FEDERAL COURT OF AUSTRALIA

Sagacious Legal Pty Ltd v Wesfarmers General Insurance Ltd

[2011] FCAFC 53

IN THE FEDERAL COURT OF AUSTRALIA | |

| Appellant | |

AND: | WESFARMERS GENERAL INSURANCE LIMITED Respondent |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. The appeal be dismissed with costs.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules. The text of entered orders can be located using Federal Law Search on the Court’s website.

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 651 of 2010 |

ON APPEAL FROM THE FEDERAL COURT OF AUSTRALIA |

BETWEEN: | SAGACIOUS LEGAL PTY LIMITED Appellant

|

AND: | WESFARMERS GENERAL INSURANCE LIMITED Respondent

|

JUDGES: | BESANKO, PERRAM & KATZMANN JJ |

DATE: | 13 APRIL 2011 |

PLACE: | SYDNEY |

REASONS FOR JUDGMENT

Introduction

1 The appellant is a company controlled by Paul O’Shanassy, a solicitor, who is its sole director. The appellant owned a Mercedes Benz motor vehicle (“the car”) which it insured with the respondent through an underwriter. Mr O’Shanassy’s wife, Lana, was, with him, a nominated driver.

2 On 16 January 2008 Mrs O’Shanassy was involved in a serious accident when she was driving the car. The police attended the scene of the accident and Mrs O’Shanassy was taken by ambulance to hospital. At the hospital a blood sample was taken from her and alcohol was detected in it. She was then charged with the offence of driving whilst there was present in her blood a mid-range concentration of alcohol (that, is more than 0.08 but less than 0.15). A magistrate dismissed the prosecution on 19 March 2009 with costs. The trial judge, however, found that she had been drinking a substantial amount of alcohol in the two hours before the accident and that she was affected by it at the time. He also found that her blood alcohol level when it was tested within two hours of the accident was 0.124, more than twice the legal limit.

3 Within a week of the accident the appellant made a claim under the insurance policy.

4 On 5 December 2008 the respondent wrote to the appellant denying indemnity. It pointed to the exclusions in the policy, noting that the contract of insurance would not cover circumstances in which the driver was under the influence of drugs or alcohol, had a blood alcohol level over the legal limit within two hours of the event, or was convicted of an offence of driving under the influence of alcohol or drugs at the time of the accident. It noted that the claim form stated that Mrs O’Shanassy was driving the car and, to the knowledge of the appellant, had not consumed any alcohol or taken any drugs within the 12 hours before the collision. Amongst other things it noted that the police report indicated that Mrs O’Shanassy had a blood alcohol level well in excess of the legal limit and referred to the appellant’s failure to cooperate with the insurer, contrary to the terms of the policy and the Insurance Contracts Act 1984 (Cth)(“the Act”).

5 On 1 June 2009 (after the criminal proceedings had concluded) the appellant filed an application for damages for breach of the contract of insurance. In substance, the defence filed on 9 July 2009 pleaded the material facts that supported the respondent’s decision to refuse indemnity under the policy.

6 On 12 August 2009 the appellant filed a reply. In summary it pleaded that the appellant had made all the necessary disclosures and, to the extent that it had not, that the respondent had waived its right to rely on it, invoking s 21(3) of the Act. It denied a number of the allegations made in the defence but it did not deny that at the time the vehicle was damaged, Mrs O’Shanassy was under the influence of intoxicating liquor.

7 On 23 October 2009 the matter was fixed for hearing commencing 8 March 2010.

8 On the first day of the hearing, during the course of its opening, the appellant sought leave to amend its reply in two respects, first, to deny that Mrs O’Shanassy was under the influence of alcohol at the time of the accident and secondly, to plead that the appellant had not consented to her driving the vehicle at that time. The respondent did not oppose the first, but did oppose the second amendment and the trial judge refused it: Sagacious Legal Pty Ltd v Wesfarmers General Insurance Ltd (No. 2) [2010] FCA 275 (Sagacious Legal (No 2)). A month after the trial judge had reserved his judgment, the appellant made an application to set aside the order refusing to allow the amended reply to be filed. That application was also refused: Sagacious Legal Pty Ltd v Wesfarmers General Insurance Ltd (No. 3) [2010] FCA 428.

9 The trial judge found in favour of the respondent and awarded it costs: Sagacious Legal Pty Ltd v Wesfarmers General Insurance Ltd (No. 4) [2010] FCA 482 (the “principal judgment”). In a separate judgment his Honour varied his previous costs order to order that the costs from 13 August 2009 be paid on an indemnity basis: Sagacious Legal Pty Ltd v Wesfarmers General Insurance Ltd (No. 5) [2010] FCA 630 (Sagacious Legal (No 5)). In the principal judgment he rejected Mrs O’Shanassy’s evidence on all disputed questions and he also made adverse findings about Mr O’Shanassy’s credit, although Mr O’Shanassy was not called to give evidence and counsel had agreed that no Jones v Dunkel (1959) 101 CLR 298 (Jones v Dunkel) submission would be made.

10 The appellant now appeals against each of these judgments.

Issues

11 The trial judge found that there had been a non-disclosure and a misrepresentation in connection with the policy of insurance and that the respondent was entitled to reduce its liability to nil under s 28(3) of the Act. The appellant challenges that conclusion and this challenge is the first issue in the case.

12 As part of his consideration of the non-disclosure and misrepresentation defences the trial judge considered Mr O’Shanassy’s role in the relevant events. Mr O’Shanassy did not give evidence at the trial. The trial judge made a number of findings adverse to Mr O’Shanassy and the appellant submits that he erred in doing so in light of an agreement between counsel about the significance of Mr O’Shanassy not giving evidence. The trial judge’s findings with respect to Mr O’Shanassy’s role in the relevant events is the second issue in the case.

13 The trial judge found that the circumstances of the accident fell within two general exceptions in the policy of insurance. First, he found that the circumstances of the accident fell within the exception in relation to loss or damage caused while the insured car “is being driven by … any person under the influence of intoxicating liquor”. Secondly, he found that the exception in relation to loss or damage caused while the insured car “is being driven by or is in the charge of anyone in whose blood the percentage of alcohol is in excess of the legal limit as prescribed by the law in [New South Wales], as indicated by analysis of the person’s breath or blood taken within 2 hours of the occurrence of the event giving rise to such loss, damage or liability” was engaged. The appellant does not challenge either of those conclusions. However, it contends that there was a proviso to the policy of insurance which was to the effect that a claim would be paid if, in the circumstances of this case, the appellant proved that it did not consent to the motor vehicle being driven by or being in the charge of Mrs O’Shanassy when she was affected by alcohol or a drug and that the respondent agreed that the appellant had no reason to suspect that Mrs O’Shanassy was under the influence of alcohol or any drug.

14 If this proviso applied then the two exceptions would not be an answer to the appellant’s claim. On the first day of trial the appellant sought leave to amend its Reply to plead the proviso. The trial judge refused leave to amend. The appellant challenges that decision and this is the third issue in the appeal.

15 Finally, the trial judge ordered that the appellant pay the respondent’s costs on an indemnity basis from 13 August 2009. He found that the appellant had acted unreasonably both in its conduct of the proceeding and in rejecting an offer made by the respondent. The appellant challenges that conclusion and this is the fourth issue in the appeal.

First Issue: mISREPRESENTATION and NON-DISCLOSURE

16 The insurance policy had been issued in September 2004 and was preceded by a proposal form completed by Mr O’Shanassy on behalf of the appellant on 30 September 2004 (the “2004 proposal form”). The policy had been renewed annually and was current as at the time of the accident.

17 At the time the 2004 proposal form was submitted to the respondent Mrs O’Shanassy had two convictions for driving with in excess of the prescribed concentration of alcohol in her blood: the first in 1999 when she was disqualified from holding a driver’s licence for 18 months and the second in 2002 when she was disqualified from holding a driver’s licence for 12 months. In the case of the 1999 offence the disqualification extended over the period from July 1999 to January 2001 and in the case of the 2002 offence the disqualification extended over the period from April 2002 to April 2003.

