee to procure the sale of the property;

(ii) the legal expenses of the trustee in respect of the sale of the property;

(iii) the other costs, expenses and outgoings (including rates and taxes charged on the property) of transferring the property to the purchaser; and

(iv) the remuneration and expenses of the trustee and his employees incurred in relation to the sale of the property;

8.6 Directs that the trustee pay any surplus to the Second Respondent after he has accounted for all of the monies referred to in these orders.

8.7 Directs that the trustee file with the Court and serve on the Applicant and the Second Respondent an affidavit deposing to his receipts and payments as trustee for sale of the property on or before the later of 60 days from completion of the sale of the property and the date of payment of the surplus pursuant to the direction in paragraph 8.6 of these orders.

9. Orders that the Notice of Motion filed by the First Respondent on 23 November 2010 is dismissed.

10. Orders that the Notice of Motion filed by the Applicant on 23 November 2010 is dismissed.

11. Orders that there be no order as to costs in respect of the issues canvassed during the hearings on 28 October, 18 November and 23 November 2010.

12. Orders that the Second Respondents (Hapday Holdings Pty Ltd, Macquarie Health Corporation Ltd and Throvena Pty Ltd) bear their own costs of the proceedings.

19 Dr Wenkart appealed from those orders. Each of the trustee and Hapday filed a Cross-Appeal from those orders. In addition, the trustee sought to challenge an earlier order made by Branson J on 16 September 2008.

20 In January 2011, Dr Wenkart paid the judgment debt of $205,762.46 to the trustee. For that reason, Order 8 made by Flick J on 24 December 2010 has not been activated. In his Appeal, Dr Wenkart seeks an order for the refund of that amount.

21 To some extent, the reasons which Flick J gave for making the final orders incorporate reasons given by Branson J in the judgments which her Honour delivered in 2007 and 2008. In this way, there are challenges in the present Appeal and Cross-Appeals to her Honour’s reasoning in those judgments even though the relief which is under attack is, with one exception, the relief granted by Flick J on 24 December 2010.

22 Before we explain the judgments appealed from and set out the issues which arise for determination in the Appeal and in the Cross-Appeals, it is necessary to provide a chronological account of the parties’ relevant dealings and of the important milestones in the proceedings below. We now turn to provide that account.

The Setting for the Proceedings Below (NSD 7051 of 2002)

23 On 9 March 2000, Dr Wenkart lodged with the trustee a composition proposal pursuant to s 73 of the Bankruptcy Act. That proposal was not progressed at that time.

24 In the period from early December 1999 to 31 July 2000, the trustee made four Reports to Creditors.

25 At the first meeting of creditors, which was held on 13 December 1999, the creditors approved remuneration for the trustee as follows:

(a) $60,744.30 in respect of the period from 28 October 1999 to 10 December 1999; and

(b) Future anticipated remuneration of $80,000.

26 On 1 February 2000, the trustee paid the first tax invoice rendered to him by CHH.

27 As at 17 March 2000, the trustee had been paid $136,672.80 by way of remuneration and $4,474.05 as expenses. In addition, legal fees totalling $15,868.48 had been paid to CHH.

28 At the third meeting of creditors, which was held on 29 March 2000, the creditors approved remuneration for the trustee as follows:

(a) $11,811.40 in respect of the period from 11 March 2000 to 28 March 2000; and

(b) Future remuneration of $68,188.60.

29 On 18 August 2000, Alan Pitman, who claimed to be a creditor of Dr Wenkart, commenced proceeding NSD 7752 of 2000 against the trustee seeking, pursuant to s 104 of the Bankruptcy Act, review of the trustee’s decision to reject part of the Proof of Debt lodged by Mr Pitman against the estate of Dr Wenkart.

30 As at 19 December 2000, the trustee had received $528,216.75 and paid out $504,674.11 in his capacity as trustee of Dr Wenkart’s bankrupt estate. Included within the total paid by the trustee were the following expenses:

| (a) | General legal fees (paid to CHH) | $223,945.54 |

| (b) | Litigation (legal) fees (paid to CHH) | $25,996.75 |

| (c) | Trustee’s remuneration (paid to the trustee) | $220,744.30 |

| TOTAL | $470,686.59 |

Included within the total amount received by the trustee were three non-recourse litigation loans totalling $345,000 and a preference recovery of $150,000.

31 As at 19 December 2000, the trustee held the amount of $23,542.84 as surplus funds in Dr Wenkart’s estate.

32 In late December 2000, the amount of total receipts, details of payments made by the trustee and the quantum of surplus funds held by the trustee were conveyed to Dr Wenkart and those creditor corporations associated with him (Throvena Pty Ltd (Throvena), Hapday and Macquarie Health Corporation Limited (MHC)).

33 On 22 December 2000, the Petitioning Creditors who had filed the Creditor’s Petition pursuant to which Dr Wenkart had been made bankrupt (G Abignano and Genallco Pty Limited) Hapday, Throvena and MHC, entered into an arrangement whereby the claims of the Petitioning Creditors were resolved on a final basis. The consequence of these arrangements was that Mr Pitman was released by G Abignano and Genallco Pty Limited from any liability which he had to them under complex indemnity arrangements involving Dr Wenkart, Mr Pitman, those corporations and others. That release resulted in Mr Pitman no longer being a creditor of Dr Wenkart, if he ever had been. He was thereafter not entitled to prove in Dr Wenkart’s bankruptcy.

34 Proceeding NSD 7752 of 2000 was, for all practical purposes, finally determined on 21 February 2002 when Beaumont J made a declaration that Mr Pitman had been effectively released from any liability which he might have had to Mr Abignano and Genallco Pty Limited. That release was the consequence of the settlement arrangements reached on 22 December 2000 and consummated in 2001. Between 18 August 2000 and 21 February 2002, proceeding NSD 7752 of 2000 had been used as the vehicle for resolving a number of issues concerning Dr Wenkart’s bankruptcy.

35 On 18 January 2001, Dr Wenkart submitted a revised proposal to the trustee for an arrangement pursuant to s 73 of the Bankruptcy Act. That proposal involved the payment in full of those creditors of Dr Wenkart who were not associated with or related to him and agreements to pay related creditors a relatively small proportion of the total sums due to them. All of the related creditors consented to the proposal then being advanced by Dr Wenkart.

36 The s 73 proposal propounded by Dr Wenkart in his letter dated 18 January 2001 required that two bank cheques, each in the amount of $105,000, be given to the trustee at or immediately before the creditors’ meeting contemplated by the proposal. It was intended at that time that there be a meeting of Dr Wenkart’s creditors on 31 January 2001. The first of those cheques was described as covering the balance of the trustee’s remuneration up to the conclusion of the creditors’ meeting to be called to consider Dr Wenkart’s s 73 proposal and its implementation. The second amount, less the cash then held by the trustee at that time (estimated to be $24,000), was required to be used to discharge the trustee’s liability to CHH for legal fees up to and including the conclusion of the s 73 meeting and its implementation. Additional bank cheques were to be made available in order to discharge the commitments to most of Dr Wenkart’s remaining creditors made by Dr Wenkart in his proposal. At that time, it was expected that the s 73 meeting would be held on 31 January 2001 and that the resolutions passed at that meeting would be implemented shortly thereafter.

