FEDERAL COURT OF AUSTRALIA

Spassked Pty Limited v Commissioner of Taxation [2003] FCAFC 282

INCOME TAX – appeal – deduction – interest on loan – group of numerous companies – holding company (Spassked) borrowed funds from finance company (IEF) within the group – Spassked, a large “dividend trap” and loss making company – Spassked incurred interest on borrowed funds – used borrowed funds to subscribe for shares in subsidiary (GIH) – GIH established with two classes of shares, “A” and “B” – “A” class, carrying right to franked and unfranked dividends, held by Spassked – “B” class, carrying right to franked dividends only, held by IEL – GIH invested profitably in various subsidiary companies – Spassked incurred tax losses as a result of interest expenses – Spassked transferred tax losses pursuant to s 80G of the Income Tax Assessment Act 1936 (Cth) to other members of the corporate group – whether interest an allowable deduction under s 51(1) of the Income Tax Assessment Act 1936 (Cth) – whether, in consequence, losses had been available to be transferred – whether subjective purpose in incurring expense relevant to determining deductibility under s 51(1) of the Income Tax Assessment Act 1936 (Cth) – whether an unfranked dividend can be converted into a franked dividend by the company receiving it voluntarily paying tax upon it – whether Spassked was carrying on business as a holding company – whether the requirement of IEL for unfranked dividends was taken into account by the Primary Judge – whether the argument that the profits in the Spassked structure were likely to exceed the compounded loan debt were a factor relevant and not taken into account by the Primary Judge – whether it should be held that Spassked borrowed finds with a view to gain by the receipt in the future of a dividend income – whether it should be held that the intention was that Spassked would cease to be a dividend trap in the future – whether the Primary Judge failed to take into account objective and relevant circumstances.

PRACTICE AND PROCEDURE – whether an appellate court should determine certain factual findings for itself where those findings would be contrary to findings of credit made by the Primary Judge who had the advantage of viewing the process of evidence giving.

COSTS – whether it is appropriate for the appellants to pay the whole sum of the costs of the appeal as well as the costs of the application before the Primary Judge where they are unsuccessful, but where the Primary Judge in the exercise of judicial discretion found that the appellants should only bear half the costs of the unsuccessful parts of the applications and none of a part of the applicant that the Primary Judge did not find it necessary to consider where the costs order was a disproportionate penalty for an error of the respondent.

Federal Court of Australia Act 1976 (Cth) s 27

Income Tax Assessment Act 1936 (Cth)s 51(1), s 80G(6)

AGC (Advances) Ltd v Federal Commissioner of Taxation (1975) 132 CLR 175 referred to

Amalgamated Zinc (de Bavcay’s Case) Ltd v Federal Commissioner of Taxation (1935) 54 CLR 295 referred to

Brookton Co-operative Society Ltd v Commissioner of Taxation (1981) 147 CLR 441 followed

Commissioner of Taxation v Consolidated Press Holdings Ltd (2001) 207 CLR 235 referred to

Federal Commissioner of Taxation v EA Marr & Sons (Sales) Ltd (1984) 2 FCR 326 distinguished

Federal Commissioner of Taxation v Smith (1981) 147 CLR 578 followed

Fletcher v Federal Commissioner of Taxation (1991) 173 CLR 1 followed

Fox v Percy (2003) 197 ALR 201 followed

Hart v Federal Commissioner of Taxation (2002) 189 ALR 584 approved

House v King (1950) 81 CLR 513 followed

Magna Alloys & Research Pty Ltd v Commissioner of Taxation (1980) 49 FLR 183 approved

Marra Developments Ltd v BW Rofe Pty Ltd [1977] 2 NSWLR 616 referred to

Queensland Wire Industries Pty Ltd v Broken Hill Proprietary Co Ltd (1987) 17 FCR 211 approved

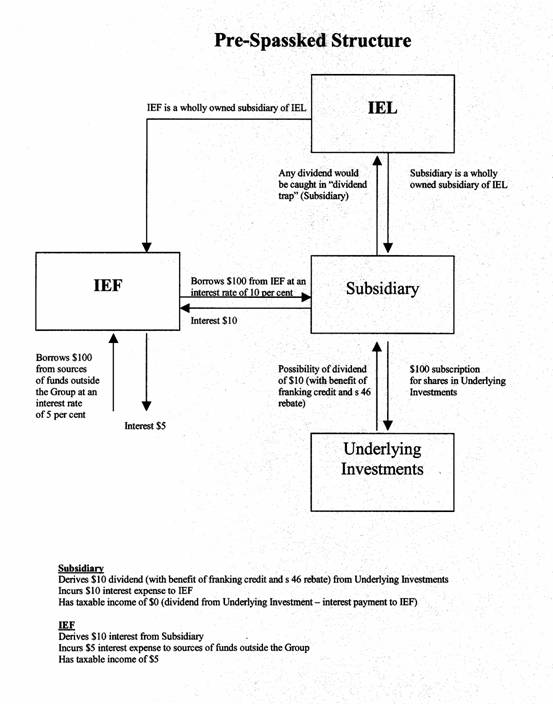

Re Minister for Immigration and Ethnic Affairs; Ex parte Lai Qin (1997) 186 CLR 622 distinguished

Ronpibon Tin NL & Tongkah Compund NL v Federal Commissioner of Taxation (1949) 78 CLR 47 applied

Service v Commissioner of Taxation (2000) 97 FCR 265 approved

STANLEY PARK LIMITED (ACN 008 432 997) v COMMISSIONER OF TAXATION

N 194 of 2003

INDUSTRIAL EQUITY LIMITED (ACN 004 617 164) v COMMISSIONER OF TAXATION

N 195 of 2003

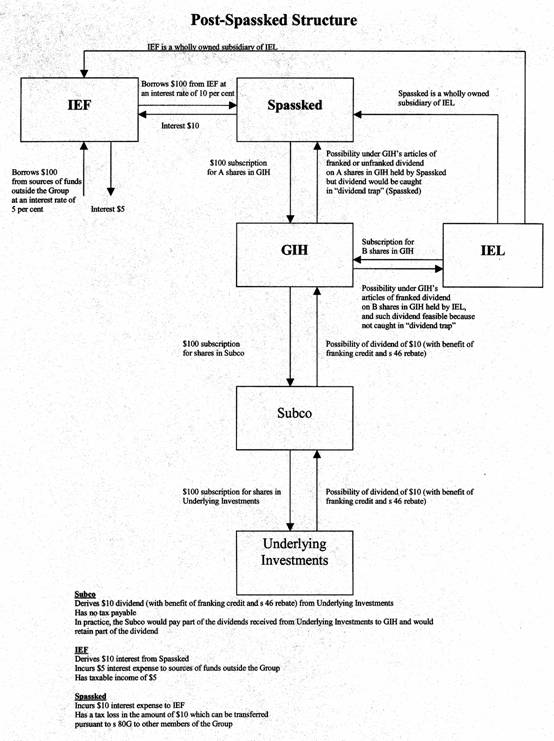

SPASSKED PTY LIMITED (ACN 003 255 847) v COMMISSIONER OF TAXATION

N 196 of 2003

HILL, GYLES & LANDER JJ

8 DECEMBER 2003

SYDNEY

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| NEW SOUTH WALES DISTRICT REGISTRY | N 194 OF 2003 |

ON APPEAL FROM A SINGLE JUDGE OF THE FEDERAL COURT OF AUSTRALIA

|

BETWEEN: |

STANLEY PARK LIMITED (ACN 008 432 997) APPELLANT CROSS RESPONDENT

|

| AND:

| COMMISSIONER OF TAXATION RESPONDENT CROSS APPELLANT

|

| HILL, GYLES & LANDER JJ | |

| DATE OF ORDER: | |

| WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

1. The appeal is dismissed.

2. The appellant pay the respondent Commissioner’s costs of the appeal.

3. The cross appeal is allowed in part.

4. Order 2 of the orders of the Primary Judge made on 21 March 2003 be set aside and in lieu thereof it be ordered that the appellant, Industrial Equity Limited and Spassked Pty Limited pay the respondent’s costs of the proceedings other than the costs of and incidental to the preparation of the second set of narratives which replaced SJM1 and the affidavit of Mr McClintock dated 13 March 2002.