18 Prestige Car Insurance Pty Limited was an underwriting agency. It had a binder with Lumley General Insurance Ltd (“Lumley”) (now the respondent) under which it was authorised to enter into contracts, on Lumley’s behalf, to insure prestige vehicles with values between $40,000 to $500,000 and certain other special categories of vehicles. Each year Prestige and Lumley agreed on the terms upon which the former could write insurance. Those terms were set out in an operations manual.

19 The chief executive of Prestige was Mr Raymond Woodlands and the chief underwriter was Ms Debbie Jacks. Under the binder only Mr Woodlands and Ms Jacks had authority within Prestige to accept any driver as a risk where that driver had one conviction for driving under the influence of intoxicating liquor, or well in excess of the prescribed concentration of alcohol (described compendiously in the operations manual as a ‘DUI offence’) or if his or her licence had been suspended or cancelled. Prestige’s operations manual also provided that it had to decline any driver as a risk where the driver had more than one conviction for a DUI offence or had had his or her licence suspended or cancelled more than once.

20 Before September 2004 Mr O’Shanassy had, through the agency of Prestige, insured other vehicles with Lumley. In April or May 2002 he personally insured another Mercedes Benz vehicle with the respondent. When the policy was taken out he was the only person named as a nominated driver. In April 2003 Mrs O’Shanassy was added to the policy as a nominated driver after she and her husband had completed a document called a Driver’s Declaration on 28 April 2003 (the “Driver’s Declaration”).

21 In about May 2003 a company called Fukura Pty Limited (“Fukura”) insured a Range Rover vehicle with the respondent. The nominated drivers under the policy were both Mr O’Shanassy and Mrs O’Shanassy. Fukura was described in the documents as a management company. Mr O’Shanassy was the managing director of the company and he completed the proposal form for the insurance on 27 May 2003 (the “Fukura proposal”).

22 The respondent’s pleaded case before the trial judge was put in terms of both misrepresentation and non-disclosure. The misrepresentation case was that the appellant’s proposal falsely represented that the only driving conviction Mrs O’Shanassy had in the five years to September 2004 was for not wearing a seat belt and she had not, during that five-year period, been charged or convicted in connection with any intoxicating liquor or drug. The respondent also pleaded that the appellant had failed to disclose Mrs O’Shanassy’s driving record in the 2004 proposal form in circumstances where it knew, or a reasonable person in its position would be expected to know, that her 1999 conviction and licence cancellation would be a matter relevant to the decision of the insurer to issue the policy.

23 In order to understand the issues before the trial judge and those raised on the appeal it is convenient to identify the relevant questions and answers in the 2004 proposal form.

24 The note appearing next to the asterisk refers to the disclosures under separate cover in the names of Mr O’Shanassy and Fukura. The disclosures made in relation to the issuing of those policies included the disclosure of Mrs O’Shanassy’s 2002 conviction but there was no disclosure of her 1999 conviction. The respondent’s case was that the appellant’s answer to question b(v) in the 2004 proposal form was a misrepresentation because, at best for the appellant, there was a disclosure of the 2002 conviction but no disclosure of the 1999 conviction. In the alternative, or additionally, the respondent’s case was that there was a failure by the appellant to comply with its duty of disclosure under s 21 of the Act.

25 In essence the trial judge accepted these arguments. He did not distinguish between misrepresentation and non-disclosure. At one point he referred to misrepresentation by omission, but there was no criticism of his approach in not distinguishing between the two. Plainly, there will be cases where there will be room for both to operate.

26 The trial judge found that, had Prestige known of Mrs O’Shanassy’s 1999 conviction and driver’s licence cancellation, she would have been rejected as a nominated driver. The appellant does not challenge that conclusion.

27 It may be that the trial judge had an alternative basis for his decision. He took the view there was a misrepresentation and non-disclosure in relation to both the Driver’s Declaration and the Fukura proposal and reasoned from this premise that, had that not occurred, Prestige would have known of the 1999 conviction and disqualification and would not have accepted Mrs O’Shanassy as a nominated driver under the policy over the vehicle. The respondent did not put a submission seeking to uphold the precise steps involved in this alternative reasoning and this Court does not need to consider it because we have reached the conclusion that the trial judge was correct in holding that there was a misrepresentation and non-disclosure in relation to the appellant’s proposal.

28 Both parties submit that the Driver’s Declaration and the Fukura proposal are significant but for different reasons. The appellant contends that the reference to them in the appellant’s proposal means that the period for which disclosure was required was limited with the consequence that the 1999 offence and disqualification did not need to be disclosed. The respondent contends that the appellant’s proposal made two representations. First, it made a representation that the only convictions in connection with intoxicating liquor or drugs are those disclosed in the documents incorporated by reference (the “incorporated documents”), and secondly, it makes a representation that the incorporated documents are themselves accurate.

29 On each party’s case then it is necessary to consider the Driver’s Declaration and the Fukura proposal and the trial judge’s findings with respect to those documents.

The Driver’s Declaration

30 When Mrs O’Shanassy’s period of driver’s licence disqualification following the 2002 conviction ended in April 2003 it was proposed that she be included as a nominated driver under the policy in the name of Mr O’Shanassy. A Driver’s Declaration had to be completed and accepted by Prestige. Mr O’Shanassy was responsible for completing most of the Driver’s Declaration.

31 One of the questions in the Declaration, Question B, was to the effect of asking whether the nominated driver (that is, Mrs O’Shanassy) had had ‘insurance or driving licence declined, cancelled, or special terms imposed?’ The ‘yes’ box was ticked and in the section where the person completing the form was asked to provide details, the following appeared:

Mid Range PCA Charge

2 April 02

Nothing was said about the 1999 conviction and disqualification.

Next to the typed section asking for details with respect to the answer to Question B the following appears in handwriting:

3 yrs

The Driver’s Declaration also sought information about claims or accidents and it sought details of convictions in the three years prior to the completion of the Declaration. In the latter context Mr and Mrs O’Shanassy provided details of the 2002 offence. As we have said, the Driver’s Declaration was signed by both Mr and Mrs O’Shanassy and was dated 28 April 2003.

32 On the morning of 29 April 2003 there was a telephone conversation between Mrs O’Shanassy and Ms Jacks. The trial judge found that Mrs O’Shanassy’s telephone was on speaker phone and that Mr O’Shanassy was present during the conversation. We will return to the telephone conversation shortly.

33 After the conversation Mrs O’Shanassy sent Ms Jacks the completed Driver’s Declaration facsimile transmission with a letter dated 29 April 2003 which read as follows:

Drivers Declaration Policy No. 6PUM/3725081

Please find attached completed Drivers Declaration form. As per your instruction during our phone conversation this morning, I have listed any offences/claims within the last 3 years for each of the questions on the form.

Can you please advise immediately if you require further information. I would appreciate if you could confirm my status as a nominated driver effective today as my husband is ultra conservative.

34 Mrs O’Shanassy and Ms Jacks gave evidence about, inter alia, the telephone conversation and were cross-examined. Mr O’Shanassy did not give evidence.

35 Mrs O’Shanassy’s evidence was directed towards proving that it was understood between the O’Shanassys on the one hand, and Prestige on the other, that the disclosure about driver’s licence disqualification was limited to a period of three years.

36 The trial judge said that he did not find Mrs O’Shanassy to be a satisfactory or reliable witness. He found that both Mr and Mrs O’Shanassy had discussed the 1999 offence and the possible need to disclose it at this time. He found Ms Jacks to be an impressive and honest witness and noted that only she and Mr Woodlands were authorised to accept a risk where there was one licence cancellation. He also noted Prestige was not authorised under its binder with the respondent to accept a risk where there had been more than one licence cancellation.

37 The trial judge found that the telephone conversation on 29 April 2003 related to offences or claims or both and not to licence cancellations. The trial judge rejected Mrs O’Shanassy’s evidence to the contrary. He also rejected a submission that the handwritten note on the Driver’s Declaration and a failure by Prestige to inquire amounted to a waiver.