37 The trustee was unable to put Dr Wenkart’s s 73 proposal to Dr Wenkart’s creditors in January 2001 because Mr Pitman had obtained an interlocutory injunction restraining the trustee from putting that proposal to Dr Wenkart’s creditors pending the determination of his (Mr Pitman’s) appeal against the trustee’s rejection of part of his proof of debt.

38 By letter dated 30 November 2001, Hunt & Hunt Lawyers, who were then acting on behalf of Dr Wenkart and his associates, requested CHH to provide to them details of the trustee’s costs in respect of the proceedings which had been brought against him by Mr Pitman (NSD 7752 of 2000).

39 By letter dated 4 December 2001, CHH informed Hunt & Hunt that the trustee’s unpaid remuneration and expenses were as follows:

| A. | Trustee’s remuneration These figures do not include any realisations and interest charges or GST payable that may become due or other possible liabilities such as insurance | $183,875.11 |

| B. | Anticipated Trustee Costs and Expenses – to finalise all matters in the bankrupt estate in the event that all costs, expenses and remuneration are paid as at 30 November 2001 | $8,600.00 |

| C. | Trustee’s Legal Fees and Disbursements – as at 30 November 2001 | $247,103.62 |

| D. | Total Further Anticipated Legal Fees and Disbursements – depending on terms of s73 proposal and date of acceptance | $3,000 to unknown $ |

| Total Costs of Administration | $442,578.73 | |

| – in the event that a s 73 proposal goes ahead which excludes any dispute as to the trustee’s entitlement for full remuneration and payment of his full costs and expenses as set out above. | ||

40 CHH made clear in its letter dated 4 December 2001 that the total of the unpaid costs of the administration up to and including the anticipated finalisation of the s 73 proposal advanced by Dr Wenkart was likely to be $442,578.73. That figure included the trustee’s remuneration and all legal fees and disbursements actually incurred by him in the administration of Dr Wenkart’s bankrupt estate up to 30 November 2001 which remained unpaid as at that date. The letter was not concerned with the trustee’s remuneration and expenses which had already been paid.

41 Between 4 December 2001 and 25 January 2002, CHH and Hunt & Hunt corresponded concerning the costs of administration claimed by the trustee in CHH’s letter dated 4 December 2001. No agreement was reached in that period between the Wenkart interests and the trustee in respect of the claims for remuneration and expenses made by the trustee in CHH’s letter dated 4 December 2001. However, one matter was quite clear: As at 8 January 2002, neither Dr Wenkart nor his creditors had requested the trustee to require CHH to tax its fees and disbursements. In their letter to CHH dated 8 January 2002, Hunt & Hunt requested one or more itemised Bills of Costs from CHH so that their clients could decide whether to press their request for taxation. On the last page of that letter, in par 3, Hunt & Hunt said:

Once we have received an itemised bill, the creditors will decide whether to proceed to a taxation of the Bill of Costs.

42 However, by letter dated 16 January 2002 from the trustee to Hunt & Hunt, the trustee said (omitting formal parts):

Re: Warren Pantzer as Trustee of the Bankrupt Estate of

Dr Thomas Richard Wenkart ats Pitman

I refer to your facsimile sent to Ms Gibson at Cutler Hughes and Harris dated 8 January 2002. I do not propose, in this facsimile, to address the baseless allegations made by you in relation to the administration of the bankrupt’s estate other than to deny them.

However, and in relation to the issue of any remuneration and costs and expenses, I make the following comments:

1. I agree that my remuneration shall be fixed in accordance with regulation 8.08 of the Bankruptcy Regulations;

2. My solicitors did not state in their facsimile to you of 11 December 2001 that an itemised Bill of Costs had been provided by it to the creditors. My solicitor’s statement was that the Trustee

“… will provide an itemised Bill of Costs (as provided by Cutler Hughes and Harris) to the Creditors; …”

I have been issued with legal Bills of Costs in relation to the estate for work up to November 2001. My solicitors are currently preparing Memoranda of Fees in relation to the work done since that date. The Bill of Costs which I have received, are of course, available for inspection by the creditors at any time.

Please find enclosed copies of the bills with which have already been issued. Upon receipt of the Bills of Costs from Cutler Hughes and Harris relating to work done from November 2011 I will provide you with those copies.

As previously offered by my solicitors, all files are available for inspection. Please make any arrangement for inspection of the files with Mr Higginbotham of Cutler Hughes and Harris. Any inspection would of course at this stage by [sic] subject to the contents of any legal advice not being disclosed.

Would you please confirm that your clients still require a taxation of those bills.

In the event that your clients require taxation of the bills, would you please indicate:

(a) Which creditor will provide me with the costs of making an application for taxation of the bills; and

(b) Which creditor will undertake to provide payment of those costs or provide me with security for the payment of those costs.

by return letter.

43 The copy Bills of Costs rendered by CHH referred to in this letter were not, in fact, enclosed with the letter.

44 On 25 January 2002, CHH sent a letter to Hunt & Hunt. This letter is not yet in evidence. The trustee sought to tender it before Branson J but her Honour rejected it. The trustee complains about this in his Cross-Appeal and seeks leave to reopen in order to have this letter and two other documents admitted into evidence. In his submissions in support of his application to reopen, the trustee confined himself to the tender of the letter dated 25 January 2002. We intend to admit that letter into evidence and will explain why later in these Reasons. It is appropriate to refer to the 25 January 2002 letter at this point in the chronology. Omitting formal parts, that letter was in the following terms:

We refer to the writer’s discussions with Ms Leis on Friday, 18 January 2002.

On 24 October 2001 your clients made an open offer in relation to security for the Trustee’s remuneration and costs. The terms of that offer were refined by our client in our facsimile to you of 11 December 2001.

We note that despite further facsimiles from us, no final offer has been agreed or accepted by your clients or the Bankrupt.

After the Court hearing on Monday, 21 January 2002 Mr Robb, QC (appearing on behalf of our client) spoke directly with Mr Chippendall who appeared on behalf of your clients. It was agreed between Counsel that they would speak again within the next few days with a view to resolving the issue as to payment of a portion of the Trustee’s remuneration, costs and expenses and the granting of security to the Trustee by the Bankrupt for the balance of the Trustee’s remuneration, costs and expenses.

Mr Robb, QC then spoke with Dr Wenkart. During that conversation Mr Robb, QC expressed a view there had developed a considerable misunderstanding between Dr Wenkart, his associated entities and the Trustee in relation to the Pitman proceedings and the administration of the estate. Mr Robb, QC told Dr Wenkart of his arrangement with Mr Chippendall to discuss the matter in the next few days. During that discussion Dr Wenkart stated that he was agreeable to moving forward in trying to resolve the remuneration and costs issue.

Accordingly, our client had instructed us to restate the following offer to your clients subject to the Bankrupt’s written agreement:

1. the Trustee will accept the sum of $105,000 for his remuneration for work completed up to 31 December 2000;

2. the Trustee will accept the sum of $105,000 for costs and expenses incurred by him up to 31 December 2000;

3. from 1 January 2001 the Trustee’s remuneration to date is approximately $75,000 exclusive of GST and realisation charges. The Trustee will accept, in accordance with the Bankruptcy Regulations, 85% of his remuneration for work undertaken from 1 January 2001 to the date of any resolution passing a s.73 Proposal (exclusive of any GST or realisation charges);

4. the Trustee will accept 100% of those costs and expenses incurred by him from 1 January 2001 up to the date of the resolution passing a s.73 Proposal.

