FEDERAL COURT OF AUSTRALIA

Commissioner of Taxation v American Express Wholesale Currency Services Pty Limited [2010] FCAFC 122

IN THE FEDERAL COURT OF AUSTRALIA | |

| Appellant | |

AND: | AMERICAN EXPRESS WHOLESALE CURRENCY SERVICES PTY LIMITED Respondent |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. The appellant be granted leave to amend the notice of appeal dated and filed 10 July 2009 to include the additional grounds referred to in the affidavit of Marlene Binnekamp sworn on 11 November 2009.

2. The appeal be allowed.

3. The orders made by the Honourable Justice Emmett on 19 June 2009 be set aside and in lieu thereof order:

3.1 the appeal against the objection decision be allowed in part.

3.2 save as to the respondent’s objection to assessment to penalties pursuant to s 284-75(1) in Schedule 1 of the Taxation Administration Act 1953 (Cth) (‘additional tax’), the objection decision notified by letter dated 21 December 2006 (‘the objection decision’) be upheld.

3.3 by consent, that part of the objection decision disallowing the respondent’s objection to assessment to penalties, and the notice of assessment to penalties dated 27 April 2006, be set aside.

4. Within 10 days of the date of judgment the parties file and serve short submissions as to costs.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules. The text of entered orders can be located using Federal Law Search on the Court’s website.

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 699 of 2009 |

ON APPEAL FROM THE FEDERAL COURT OF AUSTRALIA |

BETWEEN: | COMMISSIONER OF TAXATION Appellant |

AND: | AMERICAN EXPRESS INTERNATIONAL INC Respondent |

JUDGES: | DOWSETT, KENNY AND MIDDLETON JJ |

DATE OF ORDER: | 17 SEPTEMBER 2010 |

WHERE MADE: | MELBOURNE (HEARD IN SYDNEY) |

THE COURT ORDERS THAT:

1. The appellant be granted leave to amend the notice of appeal dated and filed 10 July 2009 to include the additional grounds referred to in the affidavit of Marlene Binnekamp sworn on 11 November 2009.

2. The appeal be allowed.

3. The orders made by the Honourable Justice Emmett on 19 June 2009 be set aside and in lieu thereof order:

3.1 the appeal against the objection decision be dismissed.

3.2 the objection decision notified by letter dated 21 December 2006 (‘the objection decision’) be upheld.

4. Within 10 days of the date of judgment the parties file and serve short submissions as to costs.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules. The text of entered orders can be located using Federal Law Search on the Court’s website.

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 698 of 2009 |

ON APPEAL FROM THE FEDERAL COURT OF AUSTRALIA |

BETWEEN: | COMMISSIONER OF TAXATION Appellant

|

AND: | AMERICAN EXPRESS WHOLESALE CURRENCY SERVICES PTY LIMITED Respondent

|

IN THE FEDERAL COURT OF AUSTRALIA | |

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 699 of 2009 |

ON APPEAL FROM THE FEDERAL COURT OF AUSTRALIA |

BETWEEN: | COMMISSIONER OF TAXATION Appellant

|

AND: | AMERICAN EXPRESS INTERNATIONAL INC Respondent

|

JUDGES: | DOWSETT, KENNY AND MIDDLETON JJ |

DATE: | 17 SEPTEMBER 2010 |

PLACE: | MELBOURNE (HEARD IN SYDNEY) |

REASONS FOR JUDGMENT

DOWSETT J:

INTRODUCTION

1 These appeals arise under the A New Tax System (Goods and Services Tax) Act 1999 (Cth) (the “GST Act”). I have had the benefit of reading the reasons prepared by Kenny and Middleton JJ (the “joint reasons”). I gratefully adopt their Honours’ summary of the facts of the case. It will not be necessary for me to set out, in full, the facts or the relevant legislative provisions and regulations. I shall refer to the respondents collectively as “American Express” and to the appellant in each matter as the “Commissioner”.

AMENDMENT

2 When the appeals were called on for argument on 26 November 2009 counsel for the Commissioner moved for leave to amend both notices of appeal. Notices of motion had been filed on 11 November 2009 and presumably served at about that time. They were supported by the affidavit of Marlene Binnekamp, filed on the same day. Attached to the affidavit were annexures A, B, C and D. Annexures A and B were the proposed amended notices of appeal. Annexures C and D were the parties’ submissions below. The question of leave to amend cannot be addressed without reference to the facts of the case.

INPUT TAX CREDITS AND INPUT TAXED SUPPLIES

3 A taxpayer will incur a liability to pay goods and services tax (“GST”) if, in carrying on an enterprise, it makes taxable supplies of goods and/or services. Most supplies for consideration are taxable supplies. The GST is calculated by reference to the amount of that consideration.

4 It is not uncommon for a taxpayer to make both taxable supplies and input taxed supplies. A taxpayer may also make GST free supplies. That category is not presently relevant. Input taxed supplies do not attract GST. Particular categories of supply are input taxed, presumably because it is more practicable that they be dealt with in that way. One such category is financial supply.

5 The amount of the GST payable by a taxpayer in connection with its own taxable supplies may be reduced by setting off against such amount the amount of any input tax credits. In carrying on its enterprise, the taxpayer will incur outgoings in acquiring goods and services. Included in those outgoings will be amounts representing GST payable by the suppliers. An input tax credit arises when the taxpayer, as a supplier of goods and services, acquires goods and services for a creditable purpose. Such acquisition is a creditable acquisition. A thing is acquired for a creditable purpose if the taxpayer acquires it in carrying on its enterprise, save to the extent that the acquisition relates to making supplies which will be input-taxed, or if it is of a private or domestic nature.

6 To the extent that an acquisition relates to input taxed supplies, no input tax credit is allowable. This is because input taxed supplies do not attract GST. The purpose of the input tax credit system is to avoid levying GST upon GST previously collected in the chain of supply. As input taxed supplies do not attract GST, it is not appropriate that there be input tax credits in connection with acquisitions attributable to such supplies. It is therefore necessary that the taxpayer apportion its input tax credits as between input taxed supplies and other supplies.

7 Sections 11-25 and 11-30 make provision for such apportionment. Section 11-30 prescribes a method of apportionment based substantially upon quantifying the extent of the creditable purpose as a percentage of the total purpose of acquisition and apportioning the input tax credits on a pro rata basis. However the apportionment process may be difficult. In order to facilitate that process, s 11-30(5) provides:

The Commissioner may determine, in writing, one or more ways in which to work out, for the purpose of subsection (3), the extent to which a creditable acquisition is for a creditable purpose.

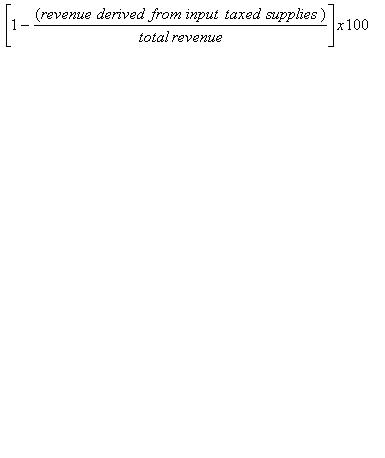

8 In the present case American Express proposed, and the Commissioner agreed that such apportionment should be calculated using the formula:

9 This calculation yields a percentage which is then used in apportioning the cost of creditable acquisitions as between input taxed and other supplies. The matter in dispute between American Express and the Commissioner is whether certain amounts received by American Express should be treated as revenue derived from input-taxed supplies for the purposes of the formula.