38 The trial judge found that the intention of Mr and Mrs O’Shanassy was to avoid disclosing the 1999 conviction and licence cancellation and that they tried to orchestrate a situation where they would not have to do so. He found that their conduct towards Prestige and Ms Jacks was disingenuous and lacking in integrity.

39 The trial judge rejected any suggestion that there could be reliance on s 26(1) or s 26(2) of the Act. He said (at [36]):

I am not satisfied that Mr or Mrs O’Shanassy held a belief that the answer given to question B was all that the insurer required. I accept the insurer’s submission that the careful wording of the conversation, letter and the driver’s declaration were all designed to enable Sagacious, and Mr and Mrs O’Shanassy, to avoid disclosing the 1999 conviction and associated cancellation, so as to not alert Mrs Jacks and the insurer to those matters. A reasonable person in the circumstances would not have held that belief for the purposes of s 26(1) of the Insurance Contracts Act. The answer given to question B was untrue because of that omission. And I am satisfied that Sagacious, Mr and Mrs O’Shanassy, or a reasonable person in their position could be expected to have known that this omitted information would have been relevant to the decision of the insurer to accept the risk of her being a nominated driver for the purposes of s 26(2).

40 He found that in answering Question B, the appellant misrepresented, by omission, the 1999 cancellation of Mrs O’Shanassy’s driver’s licence and the insurer accepted Mrs O’Shanassy as a nominated driver as a result of that untrue representation.

41 The trial judge rejected a waiver defence under s 21(3) of the Act stating that the answer to Question B was not obviously incomplete or irrelevant in the context of the letter and the telephone conversation.

42 On the appeal, there were no challenges to these findings as far as Mrs O’Shanassy was concerned. There was a challenge to the findings as far as Mr O’Shanassy is concerned.

The Fukura proposal

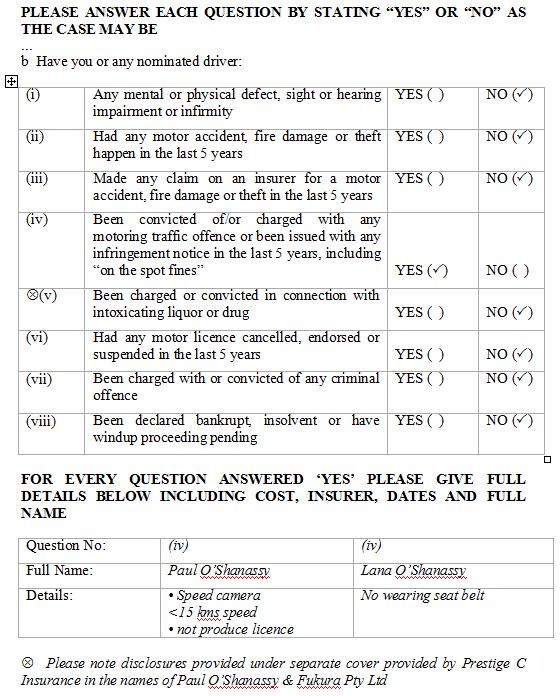

43 Mr O’Shanassy completed the Fukura proposal on 27 May 2003. The proposal form contained the following:

b – Have you or any nominated driver:

… | |

(ii) Had any motor accident, fire damage or theft happen in the last 5 years | Yes( X ) No ( ) |

… (iv) Been convicted of/or charged with any motoring traffic offence or been issued with any infringement notice in the last 5 years, including with intoxicating liquor or drug | Yes( X ) No ( ) |

(v) Been charged or convicted in connection with intoxicating liquor or drug | Yes( X ) No ( ) |

(vi) Had any motor licence cancelled, endorsed or suspended in the last 5 years | Yes( X ) No ( ) |

(vii) Having regard to “YOUR DUTY OF DISCLOSURE” at the beginning of this proposal is there any other matter or information which may be relevant to our acceptance of this proposal such as previous loss or damage, previous claims, damage or injury to third parties on their property whether insured or not; criminal convictions or charges pending or bankruptcy or winding up proceedings for any party to this insurance | Yes( ) No ( X ) |

FOR EVERY QUESTION ANSWERED “YES” PLEASE GIVE FULL DETAILS BELOW INCLUDING COST, INSURER, DATES AND FULL NAME

…

Question No: b(ii)

Full Name: Lana R O’Shanassy

Details: (a) Claim on (your reference 8019) insurance Policy 6 DOM/3725081

(b) PCA mid range charge 2 April 02 and see Drivers Declaration on above policy dated 28/4/03

We have emphasised the same parts of these questions as the trial judge did.

44 The trial judge found that the answers to questions (b)(iv), (v), (vi) and (vii) of the Fukura proposal omitted any reference to Mrs O’Shanassy’s 1999 conviction and disqualification and that the statements were made in connection with a proposed contract of insurance. The statements were untrue and amounted to a misrepresentation.

45 The trial judge rejected any suggestion that the appellant or Fukura could rely on s 26(1) or s 27 of the Act.

The 2004 proposal form

46 With this background we return to the appellant’s proposal.

47 The trial judge found that the 1999 conviction and disqualification occurred more than five years before the appellant’s proposal was completed on 30 September 2004 and therefore the answers to questions b(iv) and (vi) were correct. He said that the negative answer to question b(v) had to be understood in the context of the earlier disclosures.

48 The trial judge said that he was satisfied that at all times before 16 January 2008 the appellant was aware that the respondent was not aware of the 1999 conviction and disqualification.

49 The trial judge found that the answers to questions b(iv), (v) and (vi) in the Fukura proposal were false to the knowledge of Mr O’Shanassy and through him to the knowledge of Fukura and the appellant. He found that Mr O’Shanassy was aware of the significance of the questions to the risk the insurer was being asked to accept. A reasonable person in his position would have been expected to know that the 1999 conviction and disqualification was a significant matter that was obviously relevant to the insurer.

50 The trial judge found that reasonably construed question b(v) in the Fukura proposal and in the 2004 proposal form sought a disclosure unlimited as to any time period and he found that the responses in the Driver’s Declaration, Fukura proposal and the 2004 proposal form were clear and unambiguous on their face and did not reveal the truth.

51 On 7 December 2004 Prestige wrote to the appellant in the following terms:

Thank you for your payment of your motor vehicle insurance, however to enable us to process this proposal would you please provide the information requested below.

PLEASE CLARIFY NUMBER OF TRAFFIC OFFENCES INCURRED BY

EACH DRIVER IN PAST THREE YEARS. THANK YOU.

52 The trial judge construed this as relating to question b(iv) and having the effect of “limiting [the question] to a period of three years”. However, he rejected a submission that the respondent had waived the appellant’s duty of disclosure by its request dated 7 December 2004. Furthermore, he was not satisfied that the appellant held any belief it had made an accurate representation in respect of the 1999 conviction and disqualification in the answers to questions b(v) and (vi). He said (at [58]):

Mr O’Shanassy knew, and a reasonable person in the circumstances would have known, that these matters were relevant to the insurer’s decision whether or not to accept the risk of his wife being a nominated driver.

The arguments on appeal and their disposition

53 Before addressing the arguments addressed on the appeal it is convenient to set out the relevant provisions of the Act for the purposes of this appeal. They are as follows:

21 The insured’s duty of disclosure

(1) Subject to this Act, an insured has a duty to disclose to the insurer, before the relevant contract of insurance is entered into, every matter that is known to the insured, being a matter that:

(a) the insured knows to be a matter relevant to the decision of the insurer whether to accept the risk and, if so, on what terms; or

(b) a reasonable person in the circumstances could be expected to know to be a mater so relevant.

(2) The duty of disclosure does not require the disclosure of a matter:

…

(d) as to which compliance with the duty of disclosure is waived by the insurer.

(3) Where a person:

(a) failed to answer; or

(b) gave an obviously incomplete or irrelevant answer to;

a question included in a proposal form about a matter, the insurer shall be deemed to have waived compliance with the duty of disclosure in relation to the matter.