5. the costs and expenses referred to in point 4 above will, if your clients elect, be subject to a solicitor/client taxation unless agreement can otherwise be reached. The requesting creditor(s) is/are to fund the Trustee for such taxation prior to the Trustee commencing the taxation.

6. Dr Wenkart will provide the Trustee at the proposed Creditors’ Meeting immediately upon the passing of any s.73 Proposal, a mortgage in registrable form (prepared by the Trustee) over the property at 47 Union Street, Paddington as security for the amounts referred to in points 3 and 4 above. Any prior mortgagors or other holders of any interest in the property will grant the Trustee all necessary deeds in registrable form to the effect that the mortgage granted to the Trustee will have first priority over all interests in the property. The mortgage referred to will remain on the title to the property until payment of the amount determined to be payable under a certificate of taxation or of another amount agreed upon between the Trustee and Dr Wenkart.

7. In relation to the payments referred to in points 1 and 2, the Trustee must receive the said amount of $210,000 by bank cheque prior to the commencement of any meeting to consider a s.73 Proposal.

8. Dr Wenkart, the Intervenors and the Trustee agree to dismiss all current Court proceedings relating to the Bankrupt estate with no order as to costs.

9. Dr Wenkart, the Intervenors and the Trustee, subject to any agreement between those parties, agree to be bound by a taxation judgment and Dr Wenkart agrees to pay the amount owing under the Certificate(s) of Taxation failing which Dr Wenkart will permit the Trustee to sell the property at 47 Union Street, Paddington and apply the proceeds of sale in satisfaction of the remuneration, costs and expenses.

10. The Intervenors, Dr Wenkart and the Trustee each agree to enter into a deed comprising all of the above terms prior to the convening of a meeting to consider a s.73 Proposal.

We note your request for us to include in this letter details of our client’s proposed course should this agreement not be accepted. We do not wish to be provocative or difficult but we are obliged to inform you that should we be unable to reach agreement as to orders relating to the above, or execute a final written agreement between the Trustee, your clients and the Bankrupt, then the Trustee will be forced to lodge caveats and charges over all of the Bankrupt’s assets. Such caveats will secure his right to a full indemnity out of the assets of the estate and will remain in existence so long as any monies are outstanding to the Trustee. The Trustee will sell the properties to satisfy any outstanding amounts owed to the Trustee.

If it is necessary to proceed upon this course, Cutler Hughes & Hughes will not grant the Trustee a discount for legal costs and expenses and such costs and expenses will be subject to interest. From 1 January 2001 the Trustee has incurred legal costs and expenses of approximately $160,000.

So that there is no misunderstanding, our client is confident that any taxation would justify the costs and expenses incurred and we repeat the Trustee’s offer for your clients to review the work carried out on behalf of the Trustee (subject to the usual claims for privilege).

Accordingly, it seems to be in all parties’ interests that this matter be resolved as soon as practicable.

We confirm that this offer will remain open until 5.00pm Thursday, 31 January 2002.

45 The following observations may be made in respect of CHH’s letter dated 25 January 2002:

(a) As at 25 January 2002, no agreement had been reached among Dr Wenkart, his associated corporations and the trustee concerning the trustee’s claims for additional remuneration and reimbursement of expenses.

(b) Since at least 24 October 2001, Dr Wenkart had been prepared to provide security for the trustee’s remuneration and expenses provided that a settlement could be reached. This security was to take the form of a satisfactory charge or mortgage over the Paddington property.

(c) The proposal set out in CHH’s letter concerning the trustee’s remuneration was:

In respect of work done in the period up to 31 December 2000 for which the trustee had not yet been remunerated, the trustee would accept $105,000. This is completely consistent with the state of affairs known to both parties as at the end of 2000, namely, that, as at that date, a substantial sum of the order of $105,000 by way of trustee’s remuneration had been earned but remained unpaid.

In respect of work done in the period from 1 January 2001 to 25 January 2002, the trustee claimed to be entitled to $75,000 exclusive of GST and realisation charges. He said that he would accept 85% of that amount of $75,000 (exclusive of GST and realisation charges) and 85% of his remuneration from 25 January 2002 to the date of any resolution passing a s 73 proposal (exclusive of GST and realisation charges).

(d) The proposal set out in CHH’s letter concerning CHH’s fees and disbursements was:

In respect of work done in the period up to 31 December 2000 for which CHH had not yet been paid, the trustee would accept $105,000.

In respect of the trustee’s additional expenses (being CHH’s fees and disbursements), the trustee would accept 100% of those expenses incurred by him for work done in the period from 1 January 2001 to the date of any resolution passing Dr Wenkart’s s 73 proposal. In respect of expenses incurred after 1 January 2001 (and only in respect of such expenses), the trustee would, if required to do so by the Wenkart interests, require a taxation as between solicitor/client of CHH’s fees and disbursements unless agreement could otherwise be reached.

(e) The two amounts of $105,000 each were not intended to cover all amounts due to the trustee and CHH up to the date of any resolution passing Dr Wenkart’s s 73 proposal. Those amounts were expressed to relate to work done by the trustee and by CHH up to 31 December 2000 which had not been the subject of payment as at 25 January 2002. The offer by the trustee that he would require CHH to tax its fees and disbursements related only to fees and disbursements rendered for work done in the period after 1 January 2001 and not to paid costs which had been paid prior to 31 December 2000 and not to unpaid costs in respect of work done up to 31 December 2000 for which the amount of $105,000 was intended to constitute payment.

(f) The figures for the unpaid trustee’s remuneration ($105,000 plus $75,000) and for unpaid CHH’s fees and disbursements ($105,000 plus $155,000) as at 25 January 2002 were entirely consistent with the figures for unpaid trustee’s remuneration and unpaid CHH fees and disbursements provided by CHH in its letter to Hunt & Hunt dated 4 December 2001 – $183,875.11 for the trustee’s unpaid remuneration and $247,103.62 for CHH’s unpaid fees and disbursements.

46 Dr Wenkart and his corporate associates did not embrace the trustee’s offer made in CHH’s letter dated 25 January 2002. Instead Dr Wenkart applied to the Court for an order requiring the trustee to convene a meeting of creditors for the purpose of considering his annulment proposal. The taking of that step led to the commencement of the proceedings below.

A Brief History of the Proceedings Below (NSD 7051 of 2002)

The Early Period

47 By a document headed “Application” dated 15 February 2002 and signed by Dr Wenkart, which was transmitted by facsimile transmission by Dr Wenkart to Beaumont J on 15 February 2002, Dr Wenkart claimed the following:

Pursuant to Order 4 of Your Honour’s decision of the 8th February 2002, I request that you order the first respondent to call a meeting of creditors pursuant to s 73(2) of the Bankruptcy Act 1966.

Reasons

• My amended submission dated 30 January 2002 is attached and makes clear that unless the Court orders I will remain in bankruptcy indefinitely even though all eligible voting creditors and myself wish to have it determined urgently.

• Additionally, it is unjust and a denial of natural justice for this matter to continue to my detriment. Should any party to these proceedings wish to continue them, there is no reason to keep me captive to its conclusion.

