FEDERAL COURT OF AUSTRALIA

Australian Olive Holdings Pty Ltd v Huntley Management Limited

[2010] FCAFC 76

|

Citation: |

Australian Olive Holdings Pty Ltd v Huntley Management Limited [2010] FCAFC 76 |

|

|

Appeal from: |

Australian Olive Holdings Pty Limited v Huntley Management Limited, in the matter of Huntley Management Limited [2009] FCA 1479 |

|

|

Parties: |

AUSTRALIAN OLIVE HOLDINGS PTY LTD (ACN 078 862 085) v HUNTLEY MANAGEMENT LIMITED (ACN 089 240 513) |

|

|

File number: |

NSD 1479 of 2009 |

|

|

Judges: |

JACOBSON, GILMOUR and FOSTER JJ |

|

|

Date of judgment: |

29 June 2010 |

|

|

Catchwords: |

CORPORATIONS – whether, in the circumstances of the present case, s 601FS(1) and s 601FT(1) of the Corporations Act were engaged after the responsible entity of the relevant schemes was changed – whether, upon the true construction of the constitution of the relevant managed investment schemes, the liability of the outgoing responsible entity to pay an annual base fee under the water contract was a liability for which it could have been indemnified out of the scheme property of those schemes so that, pursuant to s 601FS(2)(d) and s 601FT(2), the provisions of s 601FS(1) and s 601FT(1) do not apply to the water contract and to the incoming responsible entity in respect of the water contract |

|

|

Legislation: |

Corporations Act 2001 (Cth), Ch 5C, Pt 5C.2 (s 601FA to s 601FT) |

|

|

Cases cited: |

Australian Olive Holdings Pty Ltd v Huntley Management Ltd (2009) 76 ACSR 256 affirmed Australian Competition and Consumer Commission v Baxter Healthcare Pty Ltd (2007) 232 CLR 1 cited Re Investa Properties Ltd (2001) 187 ALR 462 followed Syncap Management (Rural) Australia Ltd v Lyford (2004) 51 ACSR 223 followed |

|

|

|

|

|

|

Date of hearing: |

3 May 2010 |

|

|

|

|

|

|

Place: |

Sydney |

|

|

|

|

|

|

Division: |

GENERAL DIVISION |

|

|

|

|

|

|

Category: |

Catchwords |

|

|

|

|

|

|

Number of paragraphs: |

146 |

|

|

|

|

|

|

Counsel for the Appellant: |

Mr JC Giles, Mr JS McLeod |

|

|

|

|

|

|

Solicitor for the Appellant: |

Harris & Harris |

|

|

|

|

|

|

Counsel for the Respondent: |

Mr SR Donaldson SC, Mr BL Jones |

|

|

|

|

|

|

Solicitor for the Respondent: |

Piper Alderman |

|

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 1479 of 2009 |

|

ON APPEAL FROM THE FEDERAL COURT OF AUSTRALIA |

|

AUSTRALIAN OLIVE HOLDINGS PTY LTD (ACN 078 862 085) Appellant

|

|

|

AND: |

HUNTLEY MANAGEMENT LIMITED (ACN 089 240 513) Respondent

|

|

JUDGES: |

JACOBSON, GILMOUR and FOSTER JJ |

|

DATE OF ORDER: |

29 June 2010 |

|

WHERE MADE: |

SYDNEY |

THE COURT ORDERS THAT:

2. The appellant pay the respondent’s costs of and incidental to the appeal.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

The text of entered orders can be located using Federal Law Search on the Court’s website.

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 1479 of 2009 |

|

ON APPEAL FROM THE FEDERAL COURT OF AUSTRALIA |

|

BETWEEN: |

AUSTRALIAN OLIVE HOLDINGS PTY LTD (ACN 078 862 085) Appellant

|

|

AND: |

HUNTLEY MANAGEMENT LIMITED (ACN 089 240 513) Respondent

|

|

JUDGES: |

JACOBSON, GILMOURand FOSTER JJ |

|

DATE: |

29 june 2010 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

THE COURT:

1 Australian Olives Projects 1 to 6 (the projects) are carried out at Yallamundi, Qld. Yallamundi is approximately 85 km south-west of Toowoomba, Qld and about 65 km north-west of Warwick, Qld.

2 Each project is separate from the others although all six of the projects are conducted in approximately the same geographical area. Each project is a separate managed investment scheme which is registered and operated pursuant to Chapter 5C of the Corporations Act 2001 (Cth) (the Act).

3 The present appeal involves the construction of a contract made in 2002 whereby the appellant (AOHL) agreed to supply to Australian Olives Ltd (AOL) and AOL agreed to take quantities of water for the purpose of irrigating several of the projects. The appeal also involves consideration of the consequences of certain decisions taken in 2008 by the investors in the projects (the members of the relevant managed investment schemes) to remove AOL as the responsible entity of those projects and to replace it with the respondent (Huntley). It was argued by AOHL that s 601FS and s 601FT of the Act permitted and required Huntley to “step into the shoes” of AOL thus rendering it liable to pay a proportion of the annual fee which AOL was contractually bound to pay to AOHL under the contract in question.

4 The first project commenced in late 1998. Projects 2, 3 and 4 began in the period between 1999 and early 2001. All of these four projects were under way before the Act came into force and had been established and operated for a time under earlier and quite different statutory provisions. Projects 5 and 6 commenced in 2003 and 2004 respectively, after the Act had commenced.

5 The present appeal concerns Projects 4, 5 and 6 only.

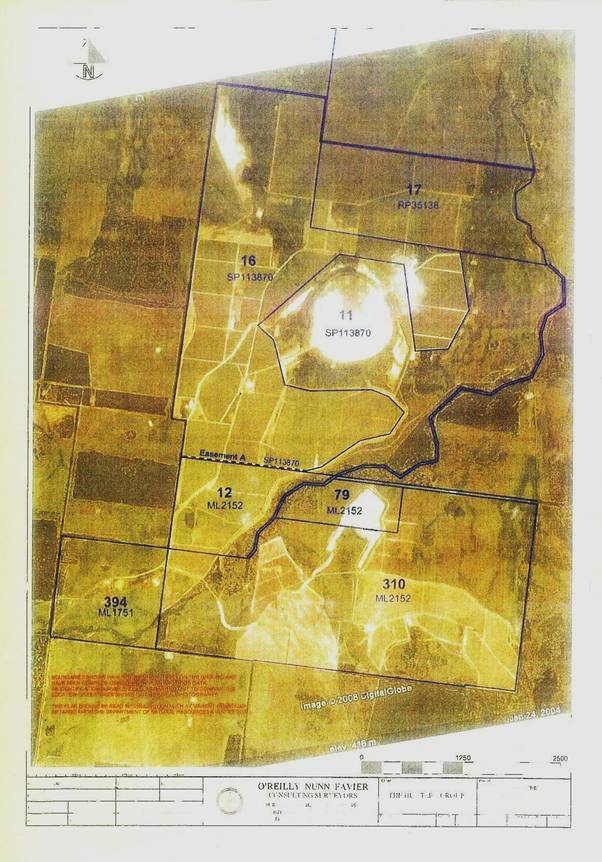

6 Attached to these Reasons for Judgment as Attachment “A” is an aerial photograph of the area where the projects are conducted. The white areas shown on that photograph are bodies of water. The north-western body of water is known as “the North-west dam”. The largest body of water just above the middle of the photograph is known as “Yallamundi Lagoon”. Yallamundi Lagoon is a freshwater lake which has the capacity to hold 7,300 megalitres of water. The body of water shown in Lot 79 in the photograph is known as “the Project 5 dam”. The creek running diagonally north-east to south-west on the photograph is Speers Creek. These bodies of water together with overland flow water are the sources of water for irrigating the projects. Natural rainfall was expected to supply a significant amount of the water required for the projects. The contribution made by natural rainfall was expected to vary from year to year.

7 Project 6 is located entirely south of Speers Creek and is irrigated solely with water from the Project 5 dam. Most of the groves comprising Project 5 are also located south of Speers Creek and are irrigated solely with water from the Project 5 dam. A small part of Project 5 is located north-west of Speers Creek. This part of Project 5 is irrigated with water from Yallamundi Lagoon.

8 Project 4 is located north of Speers Creek and is irrigated solely from Yallamundi Lagoon.

9 At all relevant times up to March 2008, AOL was the manager of all six of the projects and also the responsible entity of each of the managed investment schemes constituted by each of those projects. By March 2008, Projects 1 to 6 comprised 6,474 olive groves planted in approximately 1,060 hectares. At that time, there were 1,115 groves in Project 4 covering approximately 223 hectares. Project 4 is of central importance in the present appeal.