5. The cross respondent pay the cross appellant’s costs of the cross appeal.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| NEW SOUTH WALES DISTRICT REGISTRY | N 195 OF 2003 |

ON APPEAL FROM A SINGLE JUDGE OF THE FEDERAL COURT OF AUSTRALIA

|

BETWEEN: |

INDUSTRIAL EQUITY LIMITED (ACN 004 617 164) APPELLANT CROSS RESPONDENT

|

| AND:

| COMMISSIONER OF TAXATION RESPONDENT CROSS APPELLANT

|

| JUDGES: | HILL, GYLES & LANDER JJ |

| DATE OF ORDER: | 8 DECEMBER 2003 |

| WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

- The appeal is dismissed.

- The appellant pay the respondent Commissioner’s costs of the appeal.

- The cross appeal is allowed in part.

- Order 2 of the orders of the Primary Judge made on 21 March 2003 be set aside and in lieu thereof it be ordered that the appellant, Spassked Pty Limited and Stanley Park Limited pay the respondent’s costs of the proceedings other than the costs of and incidental to the preparation of the second set of narratives which replaced SJM1 and the affidavit of Mr McClintock dated 13 March 2002.

- The cross respondent pay the cross appellant’s costs of the cross appeal.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| NEW SOUTH WALES DISTRICT REGISTRY | N 196 OF 2003 |

ON APPEAL FROM A SINGLE JUDGE OF THE FEDERAL COURT OF AUSTRALIA

|

BETWEEN: |

SPASSKED PTY LIMITED (ACN 003 255 847) APPELLANT CROSS RESPONDENT

|

| AND:

| COMMISSIONER OF TAXATION RESPONDENT CROSS APPELLANT

|

| JUDGE: | HILL, GYLES & LANDER JJ |

| DATE OF ORDER: | 8 DECEMBER 2003 |

| WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

- The appeal is dismissed.

- The appellant pay the respondent Commissioner’s costs of the appeal.

- The cross appeal is allowed in part.

- Order 2 of the orders of the Primary Judge made on 21 March 2003 be set aside and in lieu thereof it be ordered that the appellant, Industrial Equity Limited and Stanley Park Limited pay the respondent’s costs of the proceedings other than the costs of and incidental to the preparation of the second set of narratives which replaced SJM1 and the affidavit of Mr McClintock dated 13 March 2002.

- The cross respondent pay the cross appellant’s costs of the cross appeal.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| NEW SOUTH WALES DISTRICT REGISTRY | N 194 OF 2003 |

ON APPEAL FROM A SINGLE JUDGE OF THE FEDERAL COURT OF AUSTRALIA

| JUDGE: | HILL, GYLES & LANDER JJ |

| DATE: | |

| PLACE: | SYDNEY |

REASONS FOR JUDGMENT

HILL AND LANDER JJ

1 Before the Court are appeals by three appellants (‘the taxpayers’) from judgments of a Judge of this Court dismissing their applications being appeals against decisions of the respondent Commissioner of Taxation (‘the Commissioner’) disallowing their objections in respect of assessments of income tax made by the Commissioner in relation to the year of income ending 30 June 1992. The Commissioner appeals against so much of a separate judgment of the learned Primary Judge as related to the costs of the appeals. His Honour had ordered that the appellants pay only three quarters of the Commissioner’s costs of the appeals and the Commissioner in his cross appeals submits that the correct cost order should have been that the appellants pay all of the Commissioner’s costs.

2 Each of the taxpayers is a wholly owned subsidiary of Industrial Equity Ltd (‘IEL’), which is itself the applicant in proceeding N 1364 of 1999. They and many other companies, which are also wholly owned subsidiaries of IEL, had received assessments issued by the Commissioner in respect of the years of income commencing with the 1988 year and concluding with the 1994 year of income. In each case the Commissioner disallowed losses claimed to be available as an allowable deduction to the company in question, which losses had been the subject of notices given under s 80G(6) of the Income Tax Assessment Act 1936 (Cth) (‘the Act’) and which losses derived from what were claimed to be losses incurred by one of the appellants, Spassked Pty Ltd (‘Spassked’), in the years of income in question. Those losses arose, so it was claimed by virtue of interest incurred by Spassked in the years of income on amounts advanced to that company by Industrial Equity Finance Limited (‘IEF’). All appeals, therefore, depend upon whether in the years of income the interest incurred by Spassked was an allowable deduction under s 51(1) of the Act.

3 Section 51 (1) provides that there will be an allowable deduction for:

‘51(1) Deductions for losses and outgoings All losses and outgoings to the extent to which they are incurred in gaining or producing the assessable income, or are necessarily incurred in carrying on a business for the purpose of gaining or producing such income, shall be allowable deductions except to the extent to which they are losses or outgoings of capital, or of a capital, private or domestic nature, or are incurred in relation to the gaining or production of exempt income.’

4 The deductions involved in the three appeals before the Court total $932,667,411. The total of deductions claimed in the years of income 1988 to 1994 inclusive by the various companies in the IEL group, which deductions were disallowed by the Commissioner total $6,527,082,709. The present appeals will resolve not only the issues of deductibility which they raise of amounts disallowed to the three taxpayers which are the appellants in them, but also the deductibility of losses claimed by the other companies in the IEL group.

5 There were two alternative grounds upon which the Commissioner relied in disallowing to Spassked a deduction for the interest it incurred in the relevant years of income. The first was that the interest in question was not incurred by Spassked in gaining or producing the assessable income or necessarily incurred by it in carrying on a business for the purpose of gaining or producing the assessable income and hence was not deductible under s 51(1) of the Act. The second was that if the interest in question was otherwise an allowable deduction under s 51(1) of the Act, Part IVA of the Act (the general anti-avoidance provisions of the Act) operated to permit the Commissioner to disallow the deduction and assess accordingly. Because the learned Primary Judge was of the opinion that the interest incurred by Spassked was not an allowable deduction in each year of income his Honour did not find it necessary to consider whether, if the interest had been an allowable deduction to Spassked, the provisions of Part IVA of the Act would apply. Accordingly, if the appellants are successful in the appeals it will be necessary for the respective applications to be remitted to his Honour to consider the issues arising under Part IVA.

6 For convenience, we adopt the course taken by the learned Primary Judge of presenting these reasons as if the only relevant taxpayer whose appeal was before the Court was Spassked.

The background facts.

7 Prior to November 1989 IEL was a company the shares of which were quoted on the Australian Stock Exchange (‘ASX’). On or around 20 November 1989 ownership and control of the IEL group of companies passed to the Adelaide Steamship Company Ltd, David Jones Ltd and Tooth & Co Ltd, which companies can be collectively referred to as ‘the Adsteam Group’ as a result of the acquisition by Dextran Pty Ltd, a company owned by the Adsteam Group, of all the shares in IEL. That proved a financial disaster to the IEL group, a matter which was evident by as early as November 1990 when the Adsteam Group was experiencing difficulties in meeting its debt commitments. This resulted in a restructure of the financial and capital base of the IEL group and a borrowing over the financial years 1992 to 1997 by Dextran from IEL of a figure in excess of two billion dollars. Indeed, from around November 1990, the IEL Group was, as his Honour said ‘in de facto administration and there was little or no chance of its continuing as a going concern.’

8 However, the circumstances which led to Spassked incurring interest in the years of income to IEF arose much earlier when the IEL Group was still a publicly listed company and under the chairmanship of Mr, later Sir Ronald, Brierley (‘Brierley’) who, on the takeover by the Adsteam Group was replaced as chairman by Mr Spalvins.

9 IEL was what may be called a corporate raider. Its main activity seems to have been to acquire companies which generally, although not always, became wholly owned subsidiaries and then either to realise the assets of the companies acquired or sometimes to retain those assets. The acquisitions were generally made by companies which themselves were wholly owned subsidiaries of IEL and financed by borrowings from an in house finance company, although ultimately from external lenders and at an interest. IEF was such an in house financier. By the time IEL became a listed company in early 1974 there were almost 120 Australian or New Zealand companies which were part of the IEL group and through the operating subsidiaries IEL controlled what his Honour referred to as ‘a diverse range of operating businesses’. Half of the companies in the group were at that time inactive or were shelf companies that had been acquired so as to be available for future investments or acquisitions.