48 Dr Wenkart’s additional submission dated 30 January 2002 referred to at the first dot point in his Application claimed an order requiring the trustee to call a meeting of his creditors in order to consider his s 73 proposal. In that submission, Dr Wenkart complained to the Court that the trustee had claimed that he was entitled to remuneration of $100,000 for work done by him in the twelve month period ending on 30 January 2002, excluding legal fees and disbursements. Dr Wenkart complained that the trustee had informed him that he (the trustee) would not convene a meeting of Dr Wenkart’s creditors until Dr Wenkart had agreed to accept the total amount claimed by the trustee for his remuneration and expenses.

49 Beaumont J treated the communication from Dr Wenkart which we have described at [47] above as the commencement of a fresh proceeding. The proceeding was allocated the plaint number NSD 7051 of 2002 although Dr Wenkart’s “Application” appears to have been originally filed in the proceeding commenced by Mr Pitman in August 2000 (NSD 7752 of 2000).

50 On 1 March 2002, Beaumont J made orders by consent requiring the trustee to convene a meeting of creditors within 14 days thereafter in order to consider Dr Wenkart’s s 73 proposal. One of the orders which Beaumont J made on 1 March 2002 was an order requiring Dr Wenkart to deliver to the trustee certain bank cheques (including a bank cheque for $105,000 drawn in favour of the trustee and a second bank cheque for $105,000 drawn in favour of CHH) without prejudice to the trustee’s rights to claim and to recover under the Bankruptcy Act all remuneration and expenses to which he was lawfully entitled under that Act in respect of the administration of Dr Wenkart’s bankrupt estate and also without prejudice to the rights of Dr Wenkart and Hapday to have the trustee’s remuneration and expenses determined in accordance with the Bankruptcy Act and Bankruptcy Regulations. The terms of these orders reflected the fact that, as at 1 March 2002, no agreement had been reached between Dr Wenkart and his associates, on the one hand, and the trustee, on the other hand, as to the amount which should be paid to the trustee in respect of his unpaid claim for remuneration and in respect of the amount of CHH’s fees and disbursements which were still unpaid as at that date.

51 On 11 March 2002, Beaumont J made the following consent orders in the proceedings below (the Consent Orders):

BY CONSENT THE COURT ORDERS AND NOTES THE AGREEMENT OF THE PARTIES AS FOLLOWS:

1. Warren Pantzer as Trustee of the Estate of Thomas Richard Wenkart may recover his remuneration, costs, charges and expenses to which he is lawfully entitled or may become lawfully entitled from Thomas Richard Wenkart and Thomas Richard Wenkart agrees to pay the same within 28 days of determination of the quantum of the same or at such other time as the parties may agree.

2. Thomas Richard Wenkart forthwith charges the land and improvements in folio identifier G/33817 and known as 47 Union Street, Paddington in favour of Warren Pantzer to secure the amount in paragraph 1.

3. Hapday Holdings Pty Ltd ACN 001 185 253 hereby postpones mortgage 3965299 over the land in paragraph 2 in favour of the interest of Warren Pantzer pursuant to the charge in paragraph 2.

4. The orders and agreements in paragraphs 1, 2 and 3 are only to have effect if the bankruptcy of Thomas Richard Wenkart is annulled pursuant to s 74 of the Bankruptcy Act on 15 March 2002.

5. Thomas Richard Wenkart consents to Warren Pantzer lodging a Caveat over the property in paragraph 2 for the purpose of securing the charge in paragraph 2 and Warren Pantzer will upon payment of the remuneration, costs, charges and expenses in paragraph 1 provide a Withdrawal of Caveat forthwith.

52 Those orders and notes were formally entered in the records of the Court on 19 March 2002.

53 At the time when the Consent Orders were made, the only parties to the proceedings below were Dr Wenkart, as applicant, and the trustee, as respondent. Nonetheless Hapday consented to the postponement of its mortgage as noted in paragraph 3 of the Consent Orders. Counsel who appeared before us at the hearing of the Appeal and the Cross-Appeals on behalf of Hapday accepted that Hapday had so consented.

54 As required by the orders of the Court, on 1 March 2002, the trustee convened a meeting of Dr Wenkart’s creditors for 15 March 2002. For the purposes of that meeting, the trustee made a report to the creditors dated 11 March 2002. By that report, the trustee updated creditors as to developments in the proceeding brought by Mr Pitman against the trustee and noted that the Court had directed that the trustee convene a meeting of creditors for a date which was to be no later than 15 March 2002 for the purpose of considering Dr Wenkart’s s 73 proposal. The trustee noted in his report dated 11 March 2002 that the Court had ordered Dr Wenkart to deliver to the trustee immediately before the s 73 meeting the following bank cheques:

(a) $105,000 drawn in favour of Warren Pantzer as trustee of the bankrupt estate of Thomas Richard Wenkart; and

(b) $105,000 drawn in favour of CHH.

55 After drawing the attention of the creditors to various inconsequential changes in relevant circumstances which had occurred between the date of Dr Wenkart’s most recent s 73 proposal (18 January 2001) and 1 March 2002, the trustee said (on p 2 of his report):

The following remuneration, costs and expenses remain outstanding and unpaid as at the date of this report (figures include GST):

| Warren Pantzer, Trustee (as at 4 March 2002) | $70,830.76 |

| Lawler Partners (as at 4 March 2002) | $136,506.27 |

| Cutler Hughes & Harris (approximate as at 27 February 2002) | $260,000.00 |

Outstanding remuneration and outstanding costs and expenses were the subject of consent orders made today, the effect of which is to secure payment of these outstanding amounts by first equitable mortgage over the Union Street Paddington property. Notwithstanding this, creditors will be asked at the meeting to approve my outstanding remuneration and outstanding costs and expenses. As creditors are aware my remuneration is calculated on a time basis in accordance with the rates formerly recommended by the Insolvency Practitioners Association of Australia. I attach a copy of the former IPAA scale for your information.

Updated figures will be provided at the meeting. It is anticipated that the above mentioned amounts will be reduced by the two bank cheques for $105,000.00 each referred to earlier herein.

I stated in my report accompanying the s 73 meeting convened for 31 January 2001 that I was of the view that there is a benefit to creditors in bringing certainty and finality to this administration. My view remains unaltered especially as the vast majority, if not all the creditors, support the bankrupt’s proposal.

I attach a notice of the meeting to be held on Friday, 15 March 2002 at 3.00 pm to consider the bankrupt’s proposal. I realise that this is short notice. However, the remaining creditors have indicated to me that they do not have any objection to short notice making the notice given reasonable in the circumstances.

56 Lawler Partners was the firm of accountants with which the trustee was professionally associated at all relevant times.

57 The total of the two amounts remaining due to the trustee and to Lawler Partners respectively set out in the trustee’s report dated 11 March 2002 was $207,337.03.