10 On or about 28 March 2008, the investors in Projects 5 and 6 removed AOL as the responsible entity of those projects and replaced it with Huntley. On or about 29 April 2008, the investors in Project 4 took the same actions in respect of Project 4. AOL was removed as the responsible entity of Projects 1, 2 and 3 in November 2008.

11 In 1997, AOHL, AOL and Collective Olive Groves Ltd (In Liquidation) (COGL) entered into a water supply agreement pursuant to which AOHL agreed to supply water to the projects.

12 At all relevant times:

(a) COGL has owned the land upon which all six of the projects have been conducted; and

(b) AOHL has controlled the principal sources of water for irrigating Projects 1 to 4.

13 Important amendments were made to the water supply agreement in late 2002 at the behest of the new owners of AOL who took control of AOL at about that time. By agreement styled Consolidated Water Supply Agreement dated 22 October 2002and executed on the same day (the CWSA), AOHL, AOL and COGL consolidated the terms of the water supply agreement as at 22 October 2002 into one document. This document included the 2002 amendments.

14 Under the CWSA, AOHL agreed to supply water to AOL in its capacity as the responsible entity of Projects 1 to 4 and probably also of those additional projects that might be subsequently undertaken as part of the Yallamundi plantations provided that those projects could be supplied with water from Yallamundi Lagoon.

15 AOHL contended at trial that, as a consequence of the members’ resolutions by which AOL was removed and replaced as the responsible entity of Projects 4, 5 and 6, Huntley became obliged to honour the obligations of AOL under the CWSA. According to AOHL, included amongst those obligations was the obligation to pay for water kept available by AOHL for supply to Projects 4, 5 and 6 after Huntley became the responsible entity of those projects. The amount claimed from Huntley by AOHL on a pro rata basis as a debt on this account was $486,504.77 plus interest. That amount comprised the total of the amounts charged in several tax invoices issued by AOHL to Huntley in the period from March 2008 to mid-September 2008 for water which AOHL said it had kept available for supply to Projects 4, 5 and 6 in that period. This amount comprised a pro rata allocation to Projects 4, 5 and 6 of the annual base fee payable to AOHL under cl 5 of the CWSA for the months of April to September 2008. It did not represent a charge for water actually supplied. It was AOHL’s case at trial that Huntley became liable to pay this amount by reason of the operation of s 601FS and s 601FT of the Act, as applied to the CWSA.

16 Huntley argued that it was not liable to pay the amounts claimed by AOHL and refused to pay those amounts.

17 AOHL took the view that Huntley’s refusal to pay amounted to a repudiation of the CWSA. By letter dated 2 October 2008 from the solicitors for AOHL to the solicitors for Huntley, AOHL accepted Huntley’s alleged repudiation of the CWSA and purported to terminate the CWSA on account of that repudiation as and from 9 October 2008. As mentioned at [10] above, AOL was subsequently removed and replaced as the responsible entity of Projects 1, 2 and 3.

18 At trial, Huntley admitted that it had refused to pay the amount of $486,504.77 invoiced to it by AOHL but denied that it was liable to do so. It contended that:

(a) It was not a party to the CWSA and did not otherwise have any liability or any obligations whatsoever under the CWSA because, upon the true construction of the CWSA, when the investors in Projects 4, 5 and 6 resolved to remove AOL as the responsible entity of those projects and to replace it with Huntley, both AOL and Huntley (as AOL’s successor in title) were thereupon released from any further obligation to pay the annual base fee required to be paid under cl 5 of the CWSA;

(b) In the alternative, s 601FS(1) and s 601FT(1) never applied to Huntley in the circumstances of the present case because the claimed debt was a liability for which AOL could not have been indemnified out of the scheme property of Projects 4, 5 and 6 if it had remained the responsible entity of those projects (see s 601FS(2)(d) and s 601FT(2) of the Act). Huntley argued that, under the contracts which bound AOL and the investors in the projects, AOL was obliged to secure an adequate supply of water for the projects and to pay for the cost of doing so out of its own assets; and

(c) Further, or in the alternative, the CWSA should be set aside because it was unconscionable for AOHL to seek to enforce its payment rights under the CWSA in circumstances where no water had been supplied to Huntley pursuant to that agreement. In support of this contention, evidence was led on behalf of Huntley to the effect that the only water which Huntley and its manager took in the relevant period in order to irrigate any of Projects 4, 5 and 6 was a total of 8 megalitres from the Project 5 dam. The evidence was that that water had irrigated Projects 5 and 6 only and that it had been drawn from the Project 5 dam on 6 April 2008 and on 7 April 2008. Huntley contended that that water was not supplied by AOHL under the CWSA because the Project 5 dam was not within the definition of Water Resource under the CWSA. It also contended that the market value of 8 megalitres of water at Yallamundi in March/April 2008 was between $400.00 and $800.00 (ie between $50.00 and $100.00 per megalitre).

19 In addition to its debt claim, AOHL also claimed damages for Huntley’s allegedly repudiatory breach of contract. The amount claimed by AOHL by reason of Huntley’s alleged repudiation of the CWSA was $9,620,026 plus interest.

20 In the alternative, AOHL claimed reasonable compensation for the supply of water to Huntley for Projects 4, 5 and 6 after Huntley became the responsible entity of those projects. The causes of action relied upon were estoppel and unjust enrichment. A common law count in quasi-contract (quantum valebat) was probably also included although the pleading in this respect is not at all clear. No specific sums were claimed in respect of these additional causes of action.

21 The learned primary Judge dismissed all of AOHL’s claims with costs(Australian Olive Holdings Pty Ltd v Huntley Management Ltd (2009) 76 ACSR 256).

22 On appeal, the following issues arise:

(a) Whether, upon the true construction of the CWSA, subcll 7.1(a)(iii), (b), (c) and (d), apply only where AOL is removed in accordance with the Act as the responsible entity of those projects covered by the CWSA or where AOL retires from that position in accordance with the Act and no replacement responsible entity is appointed (our emphasis) (as submitted by AOHL) or whether those subclauses apply whether or not a replacement responsible entity is appointed with the consequence in the present case that AOL was released from any further obligation to pay the annual base fee required to be paid pursuant to cl 5 of the CWSA immediately upon AOL’s removal as the responsible entity in respect of one or more of the projects or, alternatively, in respect of all six projects, which removal was effected progressively during 2008 (as argued by Huntley). AOL was removed as the responsible entity of Projects 4, 5 and 6 in March and April 2008 and removed from the last of the remaining projects in November 2008.

(b) In the event that Huntley’s construction of subcl 7.1(a)(iii) is preferred by the Court, whether that clause is void as against public policy.

(c) Whether the provisions of Chapter 5C – Managed Investment Schemes – of the Act operate to alter the answer that would otherwise be given to the questions posed in subpar (a) above. This issue gives rise to the following subsidiary issues:

(i) Whether the provisions of s 601FS(1) and s 601FT(1) of the Act are limited to those rights, obligations and liabilities of the former responsible entity which are capable of having ongoing operation after the change in the responsible entity; and

(ii) Whether the liability of AOL to pay the annual base fee required to be paid pursuant to cl 5 of the CWSA was a liability for which AOL could not have been indemnified out of the scheme property of Projects 4, 5 and 6 if it had remained the responsible entity of those projects. This issue principally involves the true construction of the Constitution of the relevant schemes (especially cl 8.1 thereof) and of the relevant Grove Agreements entered into between AOL and individual investors in the schemes (called members in those agreements).

(d) Whether, upon the true construction of the CWSA and having regard to the correct interpretation of s 601FS of the Act, the annual base fee payable under cl 5 of the CWSA is a single indivisible sum or is a sum of money which can be apportioned to individual projects covered by the CWSA in respect of only part of each yearly period to which such annual base fee is referable.