10 A consequence of the acquisitions was the existence of a large number of what the judgment appealed from refers to as ‘dividend traps’. To understand what is meant by that expression it is necessary to explain something of the then taxation system and the company law related to dividends.

DIVIDEND TRAPS, - dividend rebates, franking credits and the company law requirement of profits.

11 As the law stood at relevant times inter company dividends paid by resident Australian ‘public companies’ to shareholders which themselves were resident Australia ‘public companies’ were fully rebateable pursuant to s 46 of the Act. This meant that the dividend was included in the assessable income of the shareholder receiving the dividend, which then became entitled to a rebate of the tax payable on the dividend. However, before the tax payable on the dividend was calculated there was required to be deducted from the amount of the dividend derived amounts directly incurred in earning that dividend. If the shareholder deriving the dividend had incurred interest which was an allowable deduction to it because the amount borrowed had been used to acquire the shares on which the dividends were paid the interest had to be deducted from the dividend before the rebate was calculated. Where the interest incurred was equal to or exceeded the dividend the result was that there was no taxable income upon which tax could be calculated and no tax payable on the dividend which could be rebated. The amount of the rebate allowable was to be no greater than the tax payable on the dividend. The consequence was that the inter company dividend rebate was lost to the shareholder.

12 Dividend imputation was introduced in Australia applicable in the tax year ending 30 June 1988 to alleviate what was seen to be the double tax payable as a result of the classic system of taxation of companies and their shareholders. In the classic system the company pays tax on its taxable income and shareholders pay, additionally, tax on dividends they derive. Full dividend imputation would have the consequence that the shareholder being a resident individual receiving a dividend out of profits already subjected to tax in the hands of the company would effectively receive a credit of the tax payable by the company and thus suffer no additional income tax on the dividend provided that the rates of tax payable by companies and shareholders were aligned. In fact Australia does not have that alignment and the system adopted has been, except for a short period, largely only a system of partial and not full imputation.

13 Under the system adopted in Australia a dividend may be wholly or partially franked or unfranked depending upon whether it was paid wholly or only partially out of profits which had born tax in the hands of the company. If the dividend was paid wholly out of profits which had born tax in the hands of the company the shareholder received a credit for the tax paid by the company. The dividend was referred to as a franked dividend. The value of this credit (referred to as a ‘franking credit’) was added to the cash dividend (ie there was to be a ‘gross-up’ of the dividend and the amount of the franking credit) and the resulting figure was included in the taxable income of the shareholder. The shareholder then received a credit for the tax paid by the company. As the learned Primary Judge observed a shareholder being an individual would generally prefer to receive a franked dividend. Where the shareholder was a company the benefit of the franked dividend and thus the franking credit could be passed up through a line of companies through to the parent company and thence directly or indirectly through to an individual shareholder.

14 It is relevant, also, to understand the system in operation in the relevant taxation years which allowed a company which incurred a loss in a year of income to transfer that loss to a company within a wholly owned group of companies which had income against which the loss could be offset. A company which had borrowed money at interest to acquire shares would ordinarily obtain a deduction for the interest it incurred in the year of income under s 51(1) of the Act. If the company had, in the year of income, no income against which the interest deduction could be offset the company would have incurred a loss in the year of income. Accordingly that loss could be transferred to a group company which then had an allowable deduction to offset the assessable income it derived in that year. However, if the company which incurred the interest were to derive a dividend, then to the extent that the dividend equalled or exceeded the interest (there being no other income or deductions) there was no loss in the company and accordingly no loss which was available to be transferred to a company in the group.

15 To the tax disadvantages which would accrue to the group of companies where a company in the group both incurred interest and also derived dividends there was a company law problem created. It was at all relevant times the law that a dividend was only lawful if paid out of profits (see, s 565 of the Companies Code, s 201 of its successor the Corporations Law and now s 254T of the Corporations Act 2002 (Cth)). What constituted profits was a matter to be determined by reference to accounting evidence and commercial principles. If in a year a company both incurred interest and derived a dividend the interest would need to be deducted from the amount of the dividend to determine whether there was a company law profit. Thus if the interest equalled or exceeded the dividend a company deriving a dividend would not be able to pay a dividend because it would have no profits in the year. If the dividend in question was franked, and the company which derived it could not pay a dividend to shareholders because there were no profits the benefit of the franking credit was lost.

16 However, there was a doctrine of company law that past years’ losses were not required by law to be made good before it could be said that a company had a profit out of which it could pay a dividend. Thus a company with accumulated losses which received a dividend in the current year and which did not incur interest equal to or greater than the amount of the dividend might declare a dividend: Ammonia Soda Co Ltd v Chamberlain [1918] 1 Ch 266; Marra Developments Ltd v BW Rofe Pty Ltd [1977] 2 NSWLR 616 at 630. Of course, for company law purposes, a group company to whom losses were transferred for taxation purposes was not required to take those losses into account when determining whether it could pay a dividend out of profits. A company with company law profits but tax law losses, could thus as a matter of company law declare and pay dividends to its shareholders.

17 In summary, the use of a corporate structure whereby a company borrowed at interest to acquire dividend producing shares brought about a result that there would be a loss of the intercorporate tax rebate. In the result there could be no loss in the company available to be transferred to a group company because the interest deduction would be offset by the dividend received, to the extent that the dividend it received was franked the company would have no ability to declare a dividend so as to pass the benefit of the franking credit through intermediate companies to an individual shareholder because it had no company law profits absent other income.

18 Prior to the adoption of what is referred to as the Spassked structure in the latter half of 1987 there was a large number of individual dividend traps within the IEL Group, that is to say there was a large number of corporate taxpayers which had incurred interest to acquire shares in a company which became a subsidiary and which, if dividends were declared to it by the subsidiary would result in the loss of the s 46 rebate: the inability to transfer to other group companies a loss which would be brought about if no dividend were derived and which did not have profits out of which it could pay franked dividends to its immediate shareholder.

19 The problem was described by Mr Daniels, a management accountant employed by IEL in his affidavit evidence read in the proceedings in the following terms:

‘…I had been involved in the flow of dividends up through the IEL group for a number of years. I also knew that the structure of the IEL group at that time did not readily support the flow of dividends up to IEL, even though IEL was still able to pay dividends. In any given year for instance, a number of IEL group companies inevitably made accounting losses. Typically, these companies were the intermediate holding companies of other IEL group subsidiaries that were profitable and able to pay dividends. This usually occurred because the holding company had borrowed to acquire equity in [or lend money to] the subsidiary. In turn, the subsidiary would use the [funds] raised to acquire income-producing assets. This left the parent company with a loss represented by interest on the borrowings. In consequence, the holding company’s financial statements or accounts, usually showed the holding company as having a net asset deficiency. This meant it had no fund of profits available from which to declare a dividend. This led to a multiplicity of ‘dividend traps’, as I called them, across the IEL group. This occurred because a dividend paid to a loss making parent company by a profitable subsidiary, could not be passed on to shareholders, until such time as it had a fund of distributable profits available.

If dividends received by a loss making holding company were fully or partially franked, any franking credits associated with them would also be trapped within the loss making entity. It was part of … my role to minimise the incidence of such dividend traps, so that dividends, franked and unfranked, could be passed up to IEL to enable it to meet expenses and pay dividends. This was increasingly difficult to achieve with the complexity of the IEL group at the time.’

A DIAGRAMMATICAL VIEW OF THE PRE-SPASSKED STRUCTURE.