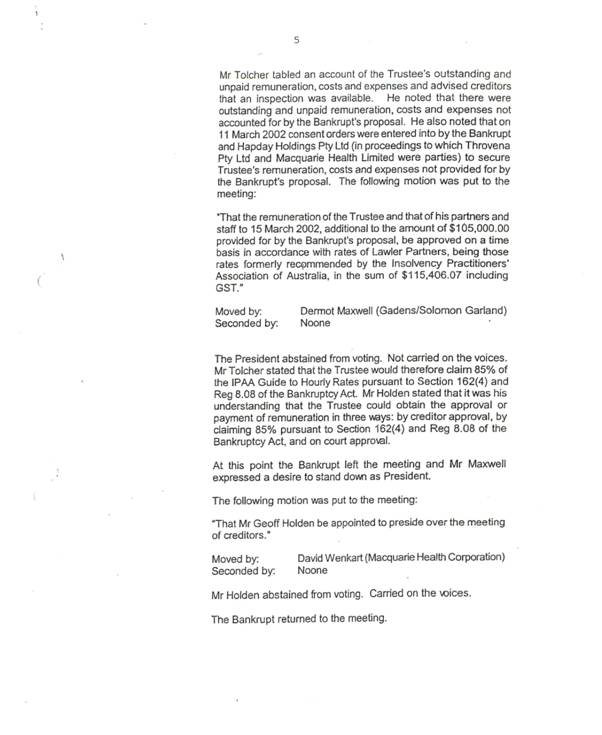

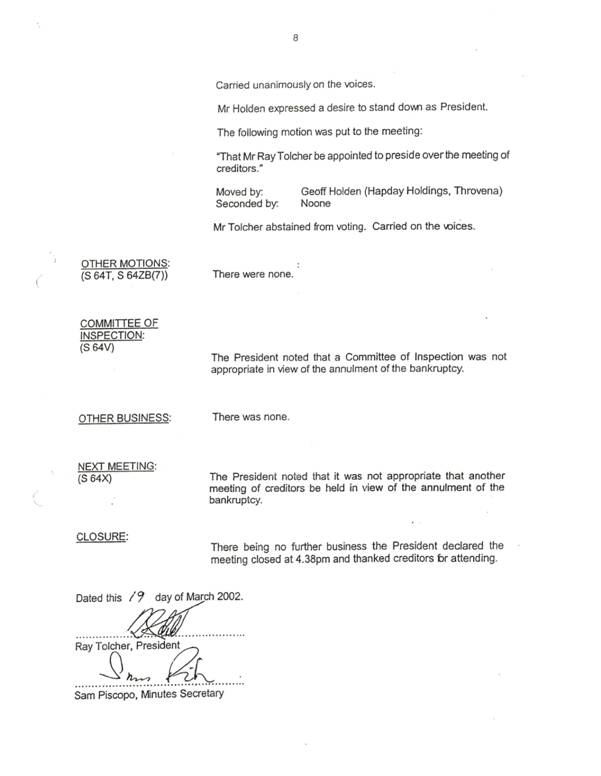

58 The creditors’ meeting convened for 15 March 2002 took place on that day. Attached to these Reasons for Judgment is a copy of the Minutes of that meeting. Those Minutes were dated and signed on 19 March 2002 by the trustee’s representative who attended the Meeting, Mr Ray Tolcher. Mr Tolcher presided over the meeting at one point but was not president at all times during that meeting. He was, however, present throughout the meeting.

59 According to the Minutes of the 15 March 2002 meeting, the creditors resolved to approve the payment to the trustee of $105,000 “… in accordance with paragraph (a)(i) of the bankrupt’s s 73 proposal as amended”.

60 An additional resolution in respect of the trustee’s remuneration recorded on p 5 of the Minutes of the meeting was put to the creditors but was not carried.

61 It is apparent from the Minutes of the meeting that, at the point in the meeting when the trustee’s remuneration was under discussion, Mr Maxwell, who was then acting as president, stood down as president and was replaced by Mr Holden. Mr Holden was in attendance at the meeting as a representative of Hapday and Throvena.

62 Thereafter, Mr Tolcher sought to have a modified resolution concerning the trustee’s remuneration passed by the creditors. That resolution was not carried.

63 At that point, Mr Tolcher stated that, in light of the failure of the creditors to approve the specific amounts claimed by the trustee for approval at the meeting, the trustee would claim 85% of the IPAA Guide to Hourly Rates pursuant to s 162(4) of the Bankruptcy Act and reg 8.08 of the Bankruptcy Regulations.

64 One of the representatives of CHH at the meeting (Mr Higginbotham) noted that the total amount for legal costs and disbursements owed by the trustee to CHH as at 1 March 2002 was approximately $337,301.72 (including GST) without prejudice to the right of CHH to claim further amounts for legal costs if properly claimable. This was a higher figure than the approximate figure previously indicated by the trustee as moneys due to CHH ($260,000).

65 Ultimately, as recorded in the Minutes, the bankrupt’s proposal for a composition dated 18 January 2001 as amended was accepted and approved by the creditors pursuant to s 73 of the Bankruptcy Act. The two bank cheques in favour of the trustee and CHH of $105,000 each referred to at [54] above were handed over to the trustee at the meeting. Those cheques were not cleared until some days later.

66 By letter dated 22 April 2002, relying upon the terms of the Consent Orders, the trustee demanded of Dr Wenkart that he pay to the trustee the sum of $98,095.16, being 85% of the remuneration claimed by the trustee as outstanding as at that point in time (viz $115,406.07). $115,406.07 was the balance of remuneration ultimately claimed by the trustee as outstanding as at 15 March 2002 ($220,406.07) less the amount of $105,000 paid to the trustee by Dr Wenkart on 15 March 2002. The trustee demanded payment within 28 days of receipt of the letter, failing which he said that he would proceed to enforce the charge which he held over the Paddington property. Omitting formal parts, this letter was in the following terms:

Re: Your Former Bankrupt Estate

I refer to previous communications.

I enclose a copy of the fee reconciliation entitled “Outstanding Remuneration as at 15 March 2002” (with annexures) tabled at your Section 73 meeting held on 15 March 2002 showing my outstanding remuneration. I also attach a copy of the consent orders made on 11 March 2002 by the Federal Court by which you agreed to pay my remuneration, costs, charges and expenses to which I am lawfully entitled or may become lawfully entitled within 28 days of determination of the quantum.

You have been sent a copy of the minutes of the Section 73 meeting. A motion was put at the Section 73 meeting to pay my outstanding remuneration in the amount of $115,406.07 (including GST) to 15 March 202, which was additional to the amount of $105,000.00 provided by your proposal. That motion was not passed and Mr Tolcher, as my representative, claimed 85% of that amount pursuant to Section 162(4) and Reg 8.08 of the Bankruptcy Act. You are therefore required to pay me $98,095.16 (including GST) within 28 days of receipt of this letter, failing which I will proceed to enforce the charge I have over the Paddington property and reserve any rights I may have to claim full remuneration of $115,406.07 to 15 March 2002 (these amounts do not include the outstanding and unpaid legal costs of Cutler Hughes Harris which will be taxed). I will also then reserve any rights I may have to remuneration beyond 15 March 2002.

Should you have any questions please contact Sam Piscopo of this office.