26 Certain statements not misrepresentations

(1) Where a statement that was made by a person in connection with a proposed contract of insurance was in fact untrue but was made on the basis of a belief that the person held, being a belief that a reasonable person in the circumstances would have held, the statement shall not be taken to be a misrepresentation.

(2) A statement that was made by a person in connection with a proposed contract of insurance shall not be taken to be a misrepresentation unless the person who made the statement knew, or a reasonable person in the circumstances could be expected to have known, that the statement would have been relevant to the decision of the insurer whether to accept the risk and, if so, on what terms.

…

27 Failure to answer questions

A person shall not be taken to have made a misrepresentation by reason only that the person failed to answer a question included in a proposal form or gave an obviously incomplete or irrelevant answer to such a question.

54 The appellant put four arguments on the appeal.

55 First, it submitted that it was only required to disclose offences that had occurred within five years of 30 September 2004 and as the 1999 conviction and disqualification had occurred outside the five-year period, there was no obligation to disclose it. This argument relies on the context in which question b(v) appears. It does not only rely on the incorporated documents and in fact the argument is inconsistent with, and therefore must be in the alternative to, the second argument.

56 The argument is that question b(v) should be construed as limited to a period of five years and therefore as extending back only to 30 September 1999. The appellant points to the fact that the questions in ‘a’ which are unlimited as to time use the word ‘ever’ and yet that word does not appear in question b(v). It also points to the fact a number of questions in ‘b’ have a time limit of five years and in that respect it points to (ii), (iii), (iv) and (vi) (see [8] above). Whilst question b(i) is not a question where one would expect to find a time limit, we note there is no time limit in questions b(vii) and (viii). Finally, the appellant points to the fact that there may be considerable overlap between the various questions. The last point is no doubt true and can be illustrated by reference to this case in that but for the five year time limit in questions b(iv) and (vi) the 1999 conviction and disqualification would also fall within the scope of those paragraphs.

57 All of these points may, to the extent we have indicated, be accepted. However, they do not persuade us that question b(v) should be limited to five years. It is not clear by what process of reasoning the clause would be so limited. The fact that the questions may overlap is not sufficient and it cannot be said that it is obvious that the insurer would not be interested in, or concerned with, convictions in connection with intoxicating liquor or drugs outside a five-year period. We reject the first argument. We would only add that there is a good deal of force in the respondent’s submission that even if question b(v) was restricted to five years, there was a representation that the Fukura proposal was accurate and that was a misrepresentation because the Fukura proposal did not disclose the 1999 conviction and disqualification which was within five years of the Fukura proposal (that is, 27 May 2003).

58 Secondly, it was submitted by the appellant that the reference in the 2004 proposal form to prior disclosures had the effect of limiting the period for disclosure to three years being either three years calculated by reference to 30 September 2004 (that is 30 September 2001) or three years calculated by reference to the date of the Driver’s Declaration dated 28 April 2003 (that is, 28 April 2000). The appellant’s contention was that the Driver’s Declaration should be construed without regard to the telephone conversation and that the matter was to be resolved simply by construing the documents.

59 This argument must be rejected for at least two reasons. First, the questions in ‘b’ in the 2004 proposal form provided their own temporal limits; in some cases it is five years and in other cases it is quite clearly unlimited. Even if the answer to Question B in the Driver’s Declaration could be construed to be limited to a period of three years there is no reason why one should take the further step of construing it as providing a limit on the periods referred to in question b of the 2004 proposal form. The important thing is the matter disclosed and there is no reason to import a time limit into the disclosure inconsistent with the question which is asked. Secondly, even if it is appropriate to exclude the telephone conversation from consideration, it would not be appropriate to exclude the letter dated 29 April 2003. When the Driver’s Declaration is read with the letter there is no statement that only licence disqualifications or cancellations for the last three years were being disclosed.

60 The third argument is that the answers given by the appellant were ‘obviously incomplete’ and therefore either the respondent had waived compliance with the duty of disclosure under s 21(3) of the Act or the answers were not misrepresentations by reason of s 27 of the Act. There was a suggestion in the appellant’s written submissions that it was contending that the questions were ambiguous (see s 23 of the Act). We see no ambiguity in the questions. There was also a reference to s 21A of the Act but the appellant abandoned any reliance on that section in the course of its oral submissions.

61 We do not think that it can be said that the answers were obviously incomplete. There would have been no reason for a reader of the 2004 proposal form to draw any conclusion other than the conclusion that the Driver’s Declaration and Fukura proposal disclosed all convictions of the nominated drivers in connection with intoxicating liquor.

62 Finally, the appellant submitted that the trial judge ought to have found that there was no misrepresentation because of the operation of s 26(1) of the Act. That section operates where a statement was made by a person which was in fact untrue but which was made on the basis of a belief that a reasonable person in the circumstances would have held. The statement in question is the assertion by Mr O’Shanassy as the governing mind of the appellant that the only relevant conviction within question b(v) was the 2002 conviction. This statement was untrue because the other relevant conviction was the 1999 conviction. To engage the subsection the appellant needed to show that Mr O’Shanassy made the statement on the basis of a belief and that belief was one that, in the circumstances, a reasonable person would have held. The argument fails on a number of points. First, the appellant did not articulate the precise belief it said Mr O’Shanassy held. Was it that disclosure for three years was sufficient? Was it that disclosure for five years was sufficient? Was it that whatever the period, the appellant had made sufficient disclosure? Secondly, Mr O’Shanassy did not give evidence and it would be difficult to draw any inference about his belief without direct evidence from him. Thirdly, and more importantly, the trial judge’s findings about Mr O’Shanassy’s actual state of mind (the challenge to which we reject below) would preclude any finding that a reasonable person would hold any belief that could form the basis of the untrue statement. We reject the appellant’s fourth argument.

63 In our opinion, the appellant’s challenge to the trial judge’s conclusion that the respondent made out its non-disclosure and misrepresentation defence and that its liability be reduced to nil under s 28(3) of the Act must be rejected.

SEcond Issue: Could the Trial Judge make adverse findings about Mr O’Shanassy

64 Another aspect of the appellant’s complaints about the trial judge’s treatment of the misrepresentation and omission cases concerns an agreement which was reached between counsel that the insurer would make no submission based upon Jones v Dunkel if Mr O’Shanassy did not give evidence. This agreement was openly announced in Court before the trial judge and, it may reasonably be surmised, it was in reliance in part upon that agreement that the appellant’s representatives then made the decision not to call Mr O’Shanassy as a witness.

65 The trial judge made extensive findings about Mr O’Shanassy which were of a serious nature. These included, for example, findings that Mr O’Shanassy’s conduct was “disingenuous and lacking in integrity” (at [34]) and that he had misrepresented his wife’s driving record to the insurer (at [35]). Putting the matter generally, the gravamen of these findings was that Mr O’Shanassy had set out deliberately to mislead the insurer. Mr McCulloch SC, who with Ms Gleeson appeared for the appellant, submitted that findings of that kind were tantamount to findings of fraud and that they severely impugned Mr O’Shanassy’s professional reputation and standing as a solicitor. The burden of Mr McCulloch SC’s argument was that, in circumstances where it had been agreed between counsel that no submission would be made based upon Jones v Dunkel, this was an unfair way to proceed. If the appellant had been put on notice that the trial judge was going to make findings of serious misconduct against Mr O’Shanassy then it was likely that the appellant would have sought to re-open its case to call him as a witness so that he could confront and defeat those suggestions. The combination of the agreement between counsel about Jones v Dunkel, its announcement before the trial judge and his Honour’s failure to indicate that he was going to make findings of that kind had resulted in an outcome which was unfair, not only to the appellant, but also to the subject of the findings himself, Mr O’Shanassy.