20 Attached to this judgment as Annexure A is a diagram which was annexed to the judgment appealed from. The diagram represents in simplified form the structure that existed before the rearrangement which effected what is referred to as the ‘post-Spassked structure’. It is simplified in that the company referred to as ‘subsidiary’ may have been owned not directly by IEL but by a company directly or indirectly wholly owned by IEL. The diagram suggests that the financier, IEF borrowed at a rate of interest being 5% and on lent to the subsidiary at a rate of interest of 10%. The evidence was, however, that IEF made only a small margin on the borrowing and lending transaction. Finally, it should be noted that the diagram merely shows one dividend trap when the evidence was that prior to the reorganisation that were many such structures within the IEL group of companies. The diagram is nevertheless useful as representing in general terms the pre-Spassked structure.

THE POST-SPASSKED STRUCTURE.

21 By the mid to late 1970’s IEL had become almost entirely reliant upon receiving dividends from its subsidiaries to fund dividends which it might wish to declare to its shareholders. From around the mid 1980’s Mr Daniels met with a chartered accountant employed by IEL, Mr Latham and a partner in the group’s external auditors twice a year, usually in May and in November/December to review trial balances of companies in the group and to decide upon what dividend recommendations should be made to the board of IEL.

22 Mr Daniels formed the view in around 1986 or early 1987 that there was a need to restructure the IEL group. He was of the view, he said, that it was becoming difficult to keep track of which company had made investments and also to manage the group’s investment portfolio. He felt there was a need to simplify the equity and more particularly the ‘debt lines’ between companies in the group. There had been a dramatic growth of the group between 1974 and 1987 as a result of which the complexity of the group structure had grown. One of the main reasons for the complexity of the IEL group structure and of the debt lines was attributable to the fact that acquisitions were often of companies which themselves had a complex structure of holding company, intermediate subsidiary and operating subsidiary. A separate IEL company was usually used as the purchaser of the shares in that group. Once companies became members of the IEL group there was a need for debt and equity finance to be provided from within the group. His Honour accepted that the debt and equity lines were, as Mr Daniels said, ‘complex’.

23 IEF had been established as the in house financier of the group in the mid 1980’s.

24 The imminent introduction of the imputation system precipitated detailed discussion at administration team meetings. Mr Daniels perceived a need to review the existing structure so as to facilitate the payment of franked dividends to such shareholders as wished to receive franked dividends. It can be accepted that there was a need generally to ensure that dividends, franked or unfranked could be paid as required. Indeed, in early 1987 IEL announced to its shareholders its intention to pay franked dividends to such shareholders who wanted them.

25 The Spassked re-organisation arose out of discussions among Mr Daniels, Mr Latham, a Mr Cottam and the then chief executive officer of IEL, a Mr Price. Among others there was consultation with the external auditors. The proposal was described by Mr Daniels as follows:

‘The Spassked Proposal involved the following elements:

(a) Spassked (a wholly owned shelf company of IEL of which Mr Price, Dr Weiss [Dr Weiss was corporate counsel for the Group and a member of its Investment Team] and I were directors), would borrow funds from IEF (of which Mr Price, Dr Weiss and I, were also directors), at a commercial rate of interest, which was to be capitalised (by which I mean that the interest expenses that would be incurred by Spassked on its loans from IEF would be added to the principal and from that time also be subject to interest which would occur by crediting the interest income in the books of IEF, and debiting the interest expense in the books of Spassked);

(b) Spassked would use the funds borrowed from IEF to subscribe for ‘A’ class shares that would be issued by GIH (known, until 12 November 1988 as Bikinga Pty Limited, which was a wholly owned shelf subsidiary of Spassked, of which Mr Price, Dr Weiss and I, were directors). The articles of association of GIH would be changed so that it could allot ‘A’ class shares that would carry the right to both franked and unfranked dividends, and ‘B’ class shares that carried the right to franked dividends only;

(c) IEL would subscribe for ‘B’ class shares in GIH, entitling IEL to franked dividends only;

(d) GIH would use the subscription moneys received from Spassked and IEL to acquire shares in either:

(i) shelf companies or entities already held by the IEL group, or newly incorporated shelf companies; or

(ii) IEL group companies with existing assets, by subscription or purchase, that were expected to produce a franked dividend stream;

(e) Those companies referred to in subparagraph (d)(i) above would deposit their funds with IEF at interest, until such time as the funds were required for a specific offer, acquisition or investment. For those companies referred to in sub-paragraph (d)(ii), the funds would be applied to existing inter-company debt, and to the extent that there was a surplus of funds, this would be deposited with IEF at interest.’

26 His Honour observed that in cross examination Mr Daniels agreed that an additional element of the Spassked proposal was that Spassked, not having any dividends to offset the interest incurred by it would incur a loss in the year of income which it could transfer to other members of the Group.

A DIAGRAM OF THE POST-SPASSKED STRUCTURE.

27 Annexed marked B is a diagram which, in simplified form sets out the structure which emerged as a result of the Spassked proposal. The diagram was likewise Annexure B to the judgment appealed from. As was the case with the diagram Annexure A this diagram shows IEF borrowing at an interest rate of 5% and on lending to Spassked at 10%. The evidence was that only a small profit margin arose between the rate of borrowing and the rate of lending.

28 The company ‘Subco’ shown in that diagram would, it was expected, be used to purchase future investments, so that companies acquired would become direct subsidiaries of that company.

THE IMPLEMENTATION OF THE SPASSKED STRUCTURE

29 The Spassked structure was implemented in a series of meeting and transactions over a period of time commencing on 30 December 1987 and concluding on 29 June 1990. The steps taken followed meetings at which Mr Daniels attended but of which no records were kept. The meetings concerned the amounts which Spassked was to borrow from IEF and invest in GIH and the amounts which GIH in turn would use to capitalise various Subcos in return for shares in them. This was in accord with the practice which prevailed in the administration of IEL. No minutes were made of meetings and indeed Mr Daniels described the meetings as ‘informal get togethers and an opportunity to discuss investments and issues associated with investments.’

30 The steps taken were described by the learned Primary Judge as follows at [95] to [104]:

‘95. On or about 30 December 1987 Daniels and Dr Gary Hilton Weiss (‘Weiss’), who was corporate counsel for the Group, a member of the Investment Team, and, like Daniels, a director of IEF, Spassked and GIH, agreed that:

o IEF would lend $25,000,000 to Spassked at the commercial rate of interest then being used within the Group for loans by IEF;

o Spassked would deposit a cheque for that amount into GIH’s bank account later the same day;

o in return, GIH would issue ‘A’ shares to Spassked to the same value;

o GIH would invest the funds received from Spassked in certain identified Subcos.

96. On 18 January 1988 Daniels attended a meeting of the members of GIH in his capacity as a director of GIH. Weiss was also present as chairman of the meeting and as the duly appointed representative of Spassked. It was resolved that GIH’s articles of association be amended, and that $100,000,000 ordinary shares in the capital of GIH be converted to 50,000,000 ‘A’ shares and 50,000,000 ‘B’ shares. The amendments to the articles defined the rights of the two classes of shares as described at [40] earlier. A sum of $25,000,000 had been transferred from IEF to Spassked and from Spassked to GIH on 30 December 1987. On 30 December 1987 GIH issued ‘A’ shares to that value to Spassked (this issue was initially recorded in the accounts of GIH as having taken place on 28 January 1988, however, subsequent records of both GIH and Spassked indicate it took place on 30 December 1987). On 30 December 1987 GIH used the $25,000,000 to subscribe for shares in Harbour Securities Pty Ltd, which, in turn, used $7,322,671.77 of that amount to repay a debt it owed to IEF and placed the balance of $17,677,328.23 on deposit with IEF at interest.

97. Also on 18 January 1988 IEF lent Spassked $950,000,000 with which it subscribed for ‘A’ shares in GIH. GIH used that amount to capitalise twelve Subcos on that date.

98. The two amounts ($25,000,000 and $950,000,000) deployed in the capitalisations on 30 December 1987 and 18 January 1988 represented just over 27 per cent of the total sum of $3,531,392,233 which Cottam said in his affidavit was similarly invested by GIH in Subcos during the period 30 December 1987 to 30 June 1992 (see [111] below).