67 The fee reconciliation forwarded with the trustee’s letter dated 22 April 2002 was in the following terms:

Thomas Richard Wenkart

(Bankrupt)

Outstanding Remuneration as at 15 March 2002

| 4069 | 5147 | 5150 | TOTAL | ||

| Entered WIP | 122,379.25 | 69,073.50 | 2,645.40 | 194,098.15 | |

| Unentered March time for WP (130 units) | 4,901.00 | 4,901.00 | |||

| Unentered March time for SP (40 units) | 616.00 | 616.00 | |||

| Unentered March time for RT (20 units) | 754.00 | 754.00 | |||

| 128,650.25 | 69,073.50 | 2,645.40 | 200,369.15 | ||

| GST | 12,865.03 | 6,907.35 | 264.54 | 20,036.92 | |

| Total | 141,515.28 | 75,980.85 | 2,909.94 | 220,406,07 | |

| Less $105,000.00 as per bankrupt’s proposal | 105,000.00 | ||||

| Balance (including GST) | 115,406.07 |

68 By facsimile transmission dated 24 April 2002 sent to the trustee’s new solicitors, Sally Nash & Company, Hunt & Hunt requested the trustee to require CHH to tax their costs. In that facsimile, Hunt & Hunt said:

We refer to your client’s letter of 22 April 2002 to Dr Wenkart. In relation to your client’s claim for remuneration we have forwarded the claim to the taxing officer in accordance with regulation 8.09(1) of the Bankruptcy Regulations requesting the taxing officer to tax the claim.

Accordingly contrary to your client’s claim, in accordance with the Consent Orders the determination of the quantum of your client’s claim has not yet been determined and therefore the 28 days has not commenced.

Although your client has indicated he has asked Cutler Hughes & Harris to tax their costs, for abundant caution we request that those costs be taxed in accordance with section 167 of the Bankruptcy Act.

69 In May 2002, correspondence was exchanged between Dr Wenkart’s lawyers and the Official Receiver and between the trustee and the Official Receiver. Ultimately, ITSA informed Dr Wenkart that, from an inspection of the files, it appeared to ITSA that the remuneration claimed by the trustee had been properly approved and that the work done by him had not been carried out unnecessarily.

70 On 6 August 2002, the Official Receiver appointed Ms Ann Sexton to tax the Bill of Costs of CHH on the basis of a solicitor/client retainer for services provided to the trustee as trustee of Dr Wenkart’s bankrupt estate. The instrument of appointment did not make clear which costs and disbursements claimed by CHH were to be taxed. It simply referred to “… the bill of costs …” of CHH.

The Trustee’s Motion to Enforce the Charge over the Paddington Property and the Subsequent Applications

71 By late October 2002, the trustee had not received satisfaction in respect of his demand for payment of remuneration and expenses (including fees and disbursements payable to CHH) as the former trustee of Dr Wenkart’s bankrupt estate.

72 By Notice of Motion filed in the proceedings below on 31 October 2002, the trustee sought to enforce the charge which he held over the Paddington property. He claimed an order that he be appointed as trustee for sale of that property with power to deduct from the proceeds of sale thereof the amount of his outstanding remuneration, the amount of CHH’s unpaid fees and disbursements and all expenses of sale. The trustee did not seek a money judgment. He did seek his costs of the Motion on an indemnity basis.

73 On 18 November 2002, Dr Wenkart filed in the proceedings below a lengthy Notice of Intention to Oppose Application. In that document, Dr Wenkart set out the grounds and reasons upon which he intended to rely for resisting the orders sought by the trustee in the Notice of Motion filed by the trustee on 31 October 2002. In that document, Dr Wenkart contended that, because his bankruptcy had been annulled, the trustee no longer had any right to claim remuneration or expenses as the former trustee of his bankrupt estate. He also argued that the effect of the creditors’ resolutions concerning remuneration and expenses of the trustee which had been passed on 15 March 2002 was that the trustee would only be entitled to the total amount of $210,000 (the total of the two bank cheques of $105,000 payable to the trustee and to CHH) and that the said sum of $210,000 had been paid in full on 15 March 2002 thereby discharging the total liability undertaken by Dr Wenkart to pay to the trustee the remuneration and expenses to which he was lawfully entitled. In addition, Dr Wenkart contended that the trustee was not entitled to any remuneration or expenses incurred in respect of litigation in the period after he submitted his original s 73 proposal, ie in the period after 9 March 2000. The proposition was that most, if not all, work done by the trustee in the 2000, 2001 and 2002 calendar years should not be the subject of any remuneration or payment on account of expenses.

74 On 12 December 2002, Dr Wenkart filed a Notice of Motion in the proceedings below seeking declaratory relief in relation to the trustee’s entitlement to remuneration and expenses and an injunction restraining the sale of the Paddington property.

75 On 17 February 2003, Ms Sexton issued a Certificate of Taxation in respect of some of CHH’s fees and disbursements. That Certificate comprised Schedule A – Paid Costs and Schedule B – Unpaid Costs. Ms Sexton certified the amount of $88,042.24 in respect of paid costs covering some work during the period from 24 January 2000 to 19 March 2002. The Bills of Costs or Memoranda of Fees which were taxed by Ms Sexton on this occasion as “paid” costs were those bills which were paid when the bank cheque in favour of CHH for $105,000 was handed over on 15 March 2002. In other words, the only “paid” costs which were taxed by Ms Sexton were those which were paid by the tender of that bank cheque. These were fees and disbursements rendered in the period up to 31 December 2000 which were still unpaid as at the date of the annulment meeting. CHH fees and disbursements which had been paid earlier (i.e. in the period prior to the annulment meeting) were not taxed by Ms Sexton.

76 Ms Sexton certified $180,435.30 in respect of unpaid costs for work done in the period from 27 July 2000 to 15 March 2002. Thus, the total amount certified by Ms Sexton was $268,477.54. It is necessary to remember that, as at the annulment date, CHH had been paid fees and disbursements which totalled $380,225.51 (including the $105,000 paid on 15 March 2002) and claimed at that time a further amount of approximately $232,301.72. Therefore, as at 15 March 2002, the total fees and disbursements claimed by CHH both paid and unpaid was slightly more than $612,000. That amount included fees paid to various Counsel from time to time. In effect, Ms Sexton taxed the amount of approximately $232,301.72 (including GST) down to $180,435.30 (including GST).

77 On 9 April 2003, Beaumont J ruled that paragraphs 1–20 of Dr Wenkart’s Notice of Intention to Oppose Application filed on 18 November 2002 did not constitute an answer to the trustee’s application to enforce the charge granted to him pursuant to the Consent Orders.

78 In his Reasons for Judgment delivered on 9 April 2003 (Wenkart v Pantzer [2003] FCA 315), Beaumont J said (at [19]–[21]):

It must follow, in my opinion, that although the agreement evidenced in the consent orders was made during the bankruptcy, it had no dispositive effect until the annulment occurred by force of s 74(5) on 15 March 2002. In any event, even if the consent orders had some inchoate or quasi-dispositive effect, their operation was both validated and sanctioned by virtue of the provisions of s 74(6), whereby, as has been noted, (1) “all ... dispositions of property ... by ... the trustee ... or the Court before the annulment shall be deemed to have been validly made”; but (2) whilst the property of the bankrupt still vested in the trustee “vests in such person as the Court appoints or, in default of appointment, reverts to the bankrupt for all his ... estate or interest in it, on such terms and subject to such conditions (if any) as the Court orders”.

The effect of the consent orders (doubtless made with a view to achieving acceptance of the applicant’s s 73 proposal) was to defer the resolution of any dispute as to the amount of the respondent’s remuneration, but upon terms that the respondent would receive security for that amount. The Court sanctioned that arrangement in the form of an order made under the reservation reserved by the concluding words of s 74(6) – “reverts ... on such terms and subject to such conditions ... as the Court orders”.