The Reasons of the Primary Judge

23 The primary Judge accepted Huntley’s submissions as to the correct construction of the CWSA. In particular, his Honour held that:

(a) Subparagraphs (i) to (iii) of subcl 7.1(a) of the CWSA describe events or circumstances which make it no longer possible for AOL to take water from AOHL and to discharge those of its obligations as responsible entity that are relevant to the CWSA (Reasons at [79]);

(b) Subclause 7.1(b)(i) distinguishes between obligations that accrued before and obligations that accrued after the event or set of circumstances referred to in subcl 7.1(a) occurred or commenced to exist (Reasons at [80]);

(c) In contractual terms, cl 6.3 and subcl 7.1(b) of the CWSA say nothing about the responsibility of a newly appointed responsible entity that replaces an incumbent responsible entity (Reasons at [80]);

(d) The CWSA did not impose obligations on a newly appointed responsible entity because such newly appointed responsible entity was not a party to the CWSA (Reasons at [80]);

(e) The term Manager is not defined in the Dictionary set out in Schedule 1 to the CWSA. The term is used simply to denote AOL, without any reference to a successor responsible entity (Reasons at [80]);

(f) Subclause 7.1(b)(ii) and subcl 7.1(b)(iii) establish and mandate a regime that must be entered into immediately by AOHL and COGL in the event that AOL is removed or retires as responsible entity. Subclause 7.1(c), which provides for the transfer of the pumping equipment and reticulation equipment to COGL, is consistent with that regime (Reasons at [81]);

(g) Clause 7.1 of the CWSA is not restricted in its application to circumstances where there is no responsible entity in place (for whatever reason) but rather applies generally with the consequence that, should AOL be removed or retire as responsible entity of the Projects (as defined in the CWSA), subcll 7.1(b), (c) and (d) would come into play so that there would be no right, obligation or liability to which Huntley, as successor responsible entity to AOL, could succeed (Reasons at [82] and [83]);

(h) The provisions of s 601FS and s 601FT of the Act do not alter the conclusions summarised at subpars (a) to (g) above. This is because there would be no rights, obligations and liabilities of the former responsible entity which have ongoing operation after the retirement or removal of AOL. The CWSA spells out, in express terms, the consequences of the retirement or removal of AOL. There are no “shoes” belonging to AOL into which Huntley might step (Reasons at [85]); and

(i) The members of a managed investment scheme, when considering whether to remove or replace a responsible entity, should take into account the terms of all relevant contractual arrangements, as indeed should the incoming responsible entity (Reasons at [86]).

24 Huntley advanced two additional arguments at trial which it contended defeated AOHL’s contractual claim in any event. Given the views which the primary Judge expressed in respect of Huntley’s contractual claim, it was strictly speaking unnecessary for him to address these additional arguments. However, he did so and, in respect of these additional arguments, concluded as follows:

(a) Section 601FS(2)(d) and s 601FT(2) did not apply, in the circumstances of the present case, to defeat AOHL’s contractual claim. Subclause 8.1(a) of the Constitution provided an appropriate indemnity in favour of AOHL (see Reasons at [88]–[106], esp at [103]); and

(b) The CWSA constituted an entire agreement and did not accommodate a pro rata apportionment of the fees payable by AOL to AOHL (Reasons at [107]–[120] esp at [114]). Accordingly, his Honour ultimately held that it was not open to AOHL to sue Huntley on the basis that Huntley was liable to pay a pro rata part of a CPI-adjusted base fee of $1,490,000 (Reasons at [120]).

25 AOHL also claimed an amount equal to the pro rata apportionment of the contractual fee as a claim in restitution. His Honour rejected that claim (see Reasons at [120]–[133]). His Honour concluded that no relevant benefit had been conferred on Huntley; that AOHL had failed to prove that water alleged to have been supplied to Huntley had in fact been supplied by it; and, finally, that AOHL had failed to prove that it had suffered detriment. There was no challenge in the appeal to his Honour’s rejection of AOHL’s claim in restitution.

Issue 1: The True Construction of Clause 7.1 of the CWSA

The Terms of the CWSA

26 Under the CWSA, AOL is named as Manager, AOHL is named as Water Owner and COGL is named as Land Owner. In the Dictionary in Schedule 1 to the CWSA, Land Owner is defined as COGL “or any permitted successors or assigns which own the Land”. Water Owner is defined as “The registered proprietor for the time being of the Water Land [which is also a defined term], but not the Land Owner”. In the Dictionary, the current registered proprietor of the Water Land is identified as AOHL. The Water Landis the land upon which Yallamundi Lagoon is located. Manager is not defined in the Dictionary.

27 According to Schedule 2 – Rules for Interpretation, in the CWSA, unless the context indicates a contrary intention:

…

(d) a person includes their executors, administrators, successors, substitutes (for example, persons taking by novation) and assigns

…

(f) except in the dictionary, headings do not affect the interpretation of this Agreement

…

(l) the defined terms in Schedule 1 have the meaning given them in that schedule except where the context otherwise requires.

Thus, unless the context indicates a contrary intention, the references throughout the CWSA to the Manager encompass a reference to AOL and to its successors, substitutes and assigns.

28 Manager is not used in Chapter 5C of the Act. It is a term used in previous legislation in order to denote a person or role broadly equivalent to that of responsible entity under Chapter 5C.

29 In the prospectus for Project 4, AOL was described as the “Responsible Entity/Manager” of Projects 1 to 4. In the Constitution for Project 4, AOL is referred to as the “Responsible Entity” of that project.

30 It is clear that AOL entered into the CWSA in its capacity as the responsible entity of Projects 1 to 4, those projects being the only projects established by it as at 22 October 2002 (the date of the CWSA) which were being conducted by it as managed investment schemes as at that date and which were dependent upon Yallamundi Lagoon as their water resource (see the definition of Projects in the Dictionary).

31 The recitals in the CWSA are in the following terms:

A. The Manager has established Projects and intends to establish further Projects for the planting, growing, harvesting and marketing of olives for commercial gain.

B. The Manager has entered Grove Agreements with the Members of the Projects. Under those Grove Agreements the Manager has agreed to manage the Members’ Groves.

C. The Manager is obliged under the Grove Agreements to irrigate the Members’ Groves.

D. The Water Owner owns the Water Land. The Water Resource is located on the Water Land.

E. The Water Owner has agreed to supply water and the Manager has agreed to take water to enable the Manager to comply with its duty to irrigate Members’ groves under the Grove Agreements.

F. The terms of this Agreement as varied by the Deed of Variation follow.

32 Clauses 1 and 2 of the CWSA are in the following terms:

1 Definitions

1.1 Dictionary

Except for terms specifically defined in Schedule 1 in this Agreement the dictionary of terms used in this Agreement is the same as that in Schedule 1 of the Constitutions.

1.2 Rules for Interpretation

The rules for interpreting this Agreement are the same as those in Schedule 2 of the Constitutions.

2 Supply of Water

(a) The Water Owner agrees to supply water to the Manager and the Manager agrees to take water from the Water Owner in the manner and on terms in accordance with this Agreement.

33 The term of the CWSA is expressed to be 80 years after the commencement of the CWSA (subcl 3(b)). According to its terms, the CWSA was expected to be in force until at least 2077. However, the term of Project 4 was to come to an end by no later than 30 June 2023 (cl 11.2 of the Constitution for Project 4) and we will assume that the outer limit of the term of both Project 5 and Project 6 was the same date. It seems that Projects 1, 2 and 3 were also required to be brought to an end by no later than 30 June 2023. Thus, the parties to the CWSA consciously embraced the idea that, subject to an early termination of the CWSA in accordance with its terms, the term of the CWSA would endure long past the expiry date of the projects. This conclusion is also supported by the terms of subcl 4.1(e) of the CWSA (which is extracted at [34] below). That clause expressly contemplates the CWSA remaining on foot after the projects have come to an end. The term of the CWSA was not, therefore, the same as the expected life of the projects.

34 Subclauses 4.1(a) to 4.1(f) provide:

4 Obligations of parties

4.1 Water Owner’s obligations

The Water Owner must observe and perform the following obligations:

(a) Subject to clause 4.1(b), supply the Manager with a maximum annual allocation of up to five megalitres of water per hectare of Groves and, if relevant, supply water for each Grove to which the Manager is obliged to supply water under any Grove Agreements even if the Manager is not obliged to continue carrying out the remaining duties under any of those Grove Agreements.

(b) For Projects in existence at 1 July 2002 the Water Owner must supply the Manager with the following water allocations:

(i) Up to 0.8 megalitres of water per annum for each Grove that is part of a Project based on an individual Grove size of 1,600 square metres.

(ii) Up to 1.0 megalitre of water per annum for each Grove that is part of a Project based on an individual Grove size of 2,000 square metres.

(c) For Projects which have commenced or will commence subsequent to 1 July 2002, the water allocation for each Grove will be an amount that equates to an allocation of up to five megalitres per hectare of Groves.

(d) In the event that at any time during the term of this Agreement the Water Resource is less than total capacity, supply the Manager with a pro-rata amount of water under clauses 4.1(a), 4.1(b) or 4.1(c) (as the case may be) which is in the same proportion that the lesser amount bears to the total capacity of the Water Resource.