99. On 2 February 1988 IEL subscribed $150,000,000 for ‘B’ shares in GIH. On that day, that amount was debited to IEL’s bank account and credited to GIH’s. In cross-examination, Daniels said that the amount of $150,000,000 was arrived at as the amount of share capital thought necessary to support that stream of franked dividends which it was estimated IEL would need to meet its shareholders’ expectations. This transaction of 2 February 1988 differs from the other ten, all of which commence with IEF lending to Spassked, because IEL did not borrow the sum of $150,000,000 from IEF, and, of course, payment of that sum to GIH resulted in the issue of ‘B’ shares to IEL rather than ‘A’ shares to Spassked. GIH placed the sum of $150,000,000 paid to it by IEL for the ‘B’ shares on deposit with IEF.

100. In order to effect the Spassked Restructuring, amounts were lent by IEF to Spassked as follows:

|

Tranche No. | Date | Amount | Manner of tranche

|

| 1 | 30 December 1987 | $25M | Cheque/bank transfer |

| 2 | 18 January 1988 | $950m | Cheque/bank transfer |

| 3 | 31 March 1988 | $675m | Cheque/bank transfer |

| 4 | 1 April 1988 | $280m | Journal entries only |

| 5 | 15 March 1989 | $400m | Promissory note |

| 6 | 30 March 1989 | $7,351,681 | Promissory note |

| 7 | 31 May 1989 | $999,791,187 | Journal entries only ($55m) Promissory note ($944,791,187) |

| 8 | 15 March 1990 | $99,999,998 | Promissory note |

| 9 | 19 March 1990 | $145m | Promissory note |

| 10 | 28 June 1990 | $155m | Promissory note |

| | Total | $3,737,142,866 | |

101. In addition, on or about 31 July 1989 IEF lent Spassked $25,613,377 at interest to be applied by Spassked in eliminating a foreign exchange loss it had sustained.

102. Spassked used the above total of $3,737,142,866, as to $3,457,142,866 in subscribing for ‘A’ shares in GIH, and as to the balance of $280,000,000 as an interest free loan to GIH.

103..By 30 June 1990 as a result of the ten transactions and the additional borrowing of $25,613,377 referred to in [101] above, Spassked had borrowed from IEF a total of $3,762,756,243. On 13 March 1989 Spassked paid $280,000,000 to IEF, reducing its indebtedness to IEF as at that time to $1,650,000,000 (excluding capitalised interest).

104. With the following exceptions, all of the funds lent by IEF to Spassked were invested in ‘A’ shares in GIH and were, for the most part, invested by GIH in Subcos: first, the $280,000,000 constituting tranche 4 was lent by Spassked interest free to GIH and invested by it in two Subcos; and, secondly, of the funds in tranche 7, $55,000,000 was used by Spassked to pay a debt it owed to GIH. (Again, there was also the special purpose loan of $25,613,377 referred to in [101] above.)’

31 His Honour notes that the amounts of capitalised interest incurred by Spassked to IEF and the respective amounts distributable and distributed by GIH to Spassked by way of dividends were as follows:

|

Year

|

Interest |

Distributable |

Distributed |

| 1988 | $113,184,429 | $98,625,459 | Nil |

| 1989 | 406,405,066 | 304,868,025 | Nil |

| 1990 | 1,064,892,295 | 901,363,305 | 29,308,093 |

| 1991 | 1,839,638,821 | 1,338,749,042 | 29,308,093 |

| 1992 | 2,727,804,345 | 1,729,279,541 | 43,962,139 |

| 1993 | 3,193,431,043 | 2,108,727,039 | 43,962,139 |

| 1994 | 3,272,715,111 | 3,045,199,551 | 43,962,139 |

32 His Honour summarised other relevant financial information as follows:

‘108. The rates of interest charged by IEF to Spassked were set by the Treasury group within IEL, and were, to the best of Daniels’ recollection, ‘akin to the prevailing market rates, such as the three year swap rate’. From about 1991 IEF added a component to reflect ‘line fees and other borrowing costs, plus a small margin to ensure that IEF would make a small profit on the loans’.

109. As noted earlier, Spassked repaid its indebtedness to IEF, including capitalised interest, in 1994. It used for the purpose money it borrowed interest free from GIH and, as to a small amount, from IEL.

110. The interest expenses Spassked incurred to IEF, the dividends Spassked received from GIH, and Spassked’s claimed losses for the 1988 to 1994 years are as follows:

|

Year

|

Interest expenses to IEF |

Unfranked dividends received from GIH |

Spassked’s losses (per income tax returns)

|

| 1988 | $113,184,429 | | $113,185,387 |

| 1989 | 293,220,637 | | 293,220,691 |

| 1990 | 658,487,229 | $29,308,093 | 654,610,528 |

| 1991 | 774,746,526 | | 774,746,571 |

| 1992 | 888,165,526 | 14,654,046 | 873,693,604 |

| 1993 | 465,626,741 | | 465,626,785 |

| 1994 | 79,284,023 | | 79,284,032 |

| Total | $3,272,715,111 | $43,962,139 | $3,254,367,598 |

The above table shows that the amounts of Spassked’s claimed losses were generally in line with the amounts of the interest expenses it incurred to IEF.

Investment by Subcos

111. During the period 30 December 1987 to 28 June 1990, GIH used funds received from Spassked to invest in Subcos, …. According to Cottam’s affidavit, the total consideration paid by GIH for shares in the Subcos was $3,531,392,233. But an addition of the amounts of ‘total consideration’ shown in the annexure to these reasons gives a total of $3,531,314,466 – a difference of $77,767. The difference is immaterial. In the interests of consistency I will use Cottam’s figure of $3,531,392,233. In that period GIH also lent to companies in the Group.

112. The Subcos used the funds invested in them by GIH to invest in a wide range of well known public companies, including, for example, Woolworths Ltd (‘Woolworths’), Southern Farmers Group Ltd, Pioneer International Ltd, Kern Corporation, Queensland Trading and Holding Company, Bell Resources Ltd, St George Building Society, Minoil Securities Ltd, Bundaberg Sugar Company, Carringbush Corporation, Rothmans Holdings Ltd and Rothmans of Pall Mall, Caltex Ltd and Sagasco Ltd. The shares were acquired as a result of subscription or transfer upon purchase.’

33 The initial investments made by GIH on 18 January 1988 were all in shares in companies capable of paying franked dividends. This was in accord with Mr Daniels’s original thinking to restrict the structure to shares which were capable of declaring franked dividends. However, Mr Daniels said in his evidence that he changed his mind in 1988 or 1989 and thereafter most of the group’s companies became part of the Spassked/GIH sub group whether or not they were capable of generating franked dividends.

34 It may be noted that Spassked only ever received two unfranked dividends totalling $43,962,139 from GIH.

THE ADSTEAM TAKEOVER AND ITS CONSEQUENCES.

35 By November 1990 the Adsteam Group was in dire straights. Mr Daniels was of the view that the group had no future and that it would probably be put into liquidation and the proceeds of assets would be used to pay external creditors and the shareholders of Dextran, that is to say the Adsteam Group companies.

36 The bankers to Adsteam ultimately agreed to an informal and temporary moratorium on debt and interest payments to permit time to develop a plan for a progressive realisation of assets. On 20 December 1991 Spassked and IEF entered into a deed by which Spassked acknowledged that it owed IEF $5,322,395,000 and undertook thereafter to pay interest at the Bank bill rate as defined plus 9 per cent per annum or so lesser rate as the parties might agree. In fact the interest rate peaked in 1991 at 17.25 per cent.

37 Assets were progressively sold off, including the sale of Woolworths in 1994 for $2,450,000,000 and the proceeds of assets sales were used to repay the external debt of the group or passed up to IEL by way of loans. External debt was repaid in full by July 1993. As part of that process Spassked’s debt to IEF was repaid by 1 July 1994 and thereafter Spassked ceased to incur interest to IEF.

38 However, by 30 June 2000 assessments of income tax had been received by various IEL group companies totalling $2,176,000,000 that sum comprising primary tax in the order of $1.148 billion and additional tax, penalties and interest in the order of $1.028 billion. It can be accepted that thereafter the possibility of companies in the IEL group paying dividends was fraught with danger as potentially the declaration of a dividend would involve an illegal reduction of capital, insolvent trading or the commission of an offence under the Crimes (Taxation Offences) Act 1980 (Cth). A considerable amount of correspondence with the Australian Taxation Office did not lead to any resolution of the taxation disputes in which the IEL group had become enmeshed.