66 It is convenient to begin with the issues which were live in the proceedings and which touched upon Mr O’Shanassy’s state of mind. As we have already noted above the respondent put a case to the trial judge that the appellant had made two false representations to it which gulled it into issuing the appellant with the policy upon which the appellant had then sought to rely. These two representations were to the effect, first, that the only offence for which Mrs O’Shanassy had been convicted during the period September 1999 until September 2004 was the offence of not wearing a seatbelt; and, secondly, that Mrs O’Shanassy had not been charged or convicted during the same period in connection with intoxicating liquor or drugs. The appellant’s pleaded response to those allegations was that it denied them. This left unclear, of course, whether it denied that the representations had been made or whether it accepted they had been made but asserted that they were true.

67 At the trial the position of the appellant came into view. Based on the construction of the various written disclosures made by the appellant to the respondent (set out above) it was put that no such representation had ever been made. More importantly for present purposes, however, it is apparent that a case was also put that, even if the representations had been made, they were not in fact false. Given that there is no dispute that Mrs O’Shanassy had been convicted in 1999 of driving with more than the prescribed content of alcohol in her blood and disqualified on that occasion for a substantial period of 18 months a question naturally arises as to how a representation to the contrary could have been other than false. The answer lies in the appellant’s defence that the appellant did believe that the statements made by it in the various disclosures were, taken together, true and that a reasonable person in its circumstances would have held the same view. As we have already noted, this argument engaged s 26(1) of the Act which operates so that a statement by a person to an insurer which is, in fact, untrue will not be treated as a misrepresentation if it “was made on the basis of a belief that the person held, being a belief that a reasonable person in circumstances would have held”. An uncontroversial use of s 26(1) is afforded by the example of an insured who states in a proposal that a vehicle is in good repair when, unbeknownst to the insured, there is a serious – but undetected – problem with the engine. The defence based on s 26(1) was not formulated in the pleadings but there was no issue before us that the trial was conducted on the basis that it was an issue. Consistently, the appellant invoked s 26 as an issue in the appeal at paragraph 6 of written submissions in reply.

68 By raising s 26(1), however, the appellant put directly in issue the question of whether it held the belief that what it had said in its disclosures was true. And, since the person who completed the disclosures was Mr O’Shanassy, it followed that the appellant had made the question of his belief in the truth of the disclosures an issue which inevitably had to be resolved by the trial judge.

69 The pursuit of this issue occupied not some little time at the trial. The appellant, through Mr O’Shanassy, had executed three sets of proposals and the respondent sought to demonstrate, in each case, that Mr O’Shanassy could not have believed that they were true. Although Mr O’Shanassy did not ultimately give evidence his wife certainly did and her account, perhaps unfortunately for Mr O’Shanassy, placed him in the very thick of it. The first proposal, which did not reveal that her licence had been cancelled in 1999 for driving under the influence, had been preceded – according to Mrs O’Shanassy – by the telephone call referred to at paragraph [32] above. Mrs O’Shanassy’s evidence in chief was that during that telephone call Ms Jacks had told her that she did not need to provide any information about matters more than 3 years old. Ms Jacks denied saying any such thing and it was also inconsistent with a covering letter written the same day which made no reference to licence cancellation disclosures being subject to a 3-year limit. On the other hand, the proposal as completed had inserted next to the section dealing with cancellation of licences the handwritten figure “3 yrs”.

70 This contradiction in the evidence opened up the real possibility that Mrs O’Shanassy’s evidence about the telephone call might be disbelieved. The possibility was not merely conjectural for it is quite plain that the insurer was actively contending that her evidence should be rejected and that of Ms Jacks accepted. Because Mrs O’Shanassy had said that Mr O’Shanassy had been present during the telephone call it was obvious that a rejection of her evidence would have carried with it significant risks to Mr O’Shanassy’s credit and this, in turn, could have had difficult and unsought for consequences for the appellant’s contention that Mr O’Shanassy really believed that the disclosures were true.

71 We emphasise this because during the hearing of the appeal Mr McCulloch SC sought to suggest, in effect, that Mr O’Shanassy and the appellant had been given no notice during the trial that his Honour was minded to make adverse findings about Mr O’Shanassy’s credit thereby depriving him of the opportunity of confronting his accusers in the witness box. That argument should be rejected. To begin with, it is unsupported by any evidence. Neither Mr O’Shanassy nor the solicitors and counsel who conducted the trial on the appellant’s behalf gave evidence before us that they did not know that Mr O’Shanassy’s credit was in issue. The reason for this is tolerably clear. By raising the s 26(1) defence the appellant had put Mr O’Shanassy’s credit directly in issue and it was obvious that his credit had been dragged further into the debate about what was said to Ms Jacks. There was in that circumstance no unfairness in the trial judge proceeding to resolve the very issue put up by the appellant for consideration, namely, whether the s 26(1) defence was made out.

72 The trial judge weighed all of this evidence and found that Mrs O’Shanassy’s evidence about it was untrue and that Ms Jacks had not suggested that information older than 3 years need not be provided. As already noted this had serious adverse consequences for Mr O’Shanassy. Since Mr O’Shanassy was a party to this telephone call it would have been open to the appellant to call him as a witness to corroborate Mrs O’Shanassy’s version of events. Without his evidence, on one side there was Mrs O’Shanassy’s oral testimony and the form itself with the annotation “3 yrs”; on the other, the covering letter and Ms Jacks’ testimony. The decision not to call him involved therefore a substantial forensic decision.

73 It is against that background that the agreement reached between counsel falls to be considered. Counsel for the appellant said this:

There was, as your Honour will recall, a proposal that Mr O’Shanassy would be called, but it does not appear, in my respectful submission, to add anything to the evidence already here, and my friend has indicated to me that no inference will be sought to be submitted ought to be drawn by reason of him not being called, so that is – subject to those qualifications, that is the applicant’s case in reply.

(our emphasis)

74 Of course, Mr O’Shanassy could have added very directly to the evidence of the conversation with Ms Jacks. He was an officer of the Court and as such his testimony would have immediately complicated the questions of credit with which the trial was confronted. On the other hand, calling him would have exposed him to the rigours of cross-examination not just about the telephone call but also about the subsequent disclosures.

75 This was a particularly difficult decision for the appellant’s representatives to make because the appellant had conducted its case on a basis which made Mr O’Shanassy’s mental states an issue by invoking s 26(1). It being an issue a point was going to come in the proceedings in which both parties would have to make submissions as to whether Mr O’Shanassy genuinely believed that the statements in the disclosures, taken altogether, were true.

76 The question which arises then is whether the respondent was disqualified from submitting that Mr O’Shannassy was lying in the disclosures. The appellant’s argument is that the above exchange had the consequence that the insurer was not permitted to make any adverse remarks about Mr O’Shanassy.

77 We reject this argument for two reasons. First, the agreement is quite clear – it was not agreement not to make adverse remarks about Mr O’Shanassy – but rather not to make adverse remarks about Mr O’Shanassy’s failure to give evidence. Secondly, the surrounding context which we have just recounted strongly supports that interpretation.

78 Before us the agreement reached was referred to by Mr McCulloch SC as the “Jones v Dunkel agreement” and in this we think he was essentially correct. The rule in Jones v Dunkel is one of the most invoked but least understood rules in litigation. It is a principle of commonsense (Jones v Dunkel at 321 per Windeyer J; Ghazal v Government Insurance Office (NSW) (1992) 29 NSWLR 336 at 343 per Kirby P, Mahoney and Clarke JA agreeing) and is directed to fact triers. At its root is the concept – explicated by Wigmore on Evidence (3rd ed, 1940, vol. 2, s. 285, p. 192) – that, where a party does not call a witness or tender evidence when that evidence might have been expected to elucidate the question before the court, one available inference is that this has occurred because the party is afraid to lead to the evidence. It being a rule of commonsense that inference need not always arise. The party, for example, may have some other explanation for why the evidence was not produced.