THE CASE

10 As is well known American Express issues cards for use by cardholders in acquiring goods and services without contemporaneous payment to suppliers. The two relevant card products are described as “credit cards” and “charge cards”. Under the terms upon which American Express provides such cards to cardholders, they must pay amounts charged to the cards within a fixed time, although the credit card also has a facility for further deferred payment of part of the amount due. That aspect is not presently relevant. The charge card conditions provide for payment of an identified amount as “liquidated damages” if payments to American Express are not made on time. The credit card conditions provide for a “late payment fee”. I will refer to both categories of payment as “Fee Payments”. Although it may previously have taken a different view, for the years from 1 July 2002 until 30 June 2004, American Express completed its Business Activity Statements upon the basis that Fee Payments were not to be included in the numerator of the formula. The Commissioner rejected this approach, re-assessed American Express’s GST liability and imposed penalties. American Express objected, but on 8 June 2006, the objections were disallowed.

11 In the Commissioner’s reasons for such disallowance, he asserted that the “supply of a charge card” was an input taxed supply, and that the Fee Payments were consideration for that supply. He made a similar assertion concerning late payment fees by credit card holders. The supply of both types of card and associated entitlements was said to comprise the supply of an interest under a debt, credit arrangement or right to credit, being one definition of the term “financial supply”, which is one category of input taxed supply. The Commissioner took the same approach in its appeal statement at first instance. Thus a significant issue below was whether the Fee Payments were consideration for the supply of the charge and credit cards and associated services. At first instance the Commissioner did not seek to justify his decision on the basis that revenue from input taxed supplies should be included in the numerator of the formula, even if that revenue was not received as consideration for such supplies. In other words, the case was conducted upon the basis that the word “revenue” in the formula meant “consideration”. The Commissioner asserted that the Fee Payments were consideration for financial supplies which were input taxed. American Express asserted that they were, in effect, damages for breach of contract, and not consideration. The primary Judge found that the Fee Payments were not consideration. The case which the Commissioner now wishes to advance is that the words “revenue derived from input taxed supplies” describe any moneys received from “the financial supply made by [American Express] to the cardholder under the charge or credit card arrangement”.

12 Although the formula was for use in apportioning the purpose for which American Express acquired goods and services, it did so by looking to the extent to which its supplies to others were input taxed. The word “revenue” has no particular meaning in the GST Act, at least for present purposes. The expression “input taxed supplies” is a statutory term. The word “consideration” is also defined in the GST Act. The definition is very broad. See s 9-15.

13 One must keep in mind the fact that the formula is not, itself, a statutory concept. As the formula addresses the extent of input taxed supplies, it will be convenient if I commence by seeking to determine whether American Express makes input taxed supplies pursuant to the arrangements concerning the charge card and credit card facilities. However, in the latter case, I will not consider that part of the credit card facility which permits further deferment of payment past the original due date. In what follows I use the term “American Express facility” as if it described a clearly identified entity. The term describes the services offered to cardholders of each type, but excluding the service provided to credit cardholders which permits the deferment of some payments to American Express past the original due date for payment. Implicit in the notion of a “facility” is the underpinning administrative arrangements which, as I infer, must exist. I also infer that they are quite complex.

FINANCIAL SUPPLIES

14 Section 40-5 identifies classes of supply which are input taxed. One such supply is a “financial supply”. That term has the meaning given by the regulations. The regulations are the A New Tax System (Goods and Services Tax) Regulations 1999 (Cth) (the “GST Regulations”). Central to the definition of “financial supply” is reg 40-5.02 which defines the term “interest” as “anything that is recognized at law or in equity as property in any form”. It is important to note that an “interest” is not an interest in legal or equitable property. Rather, an “interest” is legal or equitable property. Regulation 40-5.08 provides that for the purposes of s 40-5(2) of the GST Act a supply is a financial supply if it is a financial supply as defined in reg 40-5.09 or an incidental financial supply as defined in reg 40-5.10. Regulation 40-5.09 provides that:

(1) The provision, acquisition or disposal of an interest mentioned in sub-regulation (3) or (4) is a financial supply if:

(a) the provision acquisition or disposal is:

(i) for consideration; and

(ii) in the course or furtherance of an enterprise; and

(iii) connected with Australia; and

(b) the supplier is:

(i) registered or required to be registered; and

(ii) a financial supply provider in relation to supply of the interest.

(2) …

(3) For sub-regulation (1) the interest is an interest in or under the matter mentioned in an item in the following table … .

15 Item 2 in the table is “an interest in or under … (a) debt, credit arrangement or right to credit, including a letter of credit” (“Item 2 of the Table”).

16 Regulation 40-5.10 provides with respect to incidental financial supplies:

Despite regulation 40-5.12, if something is supplied by an entity to a recipient directly in connection with a financial supply to the recipient by the entity, the thing is an incidental financial supply if:

(a) it is incidental to the financial supply; and

(b) it and the financial supply are supplied, at or about the same time, but not for separate consideration; and

(c) it is the usual practice of the entity to supply the thing, or similar things, and the financial supply together in the ordinary course of the entity’s enterprise.

17 I do not understand reg 40-5.10 to be presently relevant.

18 A financial supply is, therefore:

the provision, acquisition or disposal of;

anything recognized at law or in equity as property in any form;

if such provision, acquisition or disposal is for consideration;

in the course or furtherance of an enterprise;

connected with Australia;

the supplier is registered or required to be registered as a financial supply provider; and

the legal or equitable property is “in or under” a matter listed in the Table in reg 40-5.9(3).

19 In argument on appeal, the focus seemed to be upon the words “credit arrangement or right to credit” in Item 2 of the Table. However a careful reading of the primary Judge’s reasons suggests that at first instance, the relevant interest was said to be “an interest in the cardholder’s debt”, meaning the debt owed by the cardholder to American Express consequent upon the former’s use of a card. See [42]-[43]. This matter may be of some importance in the resolution of this case.

20 Regulation 40-5.11 provides:

Something mentioned in a Part of Schedule 7 that relates to a financial supply mentioned in an item in the table in regulation 40-5.09, or to an incidental financial supply, is an example of the financial supply mentioned in the item or of the incidental financial supply.

21 There are then three notes to the regulation as follows:

Note 1: The examples are not to be taken as exhaustive.

Note 2: If an example in Schedule 7 is inconsistent with the description in this Division of the financial supply to which the example relates, the description prevails.

See section 15AD of the Acts Interpretation Act 1901.

Note 3: Something that is within the scope of an item in the table in regulation 40-5.09 will be a financial supply described in that item even if it is not mentioned as an example of the item set out in the Part of Schedule 7 relating to the item.

22 Section 15AD of the Acts Interpretation Act 1901 (Cth) (the “Acts Interpretation Act”) provides:

Where an Act includes an example of the operation of a provision:

(a) the example shall not be taken to be exhaustive; and

(b) if the example is inconsistent with the provision, the provision prevails.

23 As I understand it, the parties accept that s 15AD regulates the construction of the GST Regulations. In Part 2 of Schedule 7, examples of Item 2 of the Table include “Opening, keeping, operating, maintaining and closing charge and credit card facilities” (“Item 2 of the Schedule”) and “Supply of credit cards” (“Item 3 of the Schedule”).

24 Regulation 40.5.12 excludes certain supplies from the definition of “input taxed supply”. However I will consider that provision at a later stage.

25 In my view the parties have given insufficient attention to the identification of the relevant interest in or under Item 2 of the Table, the supply of which may be a financial supply. Associated with that problem is a failure to give sufficient attention to the requirement that an interest be legal or equitable property. It is not sufficient simply to assert that:

the American Express facilities might be described in terms of either Item 2 or Item 3 of the Schedule;

it is therefore a credit arrangement or right to credit; and

therefore there has been a financial supply.

The focus must be on identifying a supply of legal or equitable property.

PROPERTY

26 In the joint reasons their Honours refer to three cases concerning the meaning of the term “property”. In Jack v Smail (1905) 2 CLR 684 the High Court considered whether a grocer’s licence under licensing legislation passed to the licensee’s trustee in bankruptcy. Griffith CJ said at 705:

That being the quality of a grocer’s licence, what right can the trustees assert to it? It is not property; it is a personal right of the insolvent to carry on business in a particular place under conditions prescribed by law.