(e) For the sake of clarity, following the end of the Projects (whether by completion of their terms or prior termination) the provisions of clauses 4.1(a) to (d) of this clause 4, and other relevant parts of this Agreement, must be read and interpreted so as to apply as if the supply of water is not per hectare of Groves, but per hectare of the Land planted to olive trees.

(f) Do all things necessary to maintain the availability of the supply of water to the Manager in accordance with this Agreement, including maintain, and comply with the conditions of, the water licence attached or relating to the Water Land.

35 The remaining subclauses of cl 4.1 provide that AOHL is to protect the Water Resource (subcl 4.1(g)), is to allow the Manager free and uninterrupted access to the Water Land (subcl 4.1(h)), is not to agree to supply any third party with water from the Water Resource (subcl 4.1(i)) and is not to use water from the Water Resource for its own benefit (subcl 4.1(j)) (other than in the circumstances provided for in subcl 7.2(b)). Under subcl 4.1(h), AOL’s access to the Water Land is expressed to be for the purpose of installing and maintaining its pumping and reticulation equipment and for the purpose of operating and maintaining Yallamundi Lagoon as a Water Resource for the projects.

36 Clause 4.2 provides:

4.2 Manager’s obligations

The Manager must -

(a) pay the Water Owner the fees provided for in this Agreement

(b) maintain the Reticulation Equipment at its cost

(c) maintain the Pumping Equipment at its cost, and

(d) operate and maintain the Water Resource in a good and workmanlike manner in order to maintain the Water Resource, its water capacity and improve reticulation.

37 Clause 5.1, subcl 5.2(a) and subcl 5.2(b) are in the following terms:

5 Fees and costs

5.1 Fees payable

In consideration of the Water Owner supplying water under this Agreement the Manager must pay to the Water Owner a fee. The fee will be payable in the manner provided for in this clause 5.

5.2 Annual Base Fee

(a) Notwithstanding the provisions of this Agreement before it was varied by the Deed of Variation, the parties agree that on and from 1 July 2002 the base fee per Grove payable under this Agreement will be replaced by an annual base fee. The annual base fee will be payable in the manner and at the times provided in this clause 5.2.

(b) The annual base fee for the year commencing on 1 July 2002 will be $1,490,000 per annum. Any amount paid by the Manager to the Water Owner under the terms of this Agreement before it was varied by the Deed of Variation relating to the period on or after 1 July 2002 will be credited against the annual base fee due from the Manager to the Water Owner for the year commencing on 1 July 2002.

38 Subclause 5.2(c) provides for an increase in the annual base fee in line with CPI movements, such increase to be effected on 1 July in each year after 2002. Clause 5.3 provides that there should be no reduction in the annual base fee in the event that there is a pro-rata reduction in the allocation of water pursuant to subcll 4.1(a) to (d).

39 Clause 5.4 and cl 5.5 provide:

5.4 Payment of annual base fee

On and from 1 July 2002 the Manager will pay the annual base fee, free of any deductions, to the Water Owner by equal monthly instalments in advance on the first day of each month with, if applicable, a proportional payment for any broken portion of a month at the termination of this Agreement.

5.5 Debt due

The annual base fee payable under this Agreement is a debt due and owing by the Manager to the Water Owner. However, nothing in this Agreement prevents the Manager and Water Owner from agreeing in writing to a different payment arrangement in respect of the annual base fee.

40 Under cl 6.1 and cl 6.2 of the CWSA, the Manager is free to assign its rights and interests under the CWSA provided certain conditions are met.

41 Clause 6.3 provides:

6.3 Retirement or replacement of Manager

The parties acknowledge that in respect of Projects established by the Manager as managed investment schemes and which are dependent upon the Water Resource the Manager may retire or be removed under the Act. The procedure set out in Clause 7 must be followed by the Manager if the Manager retires or is removed under the Act.

42 Subclauses 7.1(a), (b) and (c) of the CWSA are in the following terms:

7. Continuing Obligations

7.1 Termination of Projects

(a) This clause 7.1 applies if –

(i) the Projects end or are validly terminated for any reason

(ii) the Manager is no longer the lessee under the Lease for any reason, including but not limited to valid termination of the Lease by either party or in accordance with clause 6 of this Agreement, or

(iii) for any reason there is a removal or retirement of the Manager under the Act.

(b) If any of the events in clause 7.1(a) occur, and in the case of the event in clause 7.1(a)(i), the Manager is not the manager of the olive groves on the Land, then from the time that the event occurs -

(i) the Manager will be released from any further obligation to pay the annual base fee under this Agreement (but all other accrued rights, liabilities and obligations that arose prior to the time that the event occurs remain in addition to the obligation of the Manager under clauses 7.1(c) and (d))

(ii) the Water Owner and the Land Owner must immediately enter arrangements with each other on substantially the same terms as this Agreement in order to maintain a water supply to the Groves, or that part of the Land planted to olive trees (as the case may be), which for the sake of clarity includes -

– the Water Owner and the Land Owner entering a lease on substantially the same terms as the Lease, and

– payment of the annual base fee by the Land Owner to the Water Owner which will be payable from the date that the event referred to above occurs, and

(iii) the Water Owner and the Land Owner must do all things and enter any documentation necessary to give effect to those arrangements contemplated by clause 7.1(b)(ii).

(c) If any of the events in clause 7.1(a) occur, but in the case of the event in clause 7.1(a)(i), the Manager is not the manager of the olive groves on the Land, then the Manager must transfer ownership of the Pumping Equipment and the Reticulation Equipment to the Land Owner at a price to be agreed between the Manager and the Land Owner. The Manager and the Land Owner agree the transfer price will be no less than the replacement cost of the Pumping Equipment and the Reticulation Equipment at the time the event in clause 7.1(a) occurs together with the cost of all associated civil works that would be required to install such equipment. The parties agree the Pumping Equipment and the Reticulation Equipment will at all times remain on the Land and the Water Land, as the case may be, in accordance with the provisions of the Lease.

43 Under cl 7.2 of the CWSA, various easements are required to be granted in favour of the Water Owner and the Land Owner. In cl 7.2, the parties expressly agree that those easements are required in order to protect the interests of the investors in the projects and, in particular, to do so by ensuring a continuous and satisfactory supply of water to the projects.

44 Clause 8.1 of the CWSA gives to AOHL the power to terminate the CWSA in the event that the Manager breaches its obligations under that agreement and fails to remedy that breach within 30 days of receiving written notice of that breach from AOHL. Under cl 8.2 of the CWSA, the Manager has a right to terminate the Agreement should AOHL breach its obligations thereunder and fail to rectify that breach within 30 days of receiving written notice of that breach from the Manager.

45 Clause 8.3 of the CWSA is in the following terms:

8.3. Consequences of termination

(a) If this Agreement is terminated, then the rights and obligations of the parties under the provisions of this Agreement that are not subject to clause 8.3(b) are terminated, but all accrued rights, liabilities and obligations that arose prior to the termination remain, including the liability of the Manager to pay outstanding fees under this Agreement.

(b) The rights and obligations imposed on the parties by clause 7.1 do not merge on termination of this Agreement and continue to bind the parties after termination.

46 Schedule 1 – Dictionary defines a number of terms used in the CWSA. In addition to those terms already mentioned, the following terms are presently relevant:

Agreement The water supply agreement originally entered in 1997 between Australian Olive Holdings Ltd ACN 078 885 042, Australian Olives Ltd ACN 078 862 085 (and endorsed by Collective Olive Groves Limited ACN 079 354 742) including all schedules, annexures and variations that have been made to that agreement.

Constitutions The constitutions which established and/or govern the Projects.

Deed of Variation The deed that the Manager, the Water Owner and the Land Owner executed in or about October 2002 which varies the Agreement.

Groves Those Groves which are the subject of valid and subsisting Grove Agreements and which otherwise have the same meaning as that term in the Constitutions.

Land The land from time to time on which Projects are established, excluding the Water Land.

Lease The lease to be entered between the Water Owner as lessor and the Manager as lessee, or the lease which may be entered by the Water Owner as lessor and the Land Owner as lessee if clause 7.1(b) applies, and in either case which will be on terms substantially the same as those appearing in Schedule 5.

Projects Any olive farm investment projects established by the Manager, and now conducted, as managed investment schemes and which are dependent upon the Water Resource.

Water Resource The lagoon located on the Water Land.