79 But the fact that one can infer that a party was afraid to call some particular witness or tender some particular document can take a trier of fact only so far. It is accepted that where a party fails, without explanation, to call a witness who that party might have been expected to call and whose evidence might have elucidated the matter in dispute, then the inference may be drawn that the evidence of the absent witness would not have assisted the party that failed to call that witness: Jones v Dunkel at 308, 312 and 320-321. By itself that inference is frequently somewhat barren, for knowing that the evidence of a witness would not have assisted tells one nothing about what the witness’s evidence affirmatively would have been. Often more directly useful is the allied principle that in such a case the trier of fact may more confidently draw any inference unfavourable to the party that failed to call that witness if that witness appears to be in a position to cast light on whether the inference should be drawn: Jones v Dunkel at 308 per Kitto J, 312 per Menzies J, and 320-321 per Windeyer J. Neither inference is mandatory and, generally speaking, these inferences only become material where the balance of the evidentiary record is equivocal.

80 We were not taken to any part of the trial judge’s reasons which suggests that his Honour used any reasoning remotely of this kind. The reason for this is obvious. There was no need for his Honour to do so. The trial judge formed the view that Mr O’Shanassy did not believe that the answers given in the disclosures were true because he formed a negative view as to his credit from two sources. The first was Mrs O’Shanassy’s evidence which directly implicated him in the telephone call with Ms Jacks. Since his Honour concluded that Ms Jacks did not say that nothing older than 3 years needed to be disclosed it followed that Mr O’Shanassy could not have believed that the disclosures were true. This was inconsistent with the case being put by the appellant. The second was the form of the disclosures themselves which his Honour regarded as unsatisfactory. There was no need, in those circumstances, for the trial judge to explore what else might have been said against Mr O’Shanassy by reason of the fact that he did not chance the witness box.

81 Counsel for the respondent did not submit to the trial judge that he ought to draw a Jones v Dunkel inference against Mr O’Shanassy and the trial judge did not do so. The appellant’s argument impermissibly elides general condemnation of Mr O’Shanassy’s credit based on the available evidence with the drawing of an adverse inference by reason of his failure to give evidence. These matters are plainly distinct and the argument correspondingly unsound. The variant to it developed in oral argument – that it was unfair to make adverse findings against Mr O’Shanassy without warning him that this was going to occur – founders for lack of evidence to support it and because of the fact, as is plain, that Mr O’Shanassy’s mental states and the perils to his credit were issues at trial raised by the appellant’s use of s 26(1).

Third Issue: The question of leave to amend the reply

The proposed amendment

82 The proposed amendment was in the following terms:

(1) [I]t [Sagacious] did not relevantly consent to the vehicle being driven by Mrs O’Shanassy when she was affected by alcohol;

(2) [T]here was no basis for the insurer to dispute that the insured had no reason to suspect that she was under the influence of alcohol when driving (which was denied) so that the two alcohol-based exceptions to the policy did not apply; and

(3) [T]he insurer was in breach of s 13 of the Act by denying the claim or the insurer was prevented by s 14(1) of the Act from relying on either relevant exception.

83 Sections 13 and 14 of the Act provided:

13 The duty of the utmost good faith

A contract of insurance is a contract based on the utmost good faith and there is implied in such a contract a provision requiring each party to it to act towards the other party, in respect of any matter arising under or in relation to it, with the utmost good faith.

14 Parties not to rely on provisions except in the utmost good faith

(1) If reliance by a party to a contract of insurance on a provision of the contract would be to fail to act with the utmost good faith, the party may not rely on the provision.

(2) Subsection (1) does not limit the operation of section 13.

(3) In deciding whether reliance by an insurer on a provision of the contract of insurance would be to fail to act with the utmost good faith, the court shall have regard to any notification of the provision that was given to the insured, whether a notification of a kind mentioned in section 37 or otherwise.

84 The proposed amendment was first raised with counsel for the respondent the day before the hearing began – a Sunday. Its purpose was to enable the appellant to rely on a contractual exception from the exclusions in the insurance policy. In order to obtain the benefit of the exception the insured was required to prove that it did not consent to Mrs O’Shanassy driving or being in charge of the motor vehicle when or if she was affected by alcohol and also that the insured had no reason to suspect that she was so affected (although before the trial judge the appellant would not accept that it bore such an onus).

85 The exception appeared as a note in the contract, which counsel referred to as “the proviso”. It read:

Claims will be paid to the extent that there are not any relevant statutory provisions to the contrary or where you can prove that you did not consent to the motor vehicle being driven by or being in the charge of a person when so affected and we agree that you had no reason to suspect that the driver was under the influence of alcohol or any drug.

The argument below

86 Counsel for the appellant below informed the court that within the last week proofs of evidence had been served from Mr and Mrs O’Shanassy which included the material that would be led to establish absence of consent. He referred to Mrs O’Shanassy calling her husband from a licensed club where she had been to play the poker machines, deciding to leave immediately afterwards but “sculling” two double whiskeys and coke before doing so. In those circumstances, he submitted, there could be “no serious suggestion or no reasonable basis for contending that Sagacious Legal consented to Mrs O’Shanassy being in charge of the motor vehicle in whatever state she was in”. He added that two telephone calls Mr O’Shanassy made to his wife went to message bank.

87 Counsel below also informed the court that the significance of “the point” did not occur to him until two days beforehand while he was preparing the opening.

88 The appellant called no evidence on the application.

89 The trial judge summarised the appellant’s arguments in a way the appellant accepted was a fair description of its position. He said (in Sagacious Legal (No 2)):

[12] The insured argued that by joining issue with the insurer’s denial of liability on the basis of the pleaded exceptions, it was clear that the insurer would be faced with having to deal with the subject matter of the notation to the general exceptions in the policy. It also argued that the only relevant factual inquiries concerned what occurred in considering the claim as at the date of the alleged breach, and, the question of whether or not there was any prejudice to the insurer based on the material that it now had access to concerning Mrs O’Shanassy’s consumption of alcohol. The insured said that it would make a relevant admission that Mrs O’Shanassy had alcohol problems at the time of the accident after ascertaining precisely what might be sought by the insurer. There was some medical evidence produced in response to the orders I made on 4 March 2010 that suggested that she did have an alcohol problem, as I understand is common ground between counsel.

[13] The insured next addressed the factual question raised in relation to prejudice. It characterised this as whether or not it could be said that the insurer would now have to deal with the issue of whether the insured had consented to Mrs O’Shanassy driving the vehicle at the time of the accident. There is apparently some issue as to whether she was, or may have been, an employee of the insured at the time of the accident, or at some other stage. This may or may not have provided the insured with notice of the kind that could be used as evidence from which an inference of consent might be drawn.

[14] The insured also argued that the insurer has not yet lost the ability to grant indemnity, and can still do so. It argued that the provisions of ss 13 and 14(1) of the Act were attracted because, first, at the time of the denial of liability, in some way the insurer was not acting in good faith in relying upon the policy notation identifying how it should be informed about the insured’s lack of consent to the vehicle being driven and the insured not having any reason to suspect that Mrs O’Shanassy was under the influence of alcohol at that time. Secondly, the insured argued that as at the time of the trial, and in all the circumstances, the inference should be drawn that the insurer’s reliance upon the contractual exceptions relating to alcohol was otherwise than in good faith, and that its reliance on the provisions of the policy amounted to a failure to act in the utmost good faith. These issues under the Act have only been raised by the draft pleading now for the first time.

90 When asked to particularise how ss 13 and 14 of the Act were attracted, the appellant argued that the respondent’s conduct in taking the premium and refusing to pay the claim amounted to a breach of good faith because the appellant relied upon the exception that it did not consent to the motor vehicle being driven by the driver.

91 At the time the application was made the trial judge was informed that 17 witnesses had been subpoenaed to give evidence. They included a number of police, emergency services officers and others from various parts of New South Wales.

92 Mr Braham SC, who appeared for the respondent at the trial and on appeal, told his Honour that the first his client knew of the matters raised in the proofs of evidence was when it was served with them. He tendered correspondence passing between the parties and answers to interrogatories provided by the appellant to show that a different approach had earlier been taken. It should be noted at this point that the answers to interrogatories were verified by Mr O’Shanassy, who said that, having made reasonable enquiries of other officers and agents of the company, to the best of his knowledge, information and belief, he did not know whether his wife had consumed any alcoholic beverage in the 12 hours before the accident.