27 In Commissioner of Stamp Duties (NSW) v Yeend (1929) 43 CLR 235, the High Court considered the nature of a right to sell refreshments at a racing club. At 242, Knox CJ, Gavan Duffy, Rich and Dixon JJ drew a distinction between property and contractual rights and, at 246, Isaacs J said “(t)he distinction is clear between the personal right and the property right.”

28 These cases may not be definitive in resolving the present question. Each addresses particular statutory provisions. However there is much of relevance for present purposes in the decision of the High Court in Yanner v Eaton (1999) 201 CLR 351. In discussing property at [17]-[20], the majority (Gleeson CJ, Gaudron, Kirby and Hayne JJ) points out at [17] that the notion of property:

… is a description of a legal relationship with a thing. … Usually it is treated as a “bundle of rights”. … Considering whether, or to what extent, there can be property in knowledge or information or property in human tissue may illustrate some of the difficulties in deciding what is meant by “property” in a subject matter.

29 At [18] –[20] their Honours observe:

18. Nevertheless, as Professor Gray also says… “An extensive frame of reference is created by the notion that “property” consists primarily in control over access. Much of our false thinking about property stems from the residual perception that “property” is itself a thing or resource rather than a legally endorsed concentration of power over things and resources.

19. “Property” is a term that can be, and is, applied to many different kinds of relationship with a subject matter. …

20. Because “property” is a comprehensive term it can be used to describe all or any of very many different kinds of relationships between a person and a subject matter. … The statement that A has property in B will usually provoke further questions of classification. Is the interest real or personal? Is the item tangible or intangible? Is the interest legal or equitable?

30 Yanner is not in any sense inconsistent with the two earlier cases. It does not suggest that the distinction between property rights and personal rights has been abandoned. Clearly, the notion of property contains three elements:

The subject matter;

The property holder; and

The relationship between them.

31 For present purposes an interest must be legal or equitable property. It is therefore necessary to distinguish between legal or equitable property on the one hand and personal contractual rights on the other. The relationship between American Express and a cardholder no doubt involves substantial contractual rights, but contractual rights are not necessarily property.

32 In Meagher, Gummow and Lehane’s Equity, Doctrines and Remedies (4th ed) the learned authors observe at para 4-015:

Accordingly, and as a starting point, any system of proprietary interests may usefully be valued by reference to at least four criteria. These are: (a) the power to recover the property, the subject of the interest or the income thereof (that is, a “property right”) compared with the recovery of compensation from the defendant payable from no specific fund; (b) the power to transfer the benefit of the interest to another; (c) the persistence of remedies in respect of the interest against third parties who thus assume the burden thereof; and (d) the extent to which the interest may be displaced in favour of competing dealings by the grantor or others with interests in the subject matter (that is, priorities).

These characteristics are present in varying degrees in the hierarchy of equitable estates and interests and are to be considered when dealing with and evaluating the subject matter of this chapter. It is incorrect to assume that unless all these characteristics are present there cannot be “property”, … .

33 At para 4-140, the learned authors discuss a somewhat different approach taken by Lord Wilberforce in National Provincial Bank Ltd v Ainsworth [1965] AC 1175 where, at 1247-8, his Lordship observed

Before a right or an interest can be admitted into the category of property, or of a right affecting property, it must be definable, identifiable by third parties, capable in its nature of assumption by third parties, and have some degree of permanence or stability.

34 This approach was apparently approved in The Queen v Toohey; ex parte Meneling Station Pty Ltd (1982) 158 CLR 327, per Mason J at 342, Gibbs CJ and Brennan J concurring. In particular Mason J concluded that:

… the rights of the holder of a grazing licence created under the Crown Lands Act fall short in two respects of the concept of property or proprietary rights expressed by Lord Wilberforce. Regulation 71 (the Minister’s power to forfeit a grazing licence where the licensee fails to comply with a condition of the licence after having been given notice to do so) and reg. 71B (the right of a licensee to surrender his licence) are not inconsistent with the notion that a grazing licensee holds an interest in land. But reg. 71A represents a substantial obstacle to the applicants’ case. That regulation enables the Minister to cancel a licence, the only precondition being that he give three months’ notice in writing of his intention to do so. No default on the part of the licensee is necessary. The regulation suggests that the licensee has no interest in the land at all. The future of his right to graze stock is, by virtue of the Minister’s power to cancel, absolutely in the hands of the Minister and beyond his own control. A right terminable in the manner permitted by reg. 71A lacks that degree of permanence of which his Lordship spoke.

Assignability is not in all circumstances an essential characteristic of a right of property. By statute some forms of property are expressed to be inalienable. Nonetheless, it is generally correct to say, as Lord Wilberforce said, that a proprietary right must be “capable in its nature of assumption by third parties” …. .

35 Mason J also observed at 344 that even if the licence had conferred a right to exclusive possession of the relevant land, it would not have taken the applicants “very far” in establishing the existence of a proprietary right. Wilson J, with whom Murphy J agreed, also concluded that the licence did not confer an interest in land.

36 A somewhat different approach emerges from the decision of the High Court in Federal Commissioner of Taxation v Orica Ltd (1998) 194 CLR 500. In that case, the Court was concerned with the meaning of the term “asset” in the context of capital gains tax. The term was defined to mean “any form of property and includes … a chose in action … and any other form of incorporeal property”. Brennan CJ observed at [38] that if the definition stood alone, it would be necessary to distinguish between choses in action which were proprietary and those which were personal. At [90]-[91] the majority (Gaudron, McHugh, Kirby and Hayne JJ) concluded that the various interests in question (which were largely contractual) were assets. Their Honours pointed out that “alienability is not an indispensable attribute of a right of property according to the general sense which the word ‘property’ bears in the law”, affirming that statement by Kitto J in National Trustees Executors and Agency Co of Australasia Ltd v Federal Commissioner of Taxation (1954) 91 CLR 540 at 583. At [108]-[110], Gummow J also concluded that the choses in action were assets as defined. His Honour referred to the decision of Mason J in Toohey, suggesting that it should be read with the views of Kitto J in Trustees Executors and Agency Co. At [181]-[187] Callinan J concluded that the choses in action were assets, but also discussed the differences between personal and proprietary rights.

37 I do not understand the High Court to have abolished the distinction between proprietary and personal rights. I rather understand Orica to establish that where the term “asset” is defined to mean property including choses in action (which might be property or personal rights), the term “property” should be given a wider meaning. The decision in Yanner is inconsistent with abolition of the distinction.

38 Before considering the rights and obligations comprising the relationship between American Express and its cardholders, I should say something further about the reference in Yanner to control over access to resources as a general description of property rights. The choice of the word “resources” describes a wide range of “things” over which property rights may exist. The words “control over access” mean much more than “access”. Mere access to a resource is not sufficient. It is the degree of control over access by others which is relevant.

PROPERTY IN OR UNDER A DEBT, CREDIT ARRANGEMENT OR RIGHT TO CREDIT

39 The terms upon which American Express issues cards are identified in the joint reasons and in the primary Judge’s reasons. American Express provides the cardholder with a card. The cardholder is thereafter, in effect, able to pledge American Express’s credit with suppliers. The suppliers look to American Express for payment, and American Express requires cardholders to pay to it the amounts incurred for purchases, such payments to be made at fixed times. These rights and obligations seem generally to be personal rather than proprietary. Certainly, nothing supplied to the cardholder is capable of being assigned, and the relevant arrangements are determinable at will. The American Express facilities are no doubt quite complex. To the extent that they are capable of being “owned”, the owner is, presumably, American Express. A cardholder acquires no interest in them, but rather a contractual right to utilize their services. As I have said, the right is determinable by American Express at will and cannot be assigned. Such circumstances led the High Court in Toohey to conclude that the grazing licence did not comprise property. Whilst a cardholder has access to the facility, he or she does not control access to it.