Given that conclusion, it must follow, in my opinion, that the consent orders were within power and operate to vest in the respondent the charge created by par 2 thereof.

79 In a further judgment delivered on 14 April 2003 (Wenkart v Pantzer [2003] FCA 364), Beaumont J held that, having regard to the provisions of the Consent Orders and to the annulment of Dr Wenkart’s bankruptcy on 15 March 2002, the provisions of s 167 of the Bankruptcy Act continued to apply in accordance with their terms. At [5]–[7] of his Honour’s Reasons for Judgment delivered on 14 April 2003, his Honour said:

It will be recalled that par 1 of the consent order made on 11 March 2002 provided specifically that the respondent, as trustee of the applicant’s bankrupt estate, “may recover his remuneration, costs, charges and expenses to which he is lawfully entitled or may become lawfully entitled from Thomas Richard Wenkart and Thomas Richard Wenkart agrees to pay the same within 28 days of determination of the quantum of the same or at such other time as the parties may agree”. There was no other provision made in the consent order for the laying down of any procedural mechanism for the determination of the quantum. At the same time, as I indicated in my judgment on 9 April 2003, the inference should be drawn, as I mentioned in par 20 of that judgment, that the parties had agreed to defer the resolution of any dispute as to the amount of the respondent’s entitlement, but upon terms that the respondent would receive security for that amount.

In my opinion, the provisions of the consent order should be interpreted as “holding” or preserving the status quo regime. That is to say, in order to expedite the processing of the annulment procedure that was then contemplated, the applicant and the respondent, not at that stage being in agreement on the amount of the respondent’s entitlement, deferred the implementation of any process in that area, in the absence of any agreement by way of ultimate determination. It would, in my opinion, be quite perverse to attribute to either the applicant or the respondent, in the framing of the terms of the consent order, any objective of eliminating any of the machinery provisions that would have been available for the determination of the respondent’s entitlement. Such machinery was, of course, plainly available during the course of administration of the bankrupt estate.

Essentially, for the reasons I gave in the judgment published on 9 April 2003, and in particular, having regard to the provisions of s 74(6), I am of the view that, so far only as the matters mentioned in par 1 of the consent order made on 11 March 2002, the machinery provisions of the Act, in all their relevant application, remained in force so as to protect all parties concerned; that is to say, relevantly, both the applicant and the respondent. Those machinery provisions must, in my view, clearly include s 167 and for those reasons I answer the separate question.

80 The judgments delivered by Beaumont J in April 2003 did not finally determine the matters then before the Court.

81 As a result of those judgments, on 28 April 2003, Dr Wenkart amended his Notice of Intention to Oppose Application.

82 In Reasons for Judgment delivered on 1 May 2003 (Wenkart v Pantzer (2003) 1 ABC(NS) 236; [2003] FCA 432), Beaumont J determined that the trustee’s failure to put Dr Wenkart’s 9 March 2000 s 73 proposal to creditors did not constitute an answer to the trustee’s Cross-Claim.

83 On 5 May 2003, in Wenkart v Pantzer [2003] FCA 456, Beaumont J decided that, at the meeting of his creditors held on 15 March 2002, Dr Wenkart had not been notified in writing of the amount of the trustee’s claim for remuneration and expenses as required by reg 8.09(1) of the Bankruptcy Regulations (in the form in which it then stood) so as to trigger the 14 day period in which a taxing officer may tax a claim.

84 On 6 May 2003, Beaumont J delivered further Reasons for Judgment (Wenkart v Pantzer [2003] FCA 471) in which his Honour held that the trustee was entitled to be reimbursed by Dr Wenkart for the total amount certified by Ms Sexton in her Certificate of Taxation dated 17 February 2003 as well as an additional sum of $20,000 for which he (the trustee) was liable to the Commonwealth pursuant to the Bankruptcy (Estate Charges) Act 1997 (Cth).

85 On 29 August 2003, the Full Court overturned Beaumont J’s decision given on 5 May 2003 (Wenkart v Pantzer (2003) 132 FCR 204; [2003] FCAFC 210).

86 After referring briefly to the history of the disputes between Dr Wenkart and the trustee concerning the trustee’s remuneration, at 206 [5]–[8], the Full Court said:

One question which the judge determined was whether “[h]aving regard to the provisions of the consent order … and to the annulment of the [appellant’s] bankruptcy … do the provisions of s 167 of the Bankruptcy Act continue to apply in accordance with their terms?” The judge gave an affirmative answer to this question. The correctness of this answer is the subject of the first appeal.

Section 167(1) of the Bankruptcy Act 1966 (Cth) confers upon a trustee of a bankrupt’s estate the power to require the taxation of a bill of costs for services provided by any person in relation to the administration of the estate. The trustee may require the taxation on his own initiative, or at the request of the bankrupt or a creditor of the bankrupt’s estate.

The judge found that the consent orders did not have as their object the “eliminat[ion] of any of the machinery provisions that would have been available for the determination of the [trustee’s] entitlement [to costs]”. The judge said that “the machinery provisions of the [Bankruptcy] Act [in which he included s 167] in all their relevant application, remained in force so as to protect all parties concerned; that is to say, relevantly, both the [former bankrupt] and the [former trustee].” The judge did not err in this result, though we reach that result by a different route.

The appellant’s challenge to the judge’s decision is founded on two underlying assumptions. First, that neither the agreement nor the consent orders picked up s 167 (and if either purported to do so that is beyond the power of the parties). The second assumption is that following the annulment, s 167 had no independent application to a third parties’ bill. It is not necessary to consider the correctness of the first assumption, though for present purposes it may be accepted as correct. We are of the clear view, however, that the second assumption is misplaced. Division 2 of Pt VIII of the Bankruptcy Act (comprising ss 161B to 167) deals generally with the remuneration and costs which may be charged against a bankrupt’s estate. Thus, ss 161B and 162 allow the trustee to charge remuneration; ss 163 and 163A regulates the remuneration, costs and expenses of the official trustee; s 164 deals with the situation where two or more trustees act in succession; s 165 contains prohibitions against the receipt of outside benefits; and finally s 167 deals with the taxation of third party costs. Each of ss 162, 165 and 167 regulate the claims and entitlements of the trustee while he was acting in that capacity in relation to the appellant’s estate. The sections operate by force of the Bankruptcy Act and not because of any agreement between the parties or order of the court. Moreover, lest there be any doubt about the matter, we wish to make it clear that these provisions have effect notwithstanding the annulment of the bankruptcy. It could hardly be supposed that a trustee’s right to remuneration, the manner in which that remuneration is to be determined and the trustee’s right to require a third party’s bill of costs to be taxed is lost upon an annulment.

87 In the same set of Reasons, the Full Court rejected Dr Wenkart’s challenge to the decision of Beaumont J to the effect that the trustee was entitled to remuneration and expenses incurred after 9 March 2000.