The reasons of the trial judge

93 The trial judge rejected the application for a number of reasons.

94 First, his Honour was plainly of the view that the bad faith allegation was hopeless. He said that on a reading of the notation as a whole the insured had an obligation to raise with the insurer the basis upon which it did not consent and to prove that the insured [scil.] had no reason to suspect that she was under the influence of alcohol at the time she was driving the car. He observed that the respondent had asked for information about why it ought not to have made its assumption that consent to drive the vehicle had been given to Mrs O’Shanassy as a nominated driver and been met with silence, apart from a bare assertion that the insurer was incorrect to make the assumption. He said (at [23]):

I see nothing that could possibly give rise to an allegation that the insurer, having asked the relevant question and being met with silence, could be said to be acting outside its obligation of the utmost good faith in relation to a matter arising in relation to the insurance policy. I cannot understand how the insured can argue that, by it refusing to give the insurer information about whether it had consented to Mrs O’Shanassy driving at the time, which could only be known by the insured, the insurer had been in breach of its obligation of good faith by continuing to rely upon the assumption it had identified. That assumption had simply been denied in circumstances where the policy contained the notation.

95 The appellant had submitted that, at the time the appellant disputed the correctness of the assumption, Mrs O’Shanassy was the subject of a criminal charge and was entitled to remain silent and, although the charge was later dismissed, that occurred only after the refusal of indemnity had been communicated. His Honour disposed of this submission by saying that “that has nothing to do with whether or not the insured gave consent to her driving the car, whether or not she was relevantly affected by alcohol” (at [24]).

96 Secondly, his Honour noted that an allegation of a breach of the utmost good faith by an insurer requires the pleading of particular facts the insured must establish to make good its allegation so that the insurer can know the case it has to meet, citing Dare v Pulham (1982) 148 CLR 658 at 664 per Murphy, Wilson, Brennan, Deane and Dawson JJ. He considered that the proposed amendment “fails to meet the threshold of pleading the material facts by reference to which [the] conduct could be proved or be thought to identify what it was that amounted to a lack of the utmost good faith arising out of those circumstances” (at [27]).

97 Thirdly, his Honour said that the proposed amendment would require the respondent, during the course of the trial, to investigate the new issue, interview new witnesses and put evidence together to deal with it. He observed that it raised significant issues that had not adequately been investigated before the trial. He said (at [32]):

The current pleadings raise a number of important and difficult issues of insurance and general law, and require a detailed factual inquiry. I do not consider that it would be fair to grant the proposed amendments and to permit the trial to proceed today where the issues raised by them had not been considered and investigated with the thoroughness that the other issues for the trial today have been. As I indicated in my judgment, Sagacious Legal Pty Ltd v Wesfarmers General Insurance Limited [2010] FCA 274, litigation in this Court has for a considerable period been conducted on the basis that parties cannot leave footprints in the sand and must lay their cards on the table promptly and early so that all the true issues are identified and can be fairly tried in due course. I consider that I would be forced to grant an adjournment to the insurer were I to permit these amendments to be made.

98 In that event, his Honour remarked, not only would “very considerable costs” be thrown away in its preparation but a large number of witnesses would be disrupted and the hearing of factual evidence from witnesses about their recollection of events, then almost two years old, would be further delayed. He pointed to an observation of Lord Hailsham in Reg v Lawrence [1982] AC 510 at 517B-C that “the whole quality of justice is undermined by delay that affects the recollection of individuals”. He noted that it had always been open to the appellant to plead the new case and held that it had had “a full and proper opportunity” to do so. He referred to the fact that five days had been set aside for the trial. He said that vacating those dates would mean that other parties who may have been able to have their case heard at that time were deprived of those dates. He considered that the realisation by counsel for the appellant on the weekend before the hearing was due to start was insufficient justification for allowing the introduction of wholly new issues at such a late stage. He said he had had regard to the considerations identified in Aon Risk Services Australia Pty Limited v Australian National University (2009) 239 CLR 175 and particularly at 211-215, [92]-[103] (“Aon”). He said he had given consideration to the fact that both parties were corporations but he was mindful that the appellant was a small corporation and that the respondent, unlike the individuals associated with the appellant, had no personal interest in the outcome of the litigation. Still, he said he thought there were “elements of non-compensable inconvenience and stress, both on the insurer’s witnesses, and elements of convenience to other litigants in the Court in requiring these parties to have pleaded and articulated their cases clearly from the outset”. He expressed the view that reliance on the exception to the exclusion in the policy should have been raised a lot earlier. He concluded that the disadvantage to the respondent of adjourning the trial required that he refuse the amendment application.

The argument on appeal

99 The appellant submits that the trial judge fell into error. It accepts that to succeed it must bring itself within the well-known principles of House v The King (1936) 55 CLR 499 at 504-505:

It is not enough that the judges composing the appellate court consider that, if they had been in the position of the primary judge, they would have taken a different course. It must appear that some error has been made in exercising the discretion. If the judge acts upon a wrong principle, if he allows extraneous or irrelevant matters to guide or affect him, if he mistakes the facts, if he does not take into account some material consideration, then his determination should be reviewed and the appellate court may exercise its own discretion in substitution for his if it has the materials for doing so. It may not appear how the primary judge has reached the result embodied in his order, but, if upon the facts it is unreasonable or plainly unjust, the appellate court may infer that in some way there has been a failure properly to exercise the discretion which the law reposes in the court of first instance. In such a case, although the nature of the error may not be discoverable, the exercise of the discretion is reviewed on the ground that a substantial wrong has in fact occurred.

100 The appellant’s position, in effect, is that the refusal of the adjournment was, on the facts, “unreasonable or plainly unjust” so that this Court should infer that a substantial wrong has occurred and the discretion miscarried. As it was put in oral argument, the view that was reached in the court below was “so wrong” that this Court should interfere. For the reasons that follow we are of the view that the challenge to the exercise of the trial judge’s discretion must fail.

The arguments considered and rejected

101 The appellant’s first argument was that there was no good reason to refuse the adjournment. It submitted that the only additional evidence that would have been required was evidence from Mr O’Shanassy to the effect that he did not consent to his wife driving the vehicle while she was intoxicated. He would have been believed, it went on, because that goes without saying anyway and, as a legal practitioner, it is scarcely likely he would have a company of which he was a director give consent to an asset being driven by someone who was at the time intoxicated. Mrs O’Shanassy, counsel said, was hiding her drinking and gambling from him. Mrs O’Shanassy’s evidence supported that statement.

102 We reject the submission. The proposed new defence opened up the question of the extent of Mr O’Shanassy’s knowledge of his wife’s drinking habits. Whether or not he or his wife gave exculpatory evidence, other evidence may have undermined it.

103 It is possible that some of the witnesses on the DUI issue might have been able to give some of this evidence. But there is every chance that there were others, who could have given evidence of their observations of the interactions of Mr and Mrs O’Shanassy or of conversations they had overheard between them during the same or a different or longer period of time. That evidence would affect the reliability of any evidence Mr O’Shanassy would have to have given about what he knew about his wife’s habits at the material time. The appellant said it was prepared to concede that Mr O’Shanassy was aware that his wife had a drinking problem (although Mrs O’Shanassy, herself, denied she ever did). The actual concession made at trial was that, if the amendment were allowed, the appellant would admit that “Mrs O’Shanassy had alcohol problems prior to this incident”. But such a concession could scarcely dispose of the question whether her husband consented to her driving under the influence or had reason to suspect that she did. Indeed, it would not amount to an admission that he or the company knew that she did. The extent of Mr O’Shanassy’s knowledge of her driving and drinking practices was critical. As the appellant accepted in the court below, there were several telephone conversations between Mr and Mrs O'Shanassy on the evening in question, including during the period of alleged intoxication. As the respondent submitted, it was entitled to investigate such evidence as may have been available concerning the regularity with which Mrs O'Shanassy drank alcohol and drove, and what Mr O'Shanassy (as the controlling mind of the appellant) might have known about this. It pointed to such obvious sources of information as the places where Mrs O’Shanassy drank, the domestic assistant who looked after her children while she went drinking, the people who worked at the appellant’s law firm, the publican, family doctors, and friends. Information derived from those investigations would plainly be relevant to the question whether Mr O’Shanassy consented to his wife driving the car whilst affected by alcohol and would have been a fertile basis for cross-examination of both Mr and Mrs O’Shanassy. In addition, the respondent also had an interest in investigating whether Mrs O’Shanassy may have occupied a role within the appellant that gave her the authority to consent on its behalf. It appears that there was some material suggesting she was employed by the company in a senior capacity.