40 A cardholder acquires possession, but not ownership of a card. No doubt the cardholder is a bailee. A bailee is said to have “special property” in the property bailed. Academic writers have asserted that a bailee’s rights are of a proprietary nature. See George W Paton’s Bailment in the Common Law (1952, Stevens & Sons Ltd, London) at 30. However, at 17-18, the author notes the decision in The Odesssa [1916] 1 AC 145 at 158-9, where Lord Mersey, in giving the advice of the Judicial Committee of the Privy Council, said:

But when the nature of the right of a pledgee to sell is examined it will be seen that the so-called “special” property which it is said to create is in truth no property at all. This has been recognized by many Judges who have used the expression “special interest” as a substitute for “special property” … .

41 Paton says at 17:

Special property seems to mean a possessary right available against even the true owner in certain conditions, e.g., where there is an artificer’s lien. Accurately, this is a mere right of possession not of property.

42 The author of Palmer on Bailment (3rd ed), at 1-106, asserts that:

A bailment gives rise to a form of property because it creates a division of interest in rem within the compass of a single chattel. The division is chronological rather than geographical; as in the case of leaseholds, a bailment divides the ownership of the res “on a plane of time”. The bailee obtains a legal interest in the form of possession, which is in many respects equivalent to an estate in land, and in the case of some bailments at least (such as pawns, liens and probably contracts of hire) this interest is preserved although the bailor disposes of his interest during the bailment to a third party. The bailor retains a reversionary interest in the form of his residual or eventual right to possession, which normally (but not necessarily) exists concurrently with his ownership of the goods; and here, again, this interest is generally preserved although the bailee disposes of the goods to a third party. In the terminology of the older authorities the bailor has the “general” and the bailee the “special” property in the subject chattel.

43 At 22-004 the author discusses special property again, this time in the context of pledges. He refers to the decision in The Odessa, suggesting that Lord Mersey was “inclined to disparage the significance of this interest, hinting that it was merely an inflated synonym for … ‘no property at all’.” The author refers in a footnote to the decision of the High Court in Palgo Holdings Pty Ltd v Gowans (2005) 221 CLR 249 at [17]. There McHugh, Gummow, Hayne and Heydon JJ said:

Commentators and the courts have long recognized that pawn or pledge is “a bailment of personal property, as a security for some debt or engagement”. They have identified such a transaction as distinct and different from mortgage where “the whole legal title passes conditionally to the mortgagee”. This distinction was sometimes expressed in terms of the difference between the “special property” of the pledgee and the “general property” which remained in the pledgor. The “special property” of the pledgee was described as the right to detain the goods for the pledgee’s security and “is in truth no property at all”. That “special property” depends upon delivery of possession, whereas in the case of a mortgage of personal property the right of property passes by the conveyance and possession is not essential to create or support the title.

44 In effect, the High Court adopted the view expressed in The Odessa that the special property of a bailee is “no property at all”. Although both The Odessa and Palgo concerned pledges, the notion of “special property” applies to all bailments as appears in the above extract from Palmer. Despite the views expressed in Paton and Palmer, it seems that in Australia, the special property of a bailee is not property. I should, however, refer to the decision in Xu v Council of the Law Society of New South Wales (2009) 236 FLR 480, a decision of the Court of Appeal of New South Wales. That case concerned the right of a solicitor to assert a lien over a client’s passport. At 490 Handley AJA, with whom Tobias JA agreed, appears to have treated a passport holder as having property in a passport, largely upon the basis that as a bailee, he or she has special property in it. However the Court seems not to have been referred to the decisions in The Odessa and Palgo. As with other aspects of the relationship between American Express and its cardholders, the card is, as I understand it, not transferable, and the right to possession may be revoked by American Express at will. All of this suggests that however one regards the arrangements in place between American Express and its cardholders, no proprietary rights are conferred in connection with possession of the cards.

45 If the rights of a bailee are property for the purposes of reg 40-5.02, then they might well be described as being in or under either of the American Express facilities. However one suspects that the supply of such “property” would not attract a significant proportion of American Express’s input tax credits. It seems likely that the cost of providing a card as a bare chattel would be very small.

46 As I have said, at first instance, the case was apparently disposed of upon the basis that the relevant interest was American Express’s interest in or under debts owed to it by cardholders. A debt may be described as property. See McCaughey v Commissioner of Stamp Duties (1945) 46 SR (NSW) 192 per Jordan CJ at 201; Mutual Pools & Staff Pty Ltd v The Commonwealth (1994) 179 CLR 155 per Brennan J at 176; and Orica, per Brennan CJ at 522. The tem “provision” of an interest includes “creation” of an interest (reg 40-5.03), and reg 40-5.06(2) provides that the acquirer of an interest is also a financial supply provider. It may be that American Express acquires an interest in or under a debt, created by either the cardholder’s use of the card or American Express’s payment to the supplier. Of course, such a debt is only payable upon the date fixed pursuant to the relevant conditions. I am inclined to the view that American Express’s acquisition of such a debt may be a financial supply, but the case on appeal seems not to have been conducted on that basis. See, for example, para 15 of the applicant’s further submissions dated 10 December 2009.

47 If there is no provision, acquisition or disposal of an interest (ie legal or equitable property) in or under any item in the Table in reg 40-5.09, then there can be no financial supply pursuant to that regulation. However the Commissioner submits that such an approach deprives Item 2 of the Table of any function and has a similar effect upon Items 2 and 3 of the Schedule. In my view s 15AD of the Acts Interpretation Act excludes the use of Sch 7 to expand the operation of Div 40. The section contemplates the possibility of a conflict between a substantive provision and examples of its operation. It directs that the substantive provision should prevail. The Commissioner seems to submit as follows:

Items 2 and 3 in the schedule are examples of a credit arrangement or right to credit for the purposes of reg 40-5.09;

the American Express charge and credit card facilities are capable of being described in the terms used in those items;

therefore the American Express charge and credit card systems are credit card arrangements or rights to credit; and

therefore, they are financial supplies.

48 This approach overlooks two aspects, namely:

the operation of s 15AD of the Acts Interpretation Act; and

the requirement that a financial supply be of an interest, ie legal or equitable property in or under a debt, credit arrangement or right to credit.

49 In looking to the examples for guidance as to whether there is a financial supply, the Commissioner fails to observe the requirement contained in s 15AD of the Acts Interpretation Act. That section requires that primacy be given to Div 40. Further, regs 40-5.02 and 40-5.09 require that there be a provision, acquisition or disposal of legal or equitable property. The American Express facility, however it may be named, does not satisfy that requirement. It is no answer to say that such an approach renders the examples otiose. That is the effect of s 15AD. In any event, there may be other credit card systems which involve the supply of interests in property. It seems that the regulation-maker contemplated such an arrangement. The proper question is whether the American Express facility falls within Item 2 in the Table. The question is not whether it is capable of being described in terms of Items 1 and 2 of the Schedule.

50 The Commissioner seems also to submit that the Table in reg 40-5.09, or at least Item 2 of the Table, will also be deprived of any function by the exclusion of the American Express facilities from its operation. I reject that submission. First, as I have said, I do not assume that arrangements which satisfy Items 2 and 3 in the Schedule will never give rise to the provision, acquisition or disposal of a relevant interest. However, save for the possible argument concerning a debt, the American Express facilities do not do so. Further, Items 2 and 3 of the Schedule do not exhaustively define Item 2 of the Table. There may well be other credit arrangements or rights to credit that involve such provision, acquisition or disposal. There is also the approach based on the acquisition of debts. As to the other items in the Table, it is not possible to consider, in a hypothetical way, the operation of Div 40 upon such classes of transaction.

51 As I have said, the primary Judge proceeded upon the basis that the relevant interests were American Express’s interests in debts owed to it by cardholders. I am unsure as to whether the Commissioner has on appeal, relied upon that approach. In view of my conclusions concerning the operation of reg 40-5.12, it is not necessary that I address questions arising out of such approach.