THE JUDGMENT APPEALED FROM.

39 His Honour delivered a careful and detailed judgment. The summary here set out necessarily omits much of the detail contained in the judgment.

40 There is a detailed discussion of the evidence that was given by Mr Daniels, Mr Cottam and Sir Ronald Brierley. Much of that evidence was not controversial. However, there was an important factual question which the learned Primary Judge was required to resolve, namely, whether at some time after the implementation of the Spassked structure it was intended that dividends would be declared in favour of Spassked. We will return to that evidence later.

41 The learned Primary Judge then discussed a number of cases. He concluded that the question whether interest incurred by a taxpayer was incurred in gaining or producing assessable income was ordinary to be determined by looking at the objective circumstances. What was involved was a question of characterisation. Reference was made to the judgment of the High Court in Ronpibon Tin NL & Tongkah Compund NL v Federal Commissioner of Taxation (1949) 78 CLR 47 where the Court said at 57:

‘… to come within the initial part of the sub-section [‘losses or outgoings ... incurred in gaining or producing ... assessable income’] it is both sufficient and necessary that the occasion of the loss or outgoing should be found in whatever is productive of the assessable income or, if none be produced, would be expected to produce assessable income.’

42 The reference in that passage to ‘expectation’, linked as it was to the occasion of the outgoing signified, his Honour said, that ‘the voluntary incurring of a loss or outgoing must be seen to be explicable by the taxpayer’s favourably looking forward to’ the gaining or producing of assessable income as a result, or must be seen to be ‘for’, or ‘for the purpose of’, or ‘directed to’ the gaining or producing of such income.’ The word ‘expectation’ was not, his Honour said, to be understood in the mere neutral factual sense.

43 However, the Commissioner had submitted that it was necessary in the present case to look at the subjective purposes of the taxpayer, through its officers and once this was done it could be seen, or so it was submitted, that the Spassked structure, and the loans which were entered into by Spassked as a result of its implementation, were designed to eliminate the dividend traps and to obtain deductions for losses to be transferred to the many companies in the IEL group. So, it was said, the interest was not incurred for the purpose of gaining or producing assessable income but for other purposes such as reducing income tax.

44 His Honour, while preferring to consider the question by reference to objective factors said that this did not mean that subjective expectation or purpose was irrelevant to the identification of the purpose which characterised the incurrence of the loss or outgoing. His Honour found ‘that there was no agreed plan, mechanism or time frame, according to which Spassked would cease to be a dividend trap, cease to be a repository of losses, and begin to receive dividends from GIH’. Further his Honour found that the receipt by Spassked of dividends from GIH formed no part of the motivation, subjective purpose or impetus behind the Spassked restructuring. His Honour did not find the testimony of either Mr Daniels or Mr Cottam persuasive. His Honour said that he was not satisfied that Mr Daniels himself expected that Spassked would cease to accrue interest to IEF and commence to receive dividends. His Honour said that it was his view that Mr Daniels had not given more than a fleeting consideration to the likely duration of the Spassked structure as his hope was that it would continue to be used so long as it was useful and no change of circumstances required it to be abandoned.

45 His Honour said that Mr Cottam’s evidence was ‘generally unsatisfactory’ on this issue.

46 In reaching the conclusion that the interest received was not incurred in gaining assessable income his Honour took into account a number of matters which his Honour referred to as ‘Particular Circumstances’. One in particular was the subject of criticism by counsel for the appellants as being wrong in law. We shall return to that matter later. Because the significance of this subparagraph assumed importance during argument it is useful to set out here all the matters mentioned by his Honour so that the significance of the subparagraph to his Honour’s conclusion can be appreciated:

‘Particular circumstances

The circumstances described in the numbered paragraphs below have varying degrees of relevance to the factual questions:

o whether the interest expense was incurred by Spassked, that is, whether Spassked’s course of borrowing at interest from IEF was engaged in by Spassked, in gaining or producing assessable income in the form of dividends from GIH; and

o whether the interest expense was necessarily incurred, that is, whether Spassked’s course of borrowing at interest from IEF was necessarily engaged in, in Spassked’s carrying on a business for the purpose of gaining or producing assessable income in the form of dividends from GIH.

1. The terms of the borrowings were not reduced to writing and were not recorded in the minutes of meetings of the boards of directors of borrower or lender. Such contemporaneous records as exist are, generally speaking, only records of movements of money.

2. The directors of Spassked, being also the directors of IEF, GIH and most of the Subcos (though not of IEL):

o were in a position, and, I am satisfied, intended, to act in what they perceived to be the interests of the Group as a whole, rather than the specific interests of one or more of the companies of which they were directors; and

o in their capacity as directors of Spassked, borrowed knowing what was to be the destination and use of the money borrowed as well, at least in a general sense, as the destination and use of any income which the deployment of that money would generate, that is, of any dividends the Subcos would receive from the underlying investments.

3. As noted earlier, since there was no agreed term of any of the ten loans from IEF to Spassked, by implication, they were repayable in full upon demand by IEF, whether with or without the prior giving of reasonable notice. But, again, repayment would not be required unless for some reason this was seen to be in the interests of the Group as a whole.

4. So long as Spassked was incurring an interest liability to IEF or had undistributed losses, it would not receive dividends from GIH.

5. As Daniels acknowledged, in view of (4) above, and the fact that Spassked’s ‘A’ shares in GIH were its only investments, so long as that situation continued, Spassked would not have the necessary income with which to pay the interest accruing on its borrowings from IEF, which therefore would have to be capitalised. Spassked could therefore be expected to make a loss each year of the order of the amount of the capitalised interest for that year. Except to the extent the losses were transferred by Spassked to other members of the Group, they would accumulate in Spassked.

6. The streaming up of dividends to IEL could not occur through Spassked while Spassked remained a dividend trap, but it could occur directly through GIH, by reason of IEL’s holding of ‘B’ shares in GIH. In fact, in the period 1988 to 1994, $33,378,828 (in franked dividends, representing the total amount of franked dividends received by GIH during that period from the Subcos) was streamed up to IEL in this way.

7. GIH used the funds received from Spassked (and the $150,000,000 subscribed by IEL for ‘B’ shares in GIH) in subscribing for shares in the Subcos which were:

(a) shelf companies; and

(b) already capitalised companies within the Group,

in most cases, the latter.

8. Money paid by GIH to a Subco would be applied by the Subco, first, in discharging any interest bearing debts it owed to companies in the Group, in particular, to IEF. This had the effect, as Daniels acknowledged it was intended to do, of enabling the Subco:

o to stream up to GIH, free of any dividend trap problem, any dividends the Subco received from its underlying investments; and

o to enjoy the full s 46 rebate in respect of dividends it received.

9. (a)Shelf companies referred to in 7(a) above would deposit with IEF at interest the funds they received from GIH, until those funds were required, if they were required at all, to enable the shelf company to make a specific investment.

(b)The already capitalised companies within the Group referred to in 7(b) above would deposit with IEF, at interest, any surplus funds received from GIH remaining after their intercompany debt was paid off as described in (8) above.

10. Daniels agreed that it was an element of the Spassked Structure that ‘at least in [the] early years’ Spassked would be incurring losses because it would be incurring interest to IEF and would not be receiving income with which to pay that interest, and that Spassked would transfer the resulting losses to other members of the Group.

11. Daniels said that ‘the major’reasons for adopting the Spassked Structure in preference to other structures that were considered were that:

o it enabled franked dividends to be streamed up to IEL without being subsumed in a dividend trap;

o it enabled unfranked dividends to be streamed up to GIH without being subsumed in a dividend trap; and

o it enabled maximisation of the amounts of losses available to be transferred to members of the Group.

12. Daniels said that there were three other reasons which were not ‘critical’, and which would not themselves have led to the Spassked Restructuring, but which were considered ‘as part of the structure’. They were that:

o pre-capitalised shelf companies would be readily available as and when required, through which acquisitions or other investments could be made;

o the Group would be rid of ‘pockets of non-wholly owned companies’ and any associated problem for ‘grouping for section 80 purposes’;

o the possibility would be opened up that ‘the company owning an asset [might] be sold in lieu of the asset which may yield a higher cost base for tax purposes’.