47 Schedules 3 to 5 of the CWSA contain the form of easements and lease contemplated by the CWSA.

Other Relevant Contextual Matters

48 Each investor in Projects 4, 5 and 6 was obliged to enter into a contract entitled Grove Licence Agreement. The parties to each Grove Licence Agreement were COGL, AOL (as the Responsible Entity) and each individual member of the projects. Under the standard-form Grove Licence Agreement, COGL granted a licence to the particular member to use and occupy that part of the Project Land on which the particular member’s olive grove is located. Under this agreement, the member is obliged to permit the responsible entity (AOL), its employees and agents, to enter the grove in order to enable the responsible entity to perform its obligations under the Grove Licence Agreement and also to carry out its obligations under a separate agreement entitled Grove Agreement. Under the Grove Licence Agreement, the trees in the grove remain the property of COGL. Under that agreement, it is the responsible entity which is to carry out the harvesting of olives from the trees in the grove. COGL has a right to terminate the Grove Licence Agreement. In the event that it does so, the responsible entity is entitled to terminate the Grove Agreement and the member in question loses all rights as a member of the particular project. The term of the Grove Licence Agreement is to expire by no later than 30 June 2023.

49 Each of Projects 4, 5 and 6 is governed by a Constitution. Each Constitution for each of those projects is in the same terms.

50 Clause 6.1 of the Constitution for Project 4 provides that AOL must wind up the project or cause it to be wound up if, inter alia, the project should be without a responsible entity (subcl 6.1(b)) or if the members hold a validly called meeting and vote by extraordinary resolution to remove the incumbent responsible entity, but do not, at the same meeting, pass an extraordinary resolution appointing a new responsible entity which has consented to become the project’s responsible entity (subcl 6.1(d)).

51 In addition, each member of the projects is obliged to enter into a Grove Agreement with the responsible entity. The terms of the Grove Agreements entered into in respect of Projects 4, 5 and 6 are relevantly identical.

52 Under the standard-form Grove Agreement, the responsible entity is obliged to establish the necessary seedlings, to carry out the necessary irrigation works to ensure proper reticulation of water to the seedlings and thereafter to maintain an adequate supply of water to the member’s grove in accordance with the terms of the Grove Agreement. The responsible entity is entitled to an initial fee per grove of $8,580.00 and annual fees thereafter. The term of the Grove Agreement is to come to an end by no later than 30 June 2023.

53 On appeal, there was no material before the Court proving the contractual arrangements that subsisted in respect of Projects 1, 2 and 3. Nor was it clear to us whether there was evidence of those arrangements before the primary Judge.

54 Schedule 5 to the CWSA is a form of lease over the Water Land intended to be granted by AOHL to AOL in order to enable AOL to occupy the Water Land for the purpose of plantation maintenance and, more particularly, to pump and reticulate water. It seems that this lease was entered into in order to better secure AOL’s rights of access to Yallamundi Lagoon and the administration block afforded to AOL by AOHL pursuant to subcl 4.1(h) of the CWSA.

55 Under this lease:

(a) AOL is entitled to pump and reticulate water from Yallamundi Lagoon at its sole expense (cl 4.01);

(b) The sole permitted use of the demised land and premises is for:

Agricultural plantation, maintenance, management, promotion, and ancillary or related purposes

(cl 5.01 and Item 5 of the Schedule);

(c) AOL is obliged to maintain the pumping and reticulation equipment and associated works in good repair and efficient working order (cl 7.01);

(d) AOL is not permitted to assign the benefit of the lease without the prior written consent of AOHL. An exception to this is an assignment to an assignee of the CWSA (cl 13.01);

(e) Upon termination of the lease, the pumping and reticulation equipment is to remain on the demised premises and to be delivered up to AOHL in good order and condition (cll 16.01, 16.02 and 16.03); and

(f) If the CWSA is terminated or if the tenant (AOL) is released from the obligation to continue to pay the annual base fee as manager under the CWSA, then the lease is automatically terminated (cl 16.04).

56 The term of the lease was to be almost 21 years, commencing on 1 October 2002 and ending on 30 June 2023. There were options for renewal at 10 year intervals commencing on 1 July 2023, the first renewal date. The end of the last option lease was 30 June 2078.

57 Thus, the lease was to terminate at the same time as the projects were, at the latest, to terminate, subject to successive options designed to take the lease up to a date which more or less lined up with the expiry of the CWSA.

58 Only approximately 18% of Project 5 and none of Project 6 can be irrigated with water supplied from Yallamundi Lagoon. All of Project 6 and approximately 82% of Project 5 are located on the southern side of Speers Creek and there is no infrastructure enabling the pumping of water from Yallamundi Lagoon across Speers Creek. The only water resource (apart from rain water) which is available for the irrigation of those groves which are on the south side of Speers Creek is the Project 5 dam. The Project 5 dam is filled by overland flow water, not with water from Yallamundi Lagoon. Therefore, the CWSA never applied to Project 6. Although that part of Project 5 located north of Speers Creek was potentially able to be brought under the umbrella of the CWSA, that was never done. For present purposes, therefore, of the three projects with which this appeal is concerned (Projects 4, 5 and 6), the CWSA applied only to Project 4. Therefore, under the CWSA, AOHL was obliged to supply water to irrigate only Projects 1 to 4. AOL’s payment obligations under cl 5 of the CWSA related only to the supply of water to those four projects. For this reason alone, Huntley could never have been made liable in respect of the supply of water to Projects 5 and 6.

Consideration

59 It was submitted on behalf of Huntley that cl 7.1 of the CWSA is unambiguously clear in its terms. The parties to the CWSA, according to the submissions made on behalf of Huntley, fully intended to trigger the consequences and actions embodied in subcl 7.1(b) and subcl 7.1(c) of the CWSA as soon as the original manager under the CWSA (AOL) was removed or retired as manager (responsible entity) of any one or more of the projects covered by the CWSA as at the date of its execution (viz Projects 1 to 4). It was submitted on behalf of Huntley that it was open to the parties to the CWSA to make an agreement which, in effect, denied to any incoming responsible entity control over the water supply for irrigating the groves in the projects supported by the CWSA and which compelled the ultimate transfer to COGL of all relevant pumping and reticulation equipment.

60 AOHL submitted that such a construction of cl 7.1 did not make good commercial sense.

61 Counsel for AOHL submitted that:

(a) Upon the true construction of cl 7.1, the essential common feature of each of the events described in subcll 7.1(a)(i) to (iii) is the termination of the projects. The consequences described in subcll 7.1(b) and (c), does not sit comfortably with a state of affairs whereby the projects continued beyond the termination of the CWSA;

(b) The event covered by subcl 7.1(a)(i) is the termination of the projects themselves. The event described in subcl 7.1(a)(ii) (being the termination of the Lease) is an event which has the necessary consequence of terminating the projects because, upon termination of the Lease, the responsible entity and the investors in the projects cease to have access to the Water Resource. Accordingly, subcl 7.1(a)(iii) should be similarly construed as applying only if there is an event which effectively terminates the projects. Having regard to the various matters of context to which reference has been made at [48]–[58] above, subcl 7.1(a)(iii) should be read as if the following words appeared at the very end of that subclause, namely “… without a replacement being appointed”; and

(c) AOHL advanced the following reasons in support of these submissions, namely:

(i) Such a construction would give effect to the objective commercial purpose of the CWSA. The identity of the responsible entity under the CWSA and related agreements, at any given point in time, is irrelevant as long as that responsible entity is suitably qualified and appointed in accordance with the Act and the relevant contracts;

(ii) Any attempt to entrench the position of any particular responsible entity offended the obvious purpose of Ch 5C of the Act;

(iii) Clause 6.1 of the CWSA provides that the manager may assign its rights and interests under that Agreement. AOHL’s construction avoids any conflict between cl 6.1 and cl 6.3;

(iv) The CWSA contemplates AOL having a successor or substitute which (in light of s 601FS and s 601FT) is apt to include a new responsible entity; and

(v) Under the Constitutions for Projects 4, 5 and 6, the parties contemplated the possibility that a responsible entity could retire or be removed without replacement and that the consequence of that event was winding up (see cl 6.1 of the Constitution).