CREDIT

52 It is also unnecessary that I consider the way in which the primary Judge construed the term “credit”. However I am inclined to the view that his Honour’s approach was too narrow, primarily for the reasons given in the joint reasons. A cardholder is effectively authorized to pledge American Express’s “credit”. He or she is also effectively given “credit” by American Express at the time of each purchase. The cards in question are routinely described generically as “credit cards”. American Express, itself, uses that term to describe at least one of its products. The usage has become wide-spread. It is too late to adopt the limited meaning identified by the primary Judge.

CONSIDERATION

53 I should also say something about American Express’s submission that the Fee Payments were not consideration for financial supplies. The cardholder promised to pay American Express various amounts pursuant to the relevant conditions. Those promises must have been part of the consideration for the promises made by American Express, in effect, to allow each cardholder to participate as such. I consider that, to the extent that any relevant interest was supplied, the promise to pay liquidated damages or late payment fees was consideration for such supply. For present purposes there seems little justification for treating a promise to pay as consideration, but the actual payment as not being consideration.

A PAYMENT SYSTEM

54 Regulation 40-5.12 provides that the supply of an interest in or under a payment system is not a financial supply. I turn to the question of whether the American Express facilities are payment systems. The expression “payment system” is defined in the dictionary included in the GST Regulations as:

… a funds transfer system that facilitates the circulation of money, including any procedures that relate to the system.

55 The term “money” has the meaning attributed to it in Pt 6-3 of the Act as follows:

(a) currency (whether of Australia or of any other country); and

(b) promissory notes and bills of exchange; and

(c) any negotiable instrument used or circulated, or intended for use or circulation, as currency (whether of Australia or of any other country); and

(d) postal notes and money orders; and

(e) whatever is supplied as payment by way of:

(i) credit card or debit card; or

(ii) crediting or debiting an account; or

(iii) creation or transfer of a debt.

However it does not include:

(f) a collector’s piece; or

(g) an investment article; or

(h) an item of numismatic interest; or

(i) currency the market value of which exceeds its stated value as legal tender in the country of issue.

56 Regulation 40-5.13 provides that Sch 8 contains “examples” of supplies mentioned in the table in reg 40-5.12, but again with a note concerning the operation of s 15AD of the Acts Interpretation Act. Part 2 of Sch 8 provides examples of Item 4 (a payment system) in the Table in reg 40-5.12. Part 2 of Sch 8 is as follows:

Item | Example |

1 | Supply of services by a payment system operator to a participant in the system for which the following fees are charged by the operator: (a) membership fees; (b) processing frees; (c) service fees; (d) marketing fees; (e) risk management fees; (f) multi-currency fees |

2 | Access to a payment system, and supply of other related services by a participant in the system to a third party |

3 | Supply of a service by one participant in a payment system to another participant in the system in relation to charge, credit and debit card transactions

|

4 | Processing, settling, clearing and switching transactions of the following kinds: (a) direct credit and debit; (b) other debit and credit transactions; (c) charge, credit and debit card transactions; (d) cheque; (e) electronic funds transfer; (f) ATM; (g) B-pay; (h) Internet banking; (i) GiroPost; (j) SWIFT (Society for Worldwide Interbank Financial Telecommunciations) Payment Delivery System; (k) an approved RTGS (real time gross settlement) system; (i) Austraclear |

5 | Supply to a participant in a payment system by the operator of the system of the following services: (a) processing of account data; (b) electronic payment services |

57 The Commissioner submits that American Express did not, in its “pleadings” at first instance, raise any argument based on reg 14-5.12. It may be that the argument was not raised in American Express’s appeal statement, but it was dealt with by both sides in their submissions. The primary Judge decided the matter. It is too late for the Commissioner to complain that it was not raised at an earlier stage. It is true that there is little detail of American Express’s internal operations, but the matter was dealt with on the evidence as it was. The fundamental nature of the American Express facilities was explained in the evidence. At first instance American Express bore the onus of proving that the assessments were wrong, but on appeal, it is for the Commissioner to demonstrate that the primary Judge was wrong. He has not pointed to any fatal gaps in the evidence upon which his Honour’s conclusions were based.

58 It is, I think, sufficient to identify the alleged payment systems as being the two American Express facilities, including all dealings between cardholders, suppliers and American Express, as explained in the evidence, including the American Express documentation. His Honour dealt with this matter primarily by adopting the decision of Tamberlin J in Visa International Service Association & Anor v Reserve Bank of Australia (2003) 131 FCR 300. That case concerned applications to review decisions of the Reserve Bank of Australia (the “Reserve Bank”) to designate the Visa and Mastercard card systems pursuant to the Payment Systems (Regulation) Act 1998 (Cth) and the Payment Systems and Netting Act 1998 (Cth), (collectively, the “Payment Systems legislation”) and so subject them to regulation. These systems involved the use of cards in much the same way as do the American Express facilities. However the supplier (or “merchant”) submitted the relevant vouchers to its own bank, which bank eventually presented them to the cardholder’s bank. The last-mentioned bank was the issuer of the relevant card. This presentation was done using the Reserve Bank’s clearing system. The Visa and Mastercard service operators provided various “liaison” functions as between participating banks, and between them and the Reserve Bank. Thus there were four parties to each relevant transaction apart from the Visa or Mastercard operator and the Reserve Bank. Those parties were the supplier, the supplier’s bank, the cardholder and the cardholder’s bank. The systems appear in diagramatic form at [94] and [105]. The banks are there described as the “issuer” and the “acquirer”.

59 The difference between the Visa and Mastercard systems and the American Express system is that American Express performs all of the functions performed by the banks, the Visa and Mastercard operators and the Reserve Bank. The American Express system appears to be simpler than the Visa and Mastercard systems, at least partly because many of the functions identified in the diagrams at [94] and [105] in the Visa case are performed by American Express. Evidence of those internal procedures is not relevant for present purposes. Of course banks are generally involved in the American Express system to the extent that both cardholders and suppliers will usually operate bank accounts from which cardholders pay amounts due to American Express, and into which suppliers deposit payments received from American Express. Those matters are not presently relevant. I agree with the primary Judge that there appears to be no relevant difference between the Visa and Mastercard systems and the American Express system.

60 A question arising in the Visa case was whether the Visa and Mastercard arrangements were payment systems under the relevant legislation. Tamberlin J concluded that they were. The definition of “payment system” in the Payment Systems legislation was similar to that in the GST Regulations. I agree with the Commissioner that the decision in the Visa case does not necessarily determine the present case. However a different outcome is unlikely. The only difference identified by the Commissioner is the number of parties. As I have said, that seems to make no material difference. The Commissioner also submits that the decision in the Visa case concerned only the relationship involving the supplier (or merchant), the merchant’s bank and the issuing bank. That proposition reflects a misreading of the reasons. Visa and Mastercard had asserted that any payment system operated only at the level at which the Reserve Bank was involved in clearing transactions. Tamberlin J rejected that view. At [265] his Honour accepted that at the level of merchant and cardholder, there was no transfer of money. However he concluded that:

While there is some force in the proposition that some particular steps taken in isolation do not effect a transfer of money, when considered cumulatively from the authorisation step to final settlement at the RBA level, each of the schemes as designated amounts to a payment system within the definition.

61 Whilst the extent of the schemes “as designated” is not entirely clear, it presumably included the contents of the diagrams at [94] and [105]. Further, at [299], his Honour concluded that there was a relationship between the various parts of the systems in the diagrams, commencing with the presentation of the card and acceptance by the supplier (or merchant) after authorization. Obviously, only the cardholder could present the card. Finally, Tamberlin J concluded at [305]:

For these reasons I am persuaded that the instruments (credit cards, records and forms) and procedures at the issuer [bank], acquirer [bank] or merchant levels are within the definition “payment system” as a matter of interpretation.

62 Although his Honour did not, at this point, refer to the cardholders, he referred to the cards which, again, could only be used by the cardholders.