Daniels agreed that as events transpired, generally, advantage was not taken of the first and third of these matters, that is, most of the shelf companies capitalised by GIH in January 1988 were not in fact used to acquire external assets, and in all cases underlying assets were sold rather than the companies owing them.

13. Importantly, neither Daniels nor Cottam suggested that the derivation of dividend income from GIH formed any part of the motivation behind the Spassked Restructuring: rather, Spassked’s case is that it was expected as a matter of neutral fact that at some time in the future dividends would begin to flow to it from GIH. As I have indicated earlier, in my opinion this is not sufficient to bring a loss or outgoing within subs 51(1).

14. Progressively down to 1998, Spassked transferred out to members of the Group all of its tax losses amounting to some $3.2 billion to be applied against their otherwise taxable incomes, that is to say, income against the tax on which no rebate under s 46 of the Act was to be applied. Daniels agreed that ‘the reason for making the losses …, for transferring the losses [pursuant to s 80G of the Act], was to reduce the amount of tax that the other members of the group would otherwise have had to pay.’

15. It was to be expected and was in fact expected, by Spassked’s directors, that the Subcos would receive substantial dividend income from the underlying investments. Over the 1988-1994 financial years, the Subcos received approximately $83.4 million of franked dividends and approximately $1.454 billion of unfranked dividends. Because the Subcos had been rendered clear of debts and associated interest liabilities, those dividends were not subsumed in dividend traps at the Subco level. What happened to those funds? As previously noted, GIH paid to IEL franked dividends totalling $33,378,828 (the amount of franked dividends GIH itself had received from the Subcos), and to Spassked the two unfranked dividends totalling $43,962,139 previously mentioned. This left GIH holding a balance of $182,749,388 of unfranked dividends it had received from the Subcos available for streaming up to Spassked, but not in fact streamed up to it. But perhaps more significantly, the Subcos were left holding some $50 million of franked dividends and some $1.227 billion of unfranked dividends which, so far as GIH’s articles of association were concerned, could have been streamed up to GIH and thence to Spassked and (in the case of franked dividends only) to IEL. There would be no streaming up of dividends to Spassked so long as it was a dividend trap and still had transferable losses. In relation to the latter, the Commissioner submits as follows:

“The importance to the IEL group of maximising the tax losses is illustrated by the impact of the losses on the total taxation position of the members of the group. In the year of income ended 30 June 1991 the total taxable income of the IEL group was $1,309,955,903.00 (before the transfer of losses), $162,665,425.00 of which represented rebateable dividends … After allowing for the rebateable dividends, the resulting total taxable income was $1,147,685,524.00. This figure was reduced to $5,460,747.00 by the transfer of tax losses in the sum of $1,142,224,777.00. Spassked’s contribution to these losses was $642,273,167.00. In the year of income ended 30 June 1992, the total taxable income of the IEL group (before the transfer of losses) was $4,045,564,415.00, $2,860,074,321.00 of which represented rebateable dividends. After allowing for the rebateable dividends, the resulting total taxable income was $1,181,494,467.00. This figure was reduced to $699,872.00 by the transfer of tax losses of $1,180,794,595. Spassked’s contribution to the transfer of losses was $800,415,065.00. In the year of income ended 30 June 1993, the total taxable income of the IEL group (before the transfer of losses) was $676,949,195. After allowing for the rateable dividends, the resulting total taxable income was $430,708,195. This figure was reduced to nil by the transfer of tax losses. Spassked’s contribution to the transfer of losses was $200,917,810 ...”

Daniels, said of Spassked’s ceasing to be a dividend trap and a repository of losses, “the two go together. It cease[s] to be a dividend trap. It ceases to be a borrower. It ceases to have interest deductions.”

16. It was the Administration Team and the tax division within the Group (in particular, Daniels and Latham), not the Investment Team, which perceived a restructuring of the Group to be desirable and initiated exploration of the question.

17. Similarly, while Price approved of the Spassked Structure, it was the Administration Team (notably Latham and Cottam), not the Investment Team, which determined the timing and amounts of the transactions by which the Spassked Structure was implemented.

18. Nonetheless, there was a ‘very strong desire’ on the part of the Investment Team that IEL be in a position to receive franked dividends and pass them on to its shareholders. But any incurring of interest in any company down the line from IEL would impede the flow of such dividends up to it.

19. Daniels said that to the extent that a liability to pay interest down the line constituted an impediment to the free flow of dividends up to IEL, ‘there was a necessity to try and improve that situation’.

20. I am not persuaded that simplification of the complex debt and equity lines within the Group explains the Spassked Restructuring. Overall, those lines appear to have remained as complex afterwards as they were before. The Spassked Structure may have had simpler debt and equity lines than alternative forms of restructuring that were being considered, but that is a different matter. In any event, a motive of simplification of debt and equity lines does not assist Spassked in relation to the issues under subs 51(1).

21. I am satisfied that the dominant motivation for the Spassked Structure was to be found in the following interrelated considerations:

o the removal of many dividend traps in the Group in favour of one large dividend trap (Spassked) which could be sidestepped, so that dividends, whether franked or unfranked, could be streamed up to GIH and franked dividends paid to IEL;

o ensuring the availability of s 46 tax rebates; and

o the concentration of all transferable tax losses in a single company in the Group (Spassked).

But this alone does not signify that the interest expense lay outside the terms of subs 51(1): consistently with the subjective motivation described, the borrowings might also have been explained by an expectation (in the positive sense explained at [164]-[166]) or purpose of gaining or producing assessable income.

22. The dispute with the ATO did not arise before early 1991 and did not affect the decision of GIH whether to pay a dividend to Spassked in the years ended 30 June 1988, 1989 and 1990. Moreover, Daniels conceded that it would not have affected that decision in respect of the year ended 30 June 1991 to the same extent as it did later years. Quite apart from the tax dispute with the ATO, GIH would have continued not to pay dividends to Spassked because Spassked remained a dividend trap, and did so, as Daniels agreed, at least until he left IEL on 30 June 1994.

23. Spassked was the only shareholder in GIH entitled to unfranked dividends. It follows that, unless GIH’s articles of association were altered:

o if there was an expectation or purpose that Spassked would cease to be a dividend trap and a repository of losses and that GIH would then pay unfranked dividends, there was an expectation or purpose that payment of them would be made to Spassked; and

o if the facts suggest that GIH intended to pay unfranked dividends, they suggest that it intended to pay them to Spassked.

But I am not satisfied that any such expectation, purpose or intention existed. It must not be overlooked that it was open to GIH, if it wished to upstream unfranked dividends it had received from the Subcos, to pay the relevant tax and pay franked dividends to IEL. That is, in effect, it was possible, by paying the relevant tax to ‘convert’ incoming unfranked dividends into outgoing franked dividends.’

47 His Honour’s accordingly at [236] did not accept:

‘…that it was part of the plan, purpose or expectation (in the sense explained) of the Spassked Structure that GIH would pay dividends to Spassked.’

48 Commenting on the significance of the two dividend payments to Spassked, his Honour expressed the view that they arose spontaneously and were perhaps ‘an attempt to create an appearance.’

49 His Honour’s conclusions were summarised by him in his judgment at [239] to [245] as follows:

‘239. I accept that the question of the long term future of the Spassked Structure may have fleetingly crossed the minds of Daniels and Cottam. But that was as far as it went. I find that what was important to them was to achieve the immediate objectives of making Spassked the dedicated dividend trap and loss centre of the Group: attention could be given to any unwelcome necessity which might exist for it to receive dividends from GIH in the future if and when the occasion to think about that unpleasant matter arose.