62 We think that the construction of cl 7.1 propounded by Huntley and accepted by the learned primary Judge is to be preferred. Our reasons for this conclusion are:

(a) The argument advanced by AOHL, both at trial and on appeal, was that, on the proper construction of subcl 7.1 of the CWSA, that clause is only triggered if the relevant event referred to in subcl 7.1(a) has the effect of terminating the projects. Thus, AOHL’s argument was put only as a construction argument. AOHL did not contend that the words which it sought to have added to the very end of subcl 7.1(a)(iii) (viz without a replacement being appointed) should be read into that clause as an implied term;

(b) AOHL’s contentions in support of its ultimate submission were that the consequences spelt out in subcl 7.1(b) and subcl 7.1(c) only made sense in circumstances where the projects had come to an end in the ordinary course of events or had been terminated. It was therefore submitted that subcll 7.1(a)(i), (ii) and (iii) only operated when the projects had come to an end or were terminated. It was also submitted that the Court should avoid a construction of cl 7.1 which allows the parties to the CWSA to circumvent the evident object of s 601FS and s 601FT of the Act;

(c) Contrary to the submissions of AOHL, however, although subcl 7.1(a)(i) clearly contemplates the end of the projects or the valid termination of the projects as the relevant trigger for the operation of cl 7.1, the event postulated in subcl 7.1(a)(ii) is not an event which necessarily involves the termination of the projects. The event postulated in subcl 7.1(a)(ii) is the termination of the lease of Yallamundi Lagoon and the surrounding land upon which the administration block is constructed. That termination might occur because there is a default on the part of AOL under the lease, because the CWSA is terminated or because there is an assignment by AOL of its rights and interests under the CWSA pursuant to cl 6.1 of the CWSA. Such an assignment might involve the assignment of the lease or the termination of the lease and the execution of a fresh lease between AOHL and the new manager (responsible entity). Both of these latter circumstances are expressly contemplated by subcl 7.1(a)(ii). However, as already mentioned, none of these postulated events necessarily involves the termination of the projects. The Grove Agreements, the Grove Licence Agreements and the Constitutions would all remain on foot notwithstanding the termination of the lease. At most, the occurrence of these events might make it difficult for AOL or its replacement to perform its obligations to irrigate the projects pursuant to the Grove Agreements;

(d) When regard is had to the terms of subcl (b) and subcl (c) of cl 7.1, the essential trigger for the operation of the clause appears to be the removal or replacement of AOL as the manager (responsible entity) of the projects. If the relevant trigger is the occurrence of one or more of the events described in subcl 7.1(a)(i) of the CWSA, then not only must there be an end or valid termination of the projects for the consequences in subcl 7.1(b) and subcl 7.1(c) to follow, but there must also be satisfaction of a second requirement embodied in the following words in both subclauses viz “… and in the case of the event in cl 7.1(a)(i), the Manager is not the manager of the olive groves on the Land”. In other words, if the projects come to an end or are otherwise validly terminated but AOL is still the manager of the olive groves on the land, then subcl 7.1(b) and subcl 7.1(c) are not engaged;

(e) The Act does not expressly provide that any contract or any clause in a contract which prohibits the retirement or removal of a responsible entity of a managed investment scheme is void. Nor does the Act expressly prohibit or even address third party contractual provisions which might be seen as attempts to circumvent the policy of the Act to the effect that the members of a managed investment scheme should have the right to remove the responsible entity and replace it with a responsible entity of their choice. The provisions of the Act which deal with changing the responsible entity (s 601FJ to s 601FT) are part of the setting in which the CWSA is to be construed and thus potentially constitute a relevant surrounding circumstance in aid of that construction. In the present case, however, we think that those provisions provide little or no assistance in resolving the question of construction with which we are concerned. The Act does not prohibit parties to a contract pursuant to which services are provided to a responsible entity of a managed investment scheme for the purposes of that scheme from agreeing to terms which bring that contract to an end in the event that the incumbent responsible entity is removed. That which is not prohibited is permitted. It is no different from parties to such a contract agreeing that it should automatically come to an end if one of the parties becomes insolvent;

(f) Whilst the evident commercial purpose of the CWSA is to secure a long term water supply for irrigating the projects, that purpose is just as easily served by COGL directly arranging with AOHL the supply of water to irrigate the land upon which the olive trees are planted;

(g) It is true that the effect of subcl 7.1(b) and subcl 7.1(c) is that:

(i) The CWSA is terminated (see esp subcl 7.1(b)(ii));

(ii) The Manager is released from its obligation to pay future annual base fees under the CWSA;

(iii) AOHL and COGL are obliged to make a new contract substantially on the same terms as the CWSA in order to maintain a water supply to the Groves (if the projects are still on foot) or to that part of COGL’s land which is planted with olive trees (in the event that the projects are terminated); and

(iv) The Manager is obliged to sell and COGL is obliged to purchase the pumping equipment and reticulation equipment then being used to irrigate the projects but only on the basis that that equipment will remain on the plantation land and be used to irrigate the projects.

But the removal of the Manager as a party to the CWSA and the effective termination of the CWSA do not necessarily spell the end of the projects nor are the consequences described in subcl 7.1(b) and subcl 7.1(c) only consistent with the projects no longer being on foot. Once cl 7.1 is triggered, AOHL and COGL are obliged to maintain a water supply to the land where the olive trees are planted. Presumably, if the projects are still on foot, AOHL and COGL would only maintain that supply if satisfactory commercial terms are agreed to by the new responsible entity and (possibly) the investors in the projects;

(h) Under par (f) of the Rules for Interpretation applicable to the CWSA (Schedule 2 to the CWSA), unless the context indicates a contrary intention, headings do not affect the interpretation of the CWSA. No such contrary intention is indicated here. Therefore, we must ignore the headings when interpreting cl 7;

(i) Our preferred construction of cl 7.1 accommodates cl 6.3 whereas the construction advanced by AOHL does not. AOHL’s construction requires further words to be added to cl 6.3. There is no conflict between cl 6.1 and cl 6.3 of the CWSA when subcl 7.1(a)(iii) is properly understood. Those clauses say nothing about the responsibility of a newly appointed responsible entity that replaces an incumbent responsible entity; and

(j) Huntley’s construction recognises and sensibly accommodates the fact that the annual base fee required to be paid under the CWSA is paid for the supply of specified quantities of water to four projects—Projects 1 to 4. The quantum of the fee constitutes an agreed price for the supply of quantities of water for four projects (not three). If AOL is removed as the responsible entity/manager of one of those projects, assuming for the moment that the fee cannot be apportioned, upon AOHL’s construction, AOL would thereafter be required to pay the full fee notwithstanding the fact that the quantity of water required to be supplied to AOL will have been reduced. Clause 4.1 specifies the quantities of water to be supplied under the CWSA on a per hectare basis and thus by reference to the area of land involved. By way of contrast, the fee is a fixed sum ($1,490,000 per annum) subject to upward adjustment. It is not quantified contractually on a per hectare basis. It is not adjusted if the quantity of water required to be supplied is reduced because one of the projects (Project 4) is no longer covered by the CWSA.

63 Here, there was a removal of the Manager under the Act in April 2008 when the investors in Project 4 resolved to remove AOL as the responsible entity of that project. Subclause 7.1(a)(iii) was, therefore, engaged.

64 Despite the terms of par (d) of the Rules for Interpretation governing the CWSA, we think that the term Manager when used in cl 7.1 is a reference to AOL, and to AOL alone. In our view, the context indicates that rule (d) should not be applied to that term when it is used in cl 7.1. The consequences provided for in subcll 7.1(b), (c) and (d) are consequences which can only occur once. Further, in subcl 7.1(b) and subcl 7.1(c) there is a clear distinction being drawn between the Manager (referring to AOL) and the manager referring to the incumbent responsible entity whoever that may be. Finally, the Dictionary does not define Manager. Rather, the term appears to be deliberately confined to denoting the party named as Manager in the CWSA viz AOL.

65 The reference to “a retirement or removal” (our emphasis) in subcl 7.1(a)(iii) (our emphasis) is a reference to the retirement or removal of AOL as the responsible entity of at least one of the projects for which water is to be supplied under the CWSA. The definition of Projects in the Dictionary and the terms of subcll 4.1(a) to (e) make clear that projects which came into existence after 1 July 2002 but before 22 October 2022 were covered by the CWSA. Projects which commenced after 22 October 2002 were not covered by the CWSA, unless expressly brought within its scope by a variation to the CWSA. No such variation was ever agreed. Therefore, as noted at [58] above, Projects 5 and 6 were never covered by the CWSA. This conclusion is reinforced by the fact that the sole water resource referred to in the CWSA was Yallamundi Lagoon which could not service Project 6 nor could it service most of Project 5. For these reasons, we are of the view that the removal of AOL as the responsible entity of Projects 5 and 6 was not an event within subcl 7.1(a)(iii) and did not therefore engage cl 7.1.