63 In any event, the question is not whether the American Express facilities are payment systems for the purposes of the Payment Systems legislation. The question is whether or not they are payment systems for the purposes of the GST Regulations. In other words, were the American Express facilities, as explained in the primary Judge’s reasons and in the evidence, funds transfer systems which facilitated the circulation of money, keeping in mind the very broad definition of “money” in the GST Act? The relevant item in that definition is:

(e) whatever is supplied as payment by way of:

(i) credit card or debit card; or

(ii) crediting or debiting an account; or

(iii) creation or a transfer of the debt.

64 Clearly, the distinction between a credit card and a charge card is not relevant for present purposes. One may safely assume that the expression “credit card or debit card” includes both the credit cards and charge cards with which this case is concerned. The definition of “money” as including whatever is supplied as payment by way of credit card or charge card strongly suggests that rights and obligations created and discharged when payment is made using such cards concern the circulation of money in the wider sense used in the definition. All consequential transactions would facilitate such circulation. Further, such transactions would involve the crediting or debiting of accounts.

65 A funds transfer system, I infer, is any system by which funds are transferred from one party to another. The American Express facilities involve the payment of moneys by American Express to merchants and the receipt by American Express of moneys paid by cardholders. No doubt American Express has its own substantial capital reserves with which it facilitates such transfers. The American Express facilities are funds transfer systems, involving American Express, the suppliers (or merchants) and the cardholders. Clearly, they facilitate the circulation of money as that term is defined.

66 I should add that a consideration in deciding whether a particular funds transfer system facilitates the circulation of money, might be the volume of funds transferred through it as compared to the amount of money in circulation. However neither party addressed this issue.

QUESTIONS FOR DETERMINATION

67 The Court is presently concerned to determine whether the Fee Payments were within the expression “revenue derived from input taxed supplies” in the formula. The first question is whether the Commissioner should be allowed to amend his notice of appeal in order to depart from the previously shared assertion that “revenue” in this context means “consideration”. As I have said, the Commissioner has not really explained why he has, until such a late stage, been willing to adopt that view of the formula, nor why he should now be allowed to depart from it. He asserts that American Express could not have rebutted such a case at first instance in any way which is not now open to it.

68 I again point out that the Commissioner’s reason for disallowing American Express’s objections to the assessments was that the relevant Fee Payments were by way of consideration for financial supplies. Thus, at p 13 of the reasons for each objection decision, the Commissioner said, concerning the charge card:

We consider that whichever way the amount paid as liquidated damages is described it will not alter its character as consideration for the supply of an interest in a debt, credit arrangement or right to credit. Even if the amount were to be viewed as a penalty and non-enforceable as against the cardmember, it would still be consideration. In this regard, the GST Act does not require that a supply must be lawful for it to be a supply for [the] purposes of section 9-10(3). Nor does it require that the consideration be enforceable for [the] purposes of section 9-15(2).

69 As to credit cards, the Commissioner said at p 14:

We consider that whichever way the fee is described and/or calculated and irrespective of the nature of the costs it is designed to cover, it is clearly charged in connection with the supply of an interest in a credit card and is further consideration for that supply. The supply of that interest is a supply of an interest in or under a debit, credit arrangement or right to credit under item 2 in regulation 40-5.09 in the GST Regulations which is an input taxed supply under section 40-5 of the GST Act.

70 At first instance American Express attacked these decisions, asserting that the Fee Payments were not received as consideration for financial supplies. The Commissioner did not mount an alternative argument that, in any event, the Fee Payments were revenue. The obligation imposed upon American Express by the GST Act was to pay the amount owing by way of GST, after deduction of the relevant input tax credits: see s 7-5. If the proportion of the input tax credits attributable to input taxed supplies was not to be calculated using the formula actually prescribed in s 11-30, then it had to be calculated upon a basis which either complied effectively with that section or was accepted by both the Commissioner and American Express as doing so. For so long as there was agreement as to a particular formula for calculation, no question arose as to whether that formula was appropriate for use in connection with the calculations prescribed by s 11-30.

71 The Commissioner continued to assert that the Fee Payments were consideration for the supply of financial services until 11 November 2009, shortly before the hearing of this appeal. Had the Commissioner, at or prior to the hearing below, sought to depart from that basis of calculation, it would have been necessary to consider whether he was entitled to do so and, if so, whether American Express was bound by the formula as construed by the Commissioner. The Commissioner and American Express were bound by the GST Act. It seems unlikely that the parties could have resolved any impasse by reference to the law of contract. Any “way” determined to be appropriate by the Commissioner would be a permissible method of calculation, but both the Commissioner and American Express were bound to comply with s 11-30 as a whole. The Commissioner was free to decide that a “way” was no longer appropriate. American Express was entitled to argue that any “way” approved by the Commissioner was not consistent with the GST Act.

72 American Express has given some indication of how it might have gone about challenging any decision by the Commissioner to calculate the input tax credits using his more recent view as to the meaning of the formula. It says in its further submissions dated 3 December 2009:

53 If the Commissioner had sought to take a different approach at trial by including amounts that fall within the broader expression “revenue” in the numerator of the formula referred to at paragraph [27] of the judgment of the learned primary judge, [American Express] would, in addition to the contentions advanced on the application, have sought to rely on alternative methodologies to calculate its extent of creditable purpose (“ECP”) on the basis that broadening the meaning of revenue so as to include the liquidated damages and late payment fees in the numerator would not produce a fair and reasonable calculation of ECP.

54 The first alternative methodology from which [American Express] would or is likely to have led the evidence on would be based on a model that:

(a) first allocates costs between the credit card portfolio and the charge card portfolio; and

(b) further allocates costs in respect of the credit card portfolio between transactors (ie cardholders who pay their bills in full every month) and revolvers (ie cardholders who only pay the minimum amount due on their bills every month), both of which are described in the affidavit of Mr Rayner.

55 The second alternative methodology which [American Express] would or is likely to have advanced would involve an input-based model that allocates, where possible, input tax credits to activities. That is, instead of determining an ECP by reference to revenues, the methodology would calculate [American Express’s] ECP by reference to the various taxable, “out of scope” and input taxed activities undertaken by [American Express] in carrying on its enterprise.

56 To the extent that input tax credits cannot be directly allocated to an activity, an ECP would then be calculated using the following formula:

57 This ECP would then be applied to the remaining unallocated input tax credits.

58 The further evidence that [American Express] would or is likely to have led in proceedings in support of the alternative methodologies shown above includes evidence from:

(a) an expert accountant who specializes in reviewing, preparing and developing apportionment methodologies for major financial institutions;

(b) an economist who has experience in the allocation of costs between different business activities (activity-based costing expertise);

(c) a representative of [American Express] (business modelling/finance) who would demonstrate how a greater proportion of the costs of the business relate to activities that involve the generation of income from taxable services (such as merchant services and travel-related services) as compared to activities that involve the generation of income from other areas (such as interest income); and

(d) a representative of [American Express] who would identify costs (such as rent), demonstrate how the business captures those costs (by describing systems and processes), describe how the costs are allocated to costs centres and the system of payment of invoices and expenses.

73 It may be that these assertions are relatively general. However, in comparison to the Commissioner’s explanation as to why he should be allowed to change his position at this late stage, they are substantial. I do not accept the Commissioner’s submission that American Express could not have taken steps to rebut his new approach, had this position been raised at first instance. American Express has identified courses which may have been open to it. The Commissioner has not really challenged them. He also submits that the apparent misunderstanding as to the meaning of the formula was brought about by the conduct of American Express. That is patently incorrect. As I have demonstrated, the whole basis of each of the objection decisions was that the Fee Payments constituted consideration for financial supplies. The Commissioner submits that to treat the American Express card facilities as not involving input taxed supplies would be inconsistent with the way in which American Express and he have treated supplies of card services, presumably as not attracting GST. That may be so, but if such treatment is not consistent with the GST Act and the GST Regulations, then the position should be re-considered.