88 In the last part of its Reasons, the Full Court dealt with the judgment delivered by Beaumont J on 5 May 2003 (Wenkart v Pantzer [2003] FCA 456). The Full Court disagreed with the conclusion reached by Beaumont J in that judgment. The Full Court held that, at the annulment meeting, both the bankrupt and his creditors had before them the precise amount of the trustee’s remuneration which was claimed but unpaid as at that date. When the resolutions put to the meeting did not pass, the trustee made clear that he would pursue a claim for 85% of the IPAA rate insofar as his remuneration was concerned. This had the consequence of causing time to run under reg 8.09(1) of the Bankruptcy Regulations. Under that regulation, Dr Wenkart was obliged to request any taxation pursuant to that regulation within 28 days of being notified in writing or becoming aware of the amount of the claim. Dr Wenkart was made aware of the amount of the claim on 15 March 2002 and should have lodged any request for taxation within 28 days thereafter, ie by 15 April 2002. He did not do so by that date. For that reason, Dr Wenkart lost his right to require the trustee to tax his claims for remuneration earned in the period up to and including 15 March 2002.

89 On 21 October 2003, Lindgren J, who by then had taken over the management of the proceedings below, made the following orders by consent:

THE COURT ORDERS THAT:

1. In respect of services provided by any person with respect to the estate in bankruptcy of the applicant, whether those services were provided before or after annulment of the applicant’s bankruptcy on 15 March 2002, the respondent by 22 October 2003 require such person to supply a Bill of Costs for such services pursuant to Section 167 of the Bankruptcy Act, 1966 (Cth) provided that this order does not extend to legal services provided by Cutler Hughes and Harris.

2. The respondent notify the applicant in writing by 23 October 2003 of his claim for remuneration in respect of services provided after the annulment of the applicant’s bankruptcy on 12 March 2002.

THE COURT NOTES THAT:

3. The applicant concedes that upon completion of taxation of the claims for costs and remuneration referred to in Orders 1 and 2, the amount taxed will be an amount within the following expression within Order 1 of the Orders made by Beaumont J on 9 April 2003 in this proceeding.

“remuneration, costs, charges and expenses to which [the respondent, Warren Pantzer, as trustee of the estate of the applicant, Thomas Richard Wenkart] is lawfully entitled or may become lawfully entitled from Thomas Richard Wenkart”.

4. The Commonwealth produces an invoice from Anne Sexton dated 14 October 2002 and inspection access to the invoice is granted to both parties.

5. The parties are agreed that Lindgren J should continue with the hearing of the respondent’s motion brought by notice of motion filed on 31 October 2002 and the applicant’s motion brought by notice of motion filed on 12 December 2002 as if Lindgren J stood in the shoes of Beaumont J in all respects including the respect that all evidence given before His Honour should be taken to have been given before Lindgren J and that Lindgren J should be part-heard on the motion.

90 The date in Order 2 made by Lindgren J on 21 October 2003, “12 March 2002”, is obviously incorrect. The date there referred to should have been “15 March 2002”. Further, the date in Order 3 made by Lindgren J on 21 October 2003, “9 April 2003”, should have been “11 March 2002”.

91 Order 1 made by Lindgren J on 21 October 2003 expressly excluded CHH’s fees and disbursements from its operation. Order 2 was intended to require the trustee to bring forward his claims for remuneration in the period commencing with the date of the annulment of Dr Wenkart’s bankruptcy and ending at 21 October 2003. The language of Order 3 reflected the parties’ expectation that the trustee would be required by Dr Wenkart to tax his claims for remuneration in respect of the period from 16 March 2002 to 21 October 2003 pursuant to the Bankruptcy Act and the Bankruptcy Regulations.

92 On 29 October 2003, Lindgren J declined to grant to Dr Wenkart an extension of time within which he might seek to require the trustee to tax his remuneration earned in the period from 30 January 2001 to 15 March 2002 (Wenkart v Pantzer (No 6) [2003] FCA 1210).

93 On 30 October 2003, Lindgren J held that the realisations charge set out in s 6(1)(a) of the Bankruptcy (Estate Charges) Act 1997 (Cth) did not apply to any amounts received by the trustee after the annulment of Dr Wenkart’s bankruptcy on 15 March 2002 (Wenkart v Pantzer (No 7) (2003) 132 FCR 273; (2003) 1 ABC(NS) 483; [2003] FCA 1211).

94 In a judgment delivered on 22 March 2004 (Wenkart v Pantzer (No 3, formerly No 8) (2004) 135 FCR 422, (2004) 1 ABC(NS) 490; [2004] FCA 280) Lindgren J held that this Court had jurisdiction to hear and determine the application brought by the trustee to enforce the charge granted to him by Dr Wenkart on 11 March 2002 by means of the Notice of Motion filed by the trustee in the proceedings below on 31 October 2002.

95 Subsequently, on 31 March 2004, Lindgren J made the following orders “regularising” the proceedings below and programming the hearing of the substantive issues remaining for disposition by the Court:

THE COURT ORDERS THAT

1. The applicant’s letter dated 15 February 2002 to Beaumont J (and attachments) requesting him to order the first respondent to convene a meeting of creditors be taken to be the application by which this proceeding was commenced, and be now placed on the Court file accordingly, but be taken to have been filed on 21 February 2002, and that to the extent necessary, compliance with the Rules be, and be taken to have been, dispensed with.

2. Any filing fee that would otherwise be payable on the application be, and be taken to have been, waived.

3. The first respondent’s motion brought by notice of motion filed on 31 October 2002 be taken to be, and to have been, a cross-claim seeking final relief, and that to the extent necessary, compliance with the Rules be, and be taken to have been, dispensed with.

4. Any filing fee that would otherwise be payable on the cross-claim be, and be taken to have been, waived.

5. The first respondent as cross-claimant file and serve by 23 April 2004 points of claim outlining his claim for final relief including quantification.

6. The applicant as cross-respondent file and serve by 14 May 2004 points in reply.

7. The proceeding be stood over to Wednesday 19 May 2004 at 9.30 am for directions.

96 On 23 April 2004, the trustee filed Points of Claim (the trustee’s Cross-Claim) as directed by Lindgren J on 31 March 2004. The money claim which he made at that time was quantified in par 45 of his Points of Claim in the following terms:

45. Pantzer claims as against Wenkart pursuant to the terms of paragraph 1 of the orders made on 12 March 2000 to the following monies:

| 1. | Cutler Hughes and Harris (including GST) plus interest accruing from 07.05.03 inclusive at a daily rate of $36.99 | $168,137.79 |

| 2. | Costs of Taxation of Anne Sexton in relation to Cutler Hughes and Harris Bill of Costs | $15,061.75 |

| 3. | Estate Realisation Charge (plus statutory interest accruing from 01.07.03) | $20,000.00 |

| 4. | Trustee’s remuneration and disbursements (pre bankruptcy) plus interest to be estimated | $98,095.16 |

| 5. | Trustee’s post bankruptcy remuneration and disbursements (post bankruptcy) subject to taxation estimated from 15.03.03 to 02.04.04 | $140,707.09 |

| 6. | Trustee’s solicitor’s costs and disbursements of these proceedings (subject to assessment or taxation) | $122,718.30 |

| 7. | Trustee’s solicitor’s costs and disbursements relevant to Full Court Appeal in proceedings: 633 of 2003 | $31,290.00 |

| 8. | Trustee’s solicitor’s costs and disbursements of High Court Special Leave (subject to order and taxation) estimated | $20,000.00 |