66 The removal of AOL as the responsible entity of Project 4, however, was an event within subcl 7.1(a)(iii). As a matter of contract and ignoring the impact (if any) of s 601FS and s 601FT of the Act, the occurrence of that event triggered the consequences specified in subcll 7.1(b), (c) and (d) of the CWSA.

67 The consequences summarised at [62(g)] above flowed immediately upon the removal of AOL as the responsible entity of Project 4 (ie on or about 29 April 2008).

68 For these reasons, and subject to our consideration of the remaining issues, AOHL’s claim in debt, looked at solely as a matter of contract and assuming for the moment that Huntley can somehow be made liable under the CWSA, must inevitably be confined to Project 4 and must be confined to the months of May to September 2008.

Issue 2: Is Clause 7.1(a)(iii) of the CWSA Void as against Public Policy

69 AOHL submitted that subcl 7.1(a)(iii) is void as against public policy. It submitted that the purpose of Ch 5C, Pt 5C.2—Divisions 2 and 3 of the Act and the policy reflected in those provisions are to empower the members of a managed investment scheme to change the incumbent responsible entity and to do so with as little disruption to the scheme as possible.

70 AOHL submitted that, on Huntley’s construction of subcl 7.1(a)(iii), that subclause has the effect of defeating the members’ right under s 601FM to remove AOL as the responsible entity of those projects irrigated pursuant to the CWSA. It was further submitted by AOHL that subcl 7.1(a)(iii) was severable from the balance of the CWSA both by reason of the operation of cl 12 of the CWSA and under the common law test of severability.

71 These contentions were not advanced by AOHL at trial. For this reason, the learned primary Judge did not address them. However, Huntley has not suggested that AOHL ought not to be permitted to raise the point for the first time on appeal and, for our part, we see no reason why AOHL should be shut out from raising the point now. Accordingly, we propose to allow AOHL to argue that subcl 7.1(a)(iii) is void as against public policy.

72 In our judgment, subcl 7.1(a)(iii) does not have the effect which AOHL contended that it has. It does not prevent the investors in Projects 1 to 4 from removing AOL as the responsible entity of any of those projects. Rather, it simply spells out certain contractual consequences in the event that such action is taken. If the investors in any of those projects wish to remove AOL as the responsible entity of any of those projects, one of the matters which they might wish to consider is the wisdom of doing so in circumstances where such action will trigger the consequences laid down in subcll 7.1(b), (c) and (d). No issue of severance of subcl 7.1(a)(iii) arises.

73 The question of whether a contract which, unlike subcl 7.1(a)(iii) in the present case, does prevent the members of a managed investment scheme from removing the incumbent responsible entity is void as against public policy does not arise in the present case. The High Court has held that the question whether a contractual term is rendered void as a consequence of the breach of a statutory provision is ultimately one of statutory construction (see Australian Competition and Consumer Commission v Baxter Healthcare Pty Ltd (2007) 232 CLR 1 at 29 ([45]–[46]) per Gleeson CJ, Gummow, Hayne, Heydon and Crennan JJ and the cases cited in those paragraphs). Section 601NA of the Act explicitly states that a provision in the Constitution of a managed investment scheme which purports to provide that the scheme is to be wound up if a particular company ceases to be its responsible entity is of no effect (including for the purposes of s 601NE(a)). Section 601NA is an example of a statutory provision which, upon its true construction, renders void the offending contractual provision.

Issue 3: The Impact of Section 601FS and Section 601FT of the Act

The Interpretation and Relevance of s 601FS and s 601FT of the Act

74 Chapter 5C – Managed Investment Schemes of the Act now regulates managed investment schemes as defined in the Act. Such schemes must be registered with the Australian Securities and Investments Commission (ASIC) and must have a responsible entity. The responsible entity must be a public company and must hold an Australian financial services licence (s 601FA of the Act).

75 Part 5C.2 – Division 2 – Changing the Responsible Entity contains a number of provisions which govern and regulate what is to happen when the responsible entity is changed.

76 The members of the scheme may remove a responsible entity (s 601FM) and, subject to compliance with the requirements of s 601FL, a responsible entity may retire. Pursuant to s 601FN and s 601FP, a temporary responsible entity may be appointed.

77 The terms of s 601FJ to s 601FT make clear that, under the Act, a managed investment scheme must have an appropriately qualified responsible entity at all times. Should the members of a scheme fail to appoint a new responsible entity upon the retirement or removal of an incumbent responsible entity at the same meeting where they resolve to approve the retirement of the incumbent responsible entity or to remove that responsible entity and should no temporary responsible entity otherwise be appointed, the scheme must be wound up (s 601NE).

78 The evident object of these provisions is that a managed investment scheme must have an appropriately qualified responsible entity at all times and that the selection of that entity should be the right (and responsibility) of the members of the scheme.

79 Section 601FS and s 601FT are in the following terms:

601FS Rights, obligations and liabilities of former responsible entity

(1) If the responsible entity of a registered scheme changes, the rights, obligations and liabilities of the former responsible entity in relation to the scheme become rights, obligations and liabilities of the new responsible entity.

(2) Despite subsection (1), the following rights and liabilities remain rights and liabilities of the former responsible entity:

(a) any right of the former responsible entity to be paid fees for the performance of its functions before it ceased to be the responsible entity; and

(b) any right of the former responsible entity to be indemnified for expenses it incurred before it ceased to be the responsible entity; and

(c) any right, obligation or liability that the former responsible entity had as a member of the scheme; and

(d) any liability for which the former responsible entity could not have been indemnified out of the scheme property if it had remained the scheme’s responsible entity.

601FTEffect of change of responsible entity on documents etc. to which former responsible entity is party

(1) If the responsible entity of a registered scheme changes, a document:

(a) to which the former responsible entity is a party, in which a reference is made to the former responsible entity, or under which the former responsible entity has acquired or incurred a right, obligation or liability, or might have acquired or incurred a right, obligation or liability if it had remained the responsible entity; and

(b) that is capable of having effect after the change;

has effect as if the new responsible entity (and not the former responsible entity) were a party to it, were referred to in it or had or might have acquired or incurred the right, obligation or liability under it.

(2) Subsection (1) does not apply to a right, obligation or liability that remains a right, obligation or liability of the former responsible entity because of subsection 601FS(2).

80 In Re Investa Properties Ltd (2001) 187 ALR 462 at 465 ([11]), Barrett J correctly described the purpose of s 601FS as “to cause an incoming responsible entity to step into the shoes of its predecessor”. This statement of principle was followed by RD Nicholson J in Syncap Management (Rural) Australia Ltd v Lyford (2004) 51 ACSR 223.

81 Section 601FS(2) sets out four classes of rights and liabilities of the former responsible entity which are not to be taken over by the incoming new responsible entity.

82 Section 601FT of the Act gives effect to the principles embodied in s 601FS insofar as the interpretation of particular documents is concerned.

83 At [85] of his Reasons, the primary Judge said:

85 The question that then arises is whether ss 601FS and 601FT alter this result. In my opinion they do not. The construction supported by AOHL would involve re-writing the CWSA by omitting its various provisions as to what is to happen upon the removal or retirement of AOL as RE. I do not think that s 601FS(1) of the Act requires or permits this to be done. The “rights, obligations and liabilities of the former responsible entity” to which s 601FS(1) refers are impliedly limited to those that are capable of having an ongoing operation after the change in RE. Paragraph (b) of s 601FT(1) reflects this idea expressly in the words “that is capable of having effect after the change”. If the CWSA did not provide for the effect on it of a removal or retirement of AOL, it would make sense to conceive of the new RE as stepping into the shoes of the outgoing one. That would be a situation in which the rights, obligations and liabilities of the former RE had an ongoing operation.

84 We agree with the conclusions which his Honour expressed in that paragraph and with the reasons which he gave for those conclusions.

85 We have already concluded that, upon the true construction of subcl 7.1(a)(iii), when the investors in Project 4 removed AOL as the responsible entity of that project in April 2008, cl 7.1 was engaged. The consequences provided for in subcll 7.1(b), (c) and (d) then flowed. AOL, AOHL and COGL were bound to perform the obligations imposed upon each of them under those subclauses. AOL was no longer obliged to pay the annualised base fee under the CWSA. The only obligations imposed upon AOL which remained on foot were its obligations under cl 7.1 of the CWSA.

86 Under s 601FJ, AOL remained the responsible entity of Project 4 until ASIC’s record was altered to name Huntley as the responsible entity of that project. This occurred some time after the passing of the resolution to remove AOL as the responsible entity of that project. Clause 7.1 was triggered the moment that that resolution was passed and, as the primary Judge held, by the time Huntley became the responsible entity of Project 4, upon the true construction of the CWSA, there were no “shoes” referable to the CWSA into which Huntley could step. Save for its rights and obligations under cl 7.1, the rights and obligations of AOL as the Manager under the CWSA had evaporated.