ORDERS

74 In the circumstances, I would refuse leave to amend and dispose of the matter upon the basis ventilated at first instance. Given my view that any interest in or under either of the American Express facilities would be in or under a payment system, it follows that the appeals should be dismissed.

I certify that the preceding seventy-four (74) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Dowsett. |

Associate:

IN THE FEDERAL COURT OF AUSTRALIA | |

VICTORIA DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 698 of 2009 |

ON APPEAL FROM THE FEDERAL COURT OF AUSTRALIA |

BETWEEN: | COMMISSIONER OF TAXATION Appellant

| |

AND: | AMERICAN EXPRESS WHOLESALE CURRENCY SERVICES PTY LIMITED Respondent | |

IN THE FEDERAL COURT OF AUSTRALIA | ||

VICTORIA DISTRICT REGISTRY | ||

GENERAL DIVISION | NSD 699 of 2009 | |

ON APPEAL FROM THE FEDERAL COURT OF AUSTRALIA |

BETWEEN: | COMMISSIONER OF TAXATION Appellant

|

AND: | AMERICAN EXPRESS INTERNATIONAL INC Respondent

|

JUDGES: | DOWSETT, KENNY & MIDDLETON JJ |

DATE: | 17 september 2010 |

PLACE: | MELBOURNE (heard in SYDNEY) |

REASONS FOR JUDGMENT

KENNY AND MIDDLETON JJ

INTRODUCTION

75 These appeals involve the determination of an entitlement to input tax credits under the A New Tax System (Goods and Services Tax) Act 1999 (Cth) (‘the GST Act’). Specifically, the appeals concern the treatment of payments to American Express International Inc (‘Amex Intl’), by the holders of charge cards and credit cards following the cardholders’ defaults. These payments are collectively referred to below as ‘the fee payments’.

76 It is unnecessary to differentiate between the respondents with regard to the treatment of the fee payments. The respondents are related companies whose position is relevantly the same in relation to the principal question of entitlement to input tax credits. It is sufficient to note that, although Amex Intl issued the cards and received the fee payments, American Express Wholesale Currency Services Pty Ltd (‘Amex Wholesale’) was the entity liable for GST for most of the relevant time period, pursuant to s 48-5 of the GST Act. Amex Intl was also liable for GST for a period of several months commencing 1 March 2002.

77 The respondents’ position is that they are entitled to an input tax credit for a proportion of the goods and services tax (‘GST’) said to be imbedded in the creditable acquisitions that they have made. Their dispute with the Commissioner of Taxation concerns the proper calculation of the “extent of creditable purpose” under s 11-30(3) of the GST Act – that is, the calculation to be applied in determining the entitlement to input tax credits with respect to certain acquisitions.

78 In brief, under the GST Act, taxpayers are entitled to input tax credits on “creditable acquisitions”, and an acquisition can be fully creditable, partly creditable, or not creditable, depending, among other things, on the purpose for which the taxpayer makes the acquisition. In order to have an input tax credit, the taxpayer must have a “creditable purpose” as defined. Although the GST Act uses language that is most appropriate for an analysis of individual acquisitions, an individual approach would be prohibitively inefficient for some taxpayers. For this reason, the Commissioner permits some taxpayers to analyse their acquisitions in the aggregate. No-one has suggested that the GST Act does not in fact permit an aggregate approach. The respondents adopted an aggregate approach here, using a formula which employed revenue figures to approximate the extent of creditable purpose. We discuss the formula further below.

79 In what follows, it is important to keep in mind that, although the dispute centres on the proper treatment of the fee payments, the fee payments themselves are not the source of the input tax credits at issue. Rather, the credits are for various other (creditable) acquisitions that have been made. There was no evidence of the precise nature of these acquisitions and nothing turns here on their nature. This is because the formula used to calculate the extent of creditable purpose for these acquisitions did not directly depend on the nature of the acquisitions themselves but used revenue as a proxy to calculate the extent of creditable purpose.

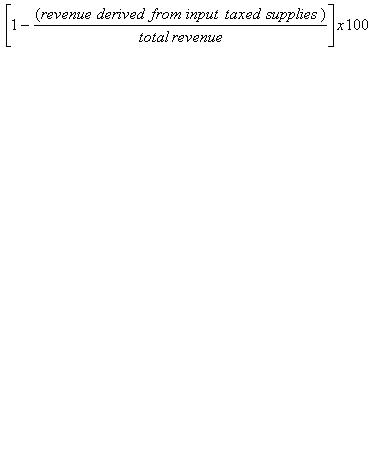

80 The parties agreed that the extent of creditable purpose, expressed as a percentage, could be calculated using the following formula (‘the formula’):

For “input taxed supplies”, see s 9-30(2) of the GST Act (discussed below).

81 At the outset, a few words must be said regarding the origin of the formula set out above. Although the formula does not mirror the language of the GST Act, the Commissioner accepted at first instance and on these appeals that the formula is in accordance with s 11-30(3) of the GST Act. The formula is an inversion of a formula approved in a ruling of the Commissioner, based in part on the efficiency concerns mentioned in paragraph [78] above: see GSTR 2000/22 at [62]. This particular ruling was later replaced by another ruling approving a formula essentially the same as the formula in the original ruling: see GSTR 2006/3 at [12], [109].

82 The central question is whether, in applying the formula, the fee payments should be considered “revenue derived from input taxed supplies” and therefore be included in the numerator of the fraction. Including fee payments in the numerator would reduce entitlement to input tax credits, which, of course, would increase the liability for GST. The Commissioner argued that the payments should be included in the numerator (as well as the denominator). The respondents argued that they should be included in the denominator but not in the numerator.

83 The case before the primary judge was conducted on the basis that, in the formula, the expression “revenue derived from input taxed supplies” was to be understood as having the same meaning as “consideration for input taxed supplies”, despite the apparent difference in meaning between “revenue” and “consideration”, upon the basis that the formula as thus understood provided a fair and reasonable method of apportionment. The only category of input taxed supply at issue was “financial supply”, a term subject to a complex definition in the GST legislation and regulations. We discuss this definition below, under the heading “Legislative Framework”.

84 Briefly stated, the primary judge concluded that the fee payments were not consideration in connection with financial supples. In the alternative, the primary judge concluded that supplies to charge card or credit cardholders were not financial supplies because they were supplies under a “payment system” which the relevant regulations exclude from the definition of financial supply. These matters are all discussed in greater detail below under the headings “Legislative Framework” and “Reasons of the Primary Judge”.

85 In the result, the primary judge upheld both of the taxation appeals, set aside the Commissioner’s objection decisions, and remitted the matters to the Commissioner. These appeals are from his Honour’s judgment in each case.

86 The Commissioner’s notices of appeal of 10 July 2009 assumed that, as both parties submitted below, the relevant issue was whether the fee payments were consideration in connection with financial supplies. Thus, the Commissioner’s grounds of appeal challenged: (1) the primary judge’s finding that Amex Intl did not make a financial supply by the provision or acquisition of an interest to or from the cardholder in or under a debt, credit arrangement or right to credit within the meaning of item 2 in the table in regulation 40-5.09(3) of the A New Tax System (Goods and Services Tax) Regulations 1999 (Cth) (‘the Regulations’); (2) the primary judge’s finding that the fee payments were not consideration in connection with the provision, acquisition or disposal by Amex Intl of an interest within the meaning of item 2 in the table in regulation 40-5.09(3) of the Regulations; (3) the primary judge’s alternative finding that the supply was not a financial supply because it was in the supply of, or an interest in or under, a payment system within the meaning of item 4 in the table in regulation 40-5.12 of the Regulations.