104 In any case the evidence would also be relevant to the second limb of the proviso. It is to be remembered that the exception only operated where the insurer agreed that the insured had no reason to suspect that the driver was under the influence of alcohol. If Mr O’Shanassy knew his wife had a problem with alcohol, knew she regularly drove to and from a licensed club and knew that she had been at the club immediately before the accident, the respondent might reasonably have concluded that he had reason to suspect that she drove on the day of the accident whilst she was affected by alcohol.

105 The appellant also submitted that “it cannot now be argued that the evidence of what the insurer would have done could be in any way relevant”.

106 This submission cannot be accepted either. As counsel for the respondent submitted, the insurer was entitled to make enquiries of the claims officers who dealt with the appellant's claim at the time indemnity was refused (in December 2008), in order to ascertain whether they would have agreed that the appellant had no reason to suspect Mrs O'Shanassy was driving under the influence of alcohol. Contrary to the appellant's submission, evidence of that kind is not irrelevant; indeed, its relevance was expressly conceded by the appellant in the Court below. Such evidence is essential if the insurer is to discharge the onus which the second limb of the proviso cast upon it.

107 Certainly, the allegations of bad faith raised by the proposed amended pleading required investigation and claims officers of the respondent are likely to have been required to testify.

108 It is possible that some, if not all, of these enquiries could have been made whilst the trial was on foot or after a short adjournment, as the appellant contended. Nevertheless, we do not consider that the trial judge’s discretion miscarried because he was of the opinion that the respondent should not have been required to conform to a timetable set by the appellant, particularly where the circumstances that gave rise to the problem were not of the respondent’s making.

109 It may be accepted, as the appellant submitted, that nothing the High Court said in Aon warrants denying applications as a matter of course. It is true that the trial judge concluded his judgment by saying that “the disadvantage to the insurer of adjourning the trial” required him to refuse the application. But on a reading of the judgment as a whole there is no basis for saying that his Honour did so “as a matter of course” or that he wrongly applied the principles in Aon.

110 The plurality observed in Aon at 214-215 [102] in the context of r 21 of the Courts Procedures Rules 2006 (ACT) (which is in similar terms to ss 37M and 37N of the Federal Court of Australia Act 1976 (Cth)):

It is the extent of the delay and the costs associated with it, together with the prejudice which might reasonably be assumed to follow and that which is shown, which are to be weighed against the grant of permission to a party to alter its case. Much may depend upon the point the litigation has reached relative to a trial when the application to amend is made. There may be cases where it may properly be concluded that a party has had sufficient opportunity to plead their case and that it is too late for a further amendment, having regard to the other party and other litigants awaiting trial dates. Rule 21 makes it plain that the extent and the effect of delay and costs are to be regarded as important considerations in the exercise of the court’s discretion…

111 His Honour took these matters into account. He also had regard to the inconvenience an adjournment would cause to the witnesses who were waiting to give evidence. Inconvenience to witnesses is not irrelevant. In Aon at 214 [101] the plurality referred to the strain of impending litigation and the disappointment that employees and office bearers of corporate parties will feel when it is not brought to an end. These remarks apply equally (if not more so) in the case of third parties.

112 The trial judge’s application of the reasoning in Aon does not disclose any appealable error.

113 The appellant complained that at the trial “there was no elucidation of particular pieces of evidence, particular statements from particular witnesses, which could have been examined to see whether in truth and in substance there was anything more than the requirement that my learned friend and his solicitors work a bit harder”. But that is scarcely surprising. The respondent had not had the opportunity to conduct the investigation in the first place.

114 The appellant made much in argument of the fact, which was not disputed, that its counsel at the trial had only become alive to the point the day before the hearing was due to start. The trial judge was cognisant of this and took it into account. But the appellant, itself, was very much alive to the point at the relevant time. On 10 June 2008 the respondent wrote to the appellant advising it that it was investigating the circumstances of the incident to determine whether indemnity would be extended to it. The letter enclosed a statutory declaration form to be completed by the driver. The penultimate paragraph of the letter was in the following terms:

We assume that the driver was driving the vehicle with the authority of Sagacious Legal Pty Ltd. We reserve our client’s rights to pursue recovery from the driver if Sagacious Legal Pty Ltd denies the driver was driving without [sic] the knowledge and consent of Sagacious Legal Pty Ltd.

115 The appellant declined to provide a statutory declaration until the criminal proceedings against Mrs O’Shanassy had been resolved. Its response to the matters raised in the last paragraph of the letter of 10 June 2008 was curt.

The assertion stated in the penultimate paragraph of your letter is incorrect.

116 The appellant relied on this statement to show that the respondent was on notice of its position. But the statement does not establish that the appellant did not consent, merely that the respondent was not entitled to assume that it did. On 24 April 2009, after the respondent refused indemnity, the appellant’s solicitors wrote a lengthy letter in response to the matters the respondent raised, which did not include mention of the proviso or any assertion that the appellant did not consent to Mrs O’Shanassy driving the car under the influence of alcohol. At no time did the appellant set out to prove that it did not consent. On 7 May 2009 the respondent’s solicitors wrote again to the appellant’s solicitors in which it stated (amongst other things):

We note our previous request to your client for confirmation of the capacity in which Lana O’Shanassy was driving the insured vehicle in question and whether this was with the express permission and consent of your client has not been responded to.

117 The only response to this letter appears to be the institution of the proceeding.

118 It was not irrelevant for his Honour to have regard to such matters. The appellant’s silence up until the eve of the hearing was inconsistent with the positive case it had to make to bring itself within the proviso. It was well open to his Honour to conclude, as he did, that this was the result of a deliberate forensic decision not to provide the information (at [20]).

119 The appellant also argued that the trial judge did not have regard to the fact (as its counsel put it) that the amendment, if accepted, would have been decisive. The matter was put a little differently in its written submissions, where it contended that “allowing the amendment with respect to the proviso issue may have rendered the large portion of the trial relating to the PCA and other like issues otiose” and would have resulted in “a net saving of time”. The suggestion was never made to the trial judge and we have difficulty seeing how adding the issues raised by the proviso would have reduced the number of issues or the extent of the evidence.

120 In any case, unless the amendment would have had the suggested effect, the result contended for does not follow.

121 In our view the submission fails anyway because, as counsel for the appellant conceded during argument, if the facts alleged by the proposed amendment were made out, that would only dispose of one part of the proceeding. The appellant could still have lost the case on the basis of misrepresentation or non-disclosure. In its written submissions it stated that its position was that, had the amendment been granted, it would not have contested the issues relating to the various exclusions that occupied most of the hearing time in the Court below. But no such concession was made to the trial judge.

122 The plurality in Aon observed in their concluding remarks at 217 [111]:

An application for leave to amend a pleading should not be approached on the basis that a party is entitled to raise an arguable claim, subject to payment of costs by way of compensation. There is no such entitlement. All matters relevant to the exercise of the power to permit amendment should be weighed.

123 His Honour had regard to the significance of the amendment for the appellant but he gave it less weight or importance than the appellant argued it should have received. That does not bespeak error.

124 His Honour’s discretion did not miscarry.

Fourth Issue: Costs