Whether AOL had an Indemnity out of the Property of Projects 1 to 4 for the Annual Base Fee

87 At trial and on appeal (by way of Notice of Contention), Huntley argued that the obligation to pay the annual base fee or any proportion of that fee pursuant to the CWSA was not a liability for which Huntley became responsible by reason of its appointment as the responsible entity of Project 4 because it was a liability for which AOL could not have been indemnified out of the scheme property of Project 4 if it had remained that project’s responsible entity. This submission relies upon the exception embodied in s 601FS(2) and s 601FT(2) of the Act. For reasons which we have already explained, the appeal does not involve or concern Projects 1 to 3.

88 The Constitution for Project 4 was executed on 14 March 2001. A Supplemental Constitution was entered into on 16 May 2001.

89 The Constitution is a document entered into between AOL and the investors in Project 4. As at the date the Constitution was executed, there were no investors in Project 4. Those persons who ultimately became investors in Project 4 became liable under and took the benefit of the Constitution subsequently when they invested in Project 4.

90 The relevant provisions of the Constitution are cll 1, 3, 6, 7, 8, 11, 17, 24, 25 and the Dictionary in Schedule 1.

91 Clause 1 of the Constitution provides that it is binding upon all investors in Project 4 and upon AOL. Clause 3.1 provides that all Project Property will be held by AOL on trust for the investors in Project 4. The respective proportions in which those investors hold that property are set out in the Constitution (cl 16 and Item 2 of Schedule 3).

92 Clause 6 of the Constitution governs the winding up of Project 4. Subclauses 6.1(a) to (d) provide as follows:

6.1 Events which cause a winding up

The Responsible Entity must wind up the Project or cause the Project to be wound up in any one of the following circumstances:

(a) The Project comes to the end of its term (as set out in this Constitution).

(b) The Project is without a responsible entity.

(c) The Members hold a validly called meeting and vote by extraordinary resolution to direct the Responsible Entity to wind up the Project.

(d) The Members hold a validly called meeting and vote by extraordinary resolution to remove the Responsible Entity, but do not, at the same meeting, pass an extraordinary resolution choosing a new responsible entity that consents to becoming the Project’s responsible entity.

93 Subclauses (e) and (f) of cl 6.1 are not presently relevant.

94 Clause 6.2 and cl 6.3 deal with the mechanics of a winding up.

95 Clause 6.4 is in the following terms:

6.4 Termination of other agreements

During the winding up of the Project, the Responsible Entity may terminate any other agreements or arrangements it has entered into with the Members which relate to this Project. The Responsible Entity must give notice to the Members of the termination of those agreements or arrangements.

96 Clause 7.1 is found under the heading Fees and Expenses. Clause 7.1 and cl 7.2 are in the following terms:

7.1 Fees payable to the Responsible Entity

The Responsible Entity is entitled to be paid fees of the amount and in the manner set out in Item 3.

7.2 Recovery of costs

The Responsible Entity is entitled to recover costs from the Proceeds Fund of the kind and in the manner set out in Item 3.

97 Item 3 of Schedule 3 to the Constitution (as originally drafted) provides as follows:

Item 3 (clause 7.1)

The Responsible Entity is entitled to be paid by each Member the fees set out below:

(a) From the date an Applicant becomes a Member to the next 30 June, $8,580 for management of the Member’s Grove

(b) For the next financial year (1 July to 30 June) following the date an Applicant becomes a Member, $11,470 for management of the Member’s Grove

(c) For each subsequent financial year of the Project, a management fee equal to the previous year’s fee increased in accordance with movements in the CPI.

(d) For harvesting the Olives Attributable to a Member’s Grove, a fee equal to that amount the Responsible Entity actually expends in carrying out the harvesting duties

The Responsible Entity’s legal recourse for its fees and payments is through the Grove Agreements. The fees and payments are noted here as a matter of record.

All fees are exclusive of Goods and Services Tax.

98 The figure at par (b) of Item 3 in Schedule 3 to the Constitution was amended by the Supplemental Constitution. The amount of $11,470 was replaced with the amount of $1,470.

99 Clause 8 is headed Indemnity and Liability. Clause 8.1 provides:

8.1 Indemnity from the Project

(a) The Responsible Entity has a right of indemnity out of the Funds and the Project Property in respect of-

(i) any liability incurred by the Responsible Entity in the performance of its duties in respect of the Project, and

(ii) all fees payable to and costs recoverable by the Responsible Entity under this Constitution.

(b) However, this indemnity does not apply where there has been any negligence, deceit, breach of duty, fraud or breach of trust on the part of the Responsible Entity.

100 Clause 11 (which is headed Period and Termination of Project) sets out the term of Project 4 and contains provisions as to the termination of the project. Although it might appear that the term of the project was to be of the order of 80 years from early 2001, when subcl 11.2(b) is read with the Grove Licence Agreement used in respect of Project 4, it is clear that the project was intended to come to an end by 30 June 2023 at the latest.

101 Clause 11.3 provides:

11.3 Termination of Grove Licence Agreements and Grove Agreements

Upon the termination of this Project all of the rights and obligations under the Grove Licence Agreements and Grove Agreements cease and those agreements are automatically terminated. However, any rights which have accrued under those agreements prior to termination will remain.

102 Clause 11.5 requires that the responsible entity is to ensure that the land intended to be utilised for Project 4 is made available for the purpose of allocating groves to investors in Project 4.

103 Clause 17 provides that the Grove Licence Agreements and Grove Agreements entered into between the responsible entity and each of the investors in Project 4 are to be read subject to the terms of the Constitution for Project 4. Clause 17.4 and cl 17.5 regulate the way in which the project is to be managed in the event that some Grove Agreements and some Grove Licence Agreements are terminated while others remain on foot.

104 Clause 24 is headed Collections and Payments. Clause 24.1 and cl 24.2 are in the following terms:

24.1 Responsible Entity to collect income from the Investments

The Responsible Entity must collect, receive and get in all income from the Investments.

24.2 Payments in respect of the Project

(a) The Responsible Entity must pay from its own assets the following expenses:

(i) All costs, expenses, commissions, fees, rates, taxes (including income tax), supervision and management charges, and other charges or outgoings payable in accordance with this Constitution in respect of the Interests.

(ii) All fees and expenses of any agents appointed by the Responsible Entity.

(iii) All costs and expenses incurred in or in connection with the preparation of any amendments, modifications or additions to the provisions of this Constitution, unless otherwise provided by Law or as agreed by the Members.

(iv) Costs of convening and holding any meeting of Members, except as provided by Law.

(v) Any costs and disbursements reasonably and properly incurred which are payable to any consultant, adviser, specialist, accountant, lawyer or other professional consultants engaged by the Responsible Entity.

(b) The Responsible Entity does not pay any fee or outlay stated to be a payment due from Members under the Grove Licence Agreements or the Grove Agreements. These amounts must be paid by the Members.

105 Clause 25.3 provides that the investors are entitled to the surplus held in the project’s bank accounts after payment of all fees payable under the particular investor’s Grove Agreement and Grove Licence Agreement as well as any other amounts payable by the investors under the Constitution or under those Agreements.

106 In the Dictionary in Schedule 1 to the Constitution for Project 4, the definition of Responsible Entity is in the following terms:

Responsible Entity Includes the Responsible Entity for the time being and any other responsible entity appointed on the retirement or removal of the Responsible Entity.

107 At [48] above, we have briefly described the important terms of the Grove Licence Agreements entered into between COGL, AOL and the investors in Project 4.

108 The other important contract entered into between each of the investors and the responsible entity is the Grove Agreement referred to in Schedule 6 to the Constitution. The parties to each Grove Agreement entered into in respect of Project 4 were AOL and each particular investor in that project. In this Agreement, as in the Constitution and in the CWSA, the Water Resource is Yallamundi Lagoon and the Water Supply Agreement is the CWSA.

109 Clause 3 of the Grove Agreement provides that the Grove Agreement will come to an end by no later than 30 June 2023. In cl 4.1 and cl 4.2 of that Agreement, detailed obligations are imposed upon AOL in relation to the initial stages of the project.

110 Clause 4.3 regulates the ongoing management and harvest duties reposed in AOL (or the responsible entity of Project 4 from time to time).

111 Subclauses 4.3(a) to (d) provide as follows:

4.3 Ongoing management and harvesting duties