87 A notice of contention was also filed by Amex Wholesale to the effect that no additional tax by way of penalty was properly payable under s 284-75(1) in Schedule 1 of the Taxation Administration Act 1953 (Cth). It is unnecessary to discuss this notice of contention following the Commissioner’s concession not to seek penalties against Amex Wholesale under Division 284 of Schedule 1 to the Taxation Administration Act 1953 (Cth) in the event the relevant appeal is upheld.

88 Prior to the hearing of the appeals, however, the Commissioner applied to expand his case. On 11 November 2009, the Commissioner filed a motion for leave to amend the notices of appeal to add the following two grounds:

The Court should have found that amounts described as “liquidated damages” and the “late payment fees” received by [Amex Intl] should not be excluded in calculating, for the purposes of section 11-15(2)(a) of [the GST Act], the extent to which acquisitions by the Respondents, which would otherwise have been creditable acquisitions, were acquisitions which “related to making supplies that would be input taxed”.

The Court should have found that amounts described as “liquidated damages” and the “late payment fees” received by [Amex Intl] should be included in both the numerator and the denominator of the fraction adopted by the parties as the measure, for the purposes of section 11-15(2)(a) of [the GST Act], of the extent to which acquisitions by the Respondents, which would otherwise have been creditable acquisitions, were acquisitions which “related to making supplies that would be input taxed”.

89 The Commissioner sought to argue that the proper question was not whether the fee payments were consideration for the making of financial supplies, but simply whether they constituted revenue derived from the making of financial supplies. The Commissioner submitted that, notwithstanding that both parties had previously equated “revenue derived from input taxed supplies” with “consideration in connection with input taxed supplies”, and the primary judge had followed their lead, this interpretation of the formula was in fact erroneous. The Commissioner argued that the proposed amendment raised a purely legal issue – i.e., the proper interpretation of the formula – and no new factual evidence would be required to resolve it.

90 The respondents argued that the Commissioner’s proposed amendment raised a new factual basis for interpreting the formula. During oral submissions and in supplementary written submissions filed (with leave) after the hearing of the appeals, the respondents asserted that they would have made a different case, with different evidence, had the case below been framed in the terms of the proposed amendment. They maintained that permitting the Commissioner to reformulate the issue on appeal would unfairly prejudice them, and that leave to amend should be denied.

91 For the reasons that follow, we would grant the Commissioner’s motion to amend and allow the appeals.

FACTUAL BACKGROUND

92 The factual context relevant to the formula and the principal question can be briefly described, in the main by reference to the reasons for judgment of the primary judge.

93 Amex Intl issues charge cards and credit cards to customers who agree to be bound by the cards’ terms and conditions. (The parties agreed that the failure of the witnesses at trial to draw a distinction between related corporations led the primary judge erroneously to refer to both respondents as card issuers. The error is immaterial for the outcome below and on the appeals.) Cardholders use the cards to make purchases from merchants. Both varieties of cards function through three separate bilateral contracts: between Amex Intl and the cardholder; between Amex Intl and the merchant; and between the cardholder and the merchant.

94 The terms of the contract between Amex Intl and the cardholder are somewhat different for charge cards and credit cards. As summarized by the primary judge (see American Express International Inc v Federal Commissioner of Taxation (2009) 73 ATR 173 (‘American Express’) 177-8 at [12]), in the case of a charge card, the terms of the agreement between Amex Intl and the cardholder are:

• A card may be used at any merchant displaying the American Express card’s logo to pay for goods or services provided by the merchant: the card may also be used by mail, telephone order or through the internet.

• The cardholder pays an annual fee for the use of the card and the services provided by card issuer.

• The card holder is liable to the card issuer for all Charges on the card: a Charge is a transaction made with the card or charged to the cardholder’s account.

• The card issuer sends to the card holder once a month a statement for each period during which there is any activity or balance outstanding on the cardholder’s account and the cardholder must pay the card issuer the full amount of the closing balance shown in the monthly statement.

• If the card holder fails to pay the balance of the cardholder’s account when due, the cardholder is liable to pay [an amount described as] liquidated damages.

• No provision is made for the deferral of payment of any part of the balance of an account.

95 The primary judge summarized the difference in terms between charge cards and credit cards as follows (at 178 [15]):

The difference is that, under the Charge Card Facility, the card holder must pay in full the balance shown on the monthly statement upon receipt of the statement from the card issuer, or within a short time after receipt of the statement. However, under the Credit Card Facility, the card holder has the option of paying the amount of the minimum payment or such further amount as the card holder chooses. The card holder then becomes liable to pay to the card issuer interest on the balance of the account outstanding from time to time under and in accordance with the provisions of the Credit Card Terms and Conditions. So long as the card holder pays at least the minimum amount, there is no breach of the Credit Card Terms and Conditions.

An additional difference is that, in the case of a credit card, the amount for which a customer is liable if he or she fails to make a timely monthly payment is designated a “late payment fee” rather than “liquidated damages”.

96 The terms of the contract between Amex Intl and the merchant are similar for both kinds of cards. As summarised in the primary judge’s findings (at 177 [11]), those terms are:

• the card issuer agrees with the merchant to pay to the merchant the face amount of all purchases that cardholders make with a card, together with any amounts incidental to such purchase, such as GST, other taxes or duties, service or delivery charges and gratuities submitted by the merchant less specified amounts, such as a merchant service fee, taxes, credits an[d] amounts owing by the merchant to the card issuer;

• the card issuer will either make a direct payment to the merchant’s business bank account on the third business day after the card issuer receives a charge summary form from the merchant or will transmit payment direct to the merchant’s business bank account on the business day after the card issuer receives charges submitted electronically;

• a cardholder who acquires goods or services from the merchant will be treated by the merchant as having discharged the cardholder’s obligation to pay for those goods and services by producing the card to the merchant and signing a record of charge form evidencing the acceptance by the cardholder of the goods supplied or services provided by the merchant.

97 The terms of the contract between the merchant and the cardholder are also similar for both cards. As summarised in the primary judge’s findings (at 178 [13]), those terms are:

• the merchant agrees to supply goods or provide services to the cardholder for a price;

• the merchant agrees that the obligation to pay the price may be discharged by the production of the card and the signing of a record of charge form;

• the transaction between the merchant and the cardholder is complete at the time when the goods are supplied or the services are provided and the cardholder has no continuing liability or obligation to the merchant in respect of the price for the goods or services: see Re Charge Card Services Ltd [1989] 1 Ch 497.

LEGISLATIVE FRAMEWORK

98 In HP Mercantile Pty Ltd v Commissioner of Taxation (2005) 143 FCR 553 (‘HP Mercantile’), at 557 [13], Hill J (with whom Stone and Allsop JJ agreed) described the scheme that the GST Act supports in the following way:

The gen[i]us of a system of value added taxation, of which the GST is an example, is that while tax is generally payable at each stage of commercial dealings (supplies) with goods, services or other “things”, there is allowed to an entity which acquires those goods, services or other things as a result of taxable supply made to it, a credit for the tax borne by that entity by reference to the output tax payable as a result of the taxable supply. That credit, known as an input tax credit, will be available, generally speaking, so long as the acquirer and the supply to it (assuming it was a “taxable supply”) satisfied certain conditions, the most important of which, for present purposes, is that the acquirer make the acquisition in the course of carrying on an enterprise and thus, not as a consumer. The system of input tax credits thus ensures that while GST is a multi-stage tax, there will ordinarily be no cascading of tax. It ensures also that the tax will be payable, by each supplier in a chain, only upon the value added by the supplier.

Liability to pay GST – taxable supply

99 The GST is generally payable at each stage of a commercial “supply” of goods and services. A person must pay the GST payable on any taxable supply that the person makes: GST Act, ss 7-1(1) and 9-40. A person makes a “taxable supply” if, amongst other things, the person makes the supply for consideration and the supply is made in the course or furtherance of an enterprise that the person carries on: s 9-5. A “supply” is defined in s 9-10(1) of the GST Act as “any form of supply whatsoever”. Paragraph 9-10(2)(f) specifically provides that “supply” includes “a financial supply”.