240. I do not accept that Daniels or Cottam expected (now in the neutral factual sense) that Spassked would receive, or was likely to receive, dividends from GIH. In so far as their testimony is to the contrary, I think they have engaged in a process of reconstruction of their 1987 thought processes. (It should go without saying that this does not suggest fabrication.) Having regard to the disparity between the large and rapidly increasing indebtedness of Spassked to IEF on and from 30 December 1987 down to 28 June 1990, and the level of GIH’s funds available to be paid to Spassked at any time during that period, and the lack of alarm or protest over that disparity at the time, I conclude that they saw nothing untoward in that growing disparity. Their acquiescence points against a subjective expectation or purpose that GIH’s funds were to be used to discharge Spassked’s debt to IEF.

241. I am not persuaded that Daniels or Cottam assessed or thought of the Spassked Structure as having a likely lifespan of five to ten years. I find that either they did not direct their minds to its lifespan at all, or that if they did, it was regarded as of no significance whatever and as something which may or may not call for attention at some unidentified future time. I think they arrived at the ‘five to ten years’ estimate in the witness box or at least while reflecting upon the case in relatively recent times, not back in 1987 when the Spassked Structure was devised.

242. The ATO’s claims and resulting disputation prove to be of no significance. I accept Daniels’ testimony that the potential tax liability might well have inhibited payment of dividends if such a payment had been otherwise contemplated. But it was not contemplated: GIH was already committed to a course of not paying dividends to Spassked. It is not to the point to say that if Spassked had ceased to be a dividend trap and if it had ceased to have tax losses, nonetheless dividends would not have been paid to it for a new supervening reason: the possible tax liability. The character of the interest expense must be determined as at the time of its incurrence, in this case at the times of the borrowings of the money on which it accrued. It is at those times that expectations and purposes are to be identified. The position might be different if the ATO had asserted the tax liability before the first occasion of decision as to whether GIH was to pay dividends to Spassked, or if, somehow, the Commissioner’s only reason for regarding the interest expenses as non-deductible was the non-payment of dividends to Spassked after the outbreak of hostilities between the Group and the ATO.

243 I have dealt at length above with the states of mind of Daniels and Cottam. It should be emphasized, however, as I said earlier, that on the basis of the objective facts alone, that is, leaving their states of mind out of account, I would have no difficulty in concluding that the interest expense is not shown to be within subs 51(1). My purpose in addressing the states of mind of Daniels and Cottam is to allow for the possibility that the expense is within the subsection after all, notwithstanding appearances. The relevance of Cottam’s state of mind is doubtful in any event because he was not a director of Spassked at the relevant times, and I have not been prepared to attribute Daniels’ state of mind to his co-directors.

244. For the above reasons, I do not think that the required expectation (in the positive sense explained at [164]-[166]) or purpose is established, even having regard to Daniels’ and Cottam’s testimony as to their subjective expectations and purposes.

245. Spassked’s interest expense of $888,165,526 paid to IEF in respect of the year of income ended 30 June 1992 was not a loss or outgoing incurred in gaining or producing assessable (dividend) income from GIH, or necessarily incurred in carrying on a business for the purpose of gaining or producing such income.’

The Appellants’ Submissions.

50 The Appellants’ submissions, which to some extent were overlapping, may now be summarised as follows:

* The learned Primary Judge erred in law in considering the subjective motivation of IEL and its directors.

* The learned Primary Judge erred in law in concluding that an unfranked dividend could be converted into a franked dividend (see [23] reproduced in [46] of these reasons) and this error affected the conclusion reached by him.

* The learned Primary Judge erred in not having regard to the circumstance that Spassked was an intermediate holding company and in business to serve the ends of the IEL group.

* His Honour failed to take account of the fact that IEL required not only franked dividends, but unfranked dividends which if they were to flow to IEL must come from Spassked.

* On the facts his Honour should have held that the funds available for distribution as profits would eventually exceed the compounded loan debt thus enabling that debt to be repaid and dividends to flow to Spassked.

* On the evidence his Honour should have held that the Spassked structure was one established with a view to gain by the future receipt of a dividend by Spassked.

* This Court on Appeal should find, contrary to the findings of the learned Primary Judge that those responsible for implementing the Spassked structure expected that Spassked would cease to be a dividend trap in the medium term and that thereafter dividends would flow to it.

* The learned Primary Judge failed to have regard to all the objective relevant circumstances.

The Case Law

51 Section 51(1) is written in simple terms as is appropriate for a section designed to provide over a large range of factual circumstances for a deduction of what may be here referred to as working expenses, whether those expenses are incurred in the course of a business or in the course of other income producing activities. As is apparent from its terms there are two positive limbs, one of which must be satisfied before the deduction is allowable. However, it seems clear that the second (business) limb adds little, if at all to the first limb: Ronpibon Tin NL & Tongkah Compund NL v Federal Commissioner of Taxation (1949) 78 CLR 47 at 56. Indeed, to some extent it is narrower, in that it can operate only when the taxpayer carries on a business. The word ‘necessarily’ which appears in the second limb is intended, so it was said in Ronpibon to mean no more than ‘clearly appropriate or adapted for’ (see at 56.)

52 In the discussion which follows the emphasis will be on the first limb. This is so because it avoids the difficulty which the taxpayer would have in falling within the second limb that, at least prima facie, it is not carrying on any business. However, the question whether it is will be discussed later when considering the third submission of the appellants. It suffices here to say that what is said here of the first limb of the subsection is for all relevant purposes equally applicable to the second limb.

53 There have been a multitude of cases which have had cause to consider the subsection and particularly the required connection between the incurring of the outgoing and the gaining or producing of assessable income or carrying on a business for the purpose of gaining or producing assessable income. The cases have given rise to what Dixon CJ once referred to as ‘felicitous expressions’. But those felicitous expressions were not designed to, nor could they, take the place of the language of the section itself.

54 A convenient starting point in considering the issues which arise in the present case is the well-known decision of the High Court in Ronpibon. That case concerned taxpayers who, prior to the war, had derived income in countries outside Australia which income had been, as a result of the then s 23(q) of the Act, exempt from Australian income tax because it was taxable in the overseas country of source. The operations of the taxpayers were brought to an end by the Second World War. However, each company continued to have expenses in Australia, and each company at least hoped it would resume business activities when the war came to an end. Each company sought to deduct these expenses against income it derived from Australian investments. The actual decision in the case is concerned with the need to apportion deductions and in that connection the need to establish how much of the expenditure incurred was fairly and properly attributable to the gaining of assessable income. That question has no direct relevance to the present case. However, in the course of its reasons the Full High Court, Latham CJ, Rich, Dixon, McTiernan and Webb JJ said at 57:

‘In brief substance, to come within the initial part of the sub-section it is both sufficient and necessary that the occasion of the loss or outgoing should be found in whatever is productive of the assessable income, or, if none be produced, would be expected to produce assessable income.’

55 It is clear, as the learned Primary Judge observed, that the reference in the passage cited to expectation was not intended to refer to the actual expectation of a taxpayer but rather was used in an objective sense. That follows from the use of the language ‘would be expected’ in the subsection. It is clear too, by reference to the order actually made by the Court that their Honours were of the view that the question of apportionment involved an issue of fact and it is certainly arguable from the order that their Honours by accepting the need for apportionment between assessable income and other income not being assessable income accepted that it would be possible for future exempt income arising after the war had finished and the overseas business had revived to be taken into account in making the apportionment. It was a matter which their Honours were not called upon to decide.

56 While it can be said that at the time Ronpibon was decided there was no authoritative decision on the meaning of the words ‘the assessable income’ which appear in both the first and second positive limbs (although the passage cited makes it clear that a deduction would be available notwithstanding that there is no assessable income derived in the year of income) it is certainly now beyond doubt that the subsection does not require the assessable income referred to, to be the assessable income of the year of income, but it may refer to the assessable income of a past or future year of income. So, in AGC (Advances) Ltd v Federal Commissioner of Taxation (1975) 132 CLR 175, it was recognised both by Barwick CJ (at 189) and by Mason J (at 195-197) that the words ‘the assessable income’ refer to ‘the assessable income of the taxpayer generally without regard to division into accounting periods.’ Recently in Commissioner of Taxation v Consolidated Press Holdings Ltd (2001) 207 CLR 235 (at [74], [75]), in a passage cited by the learned Primary Judge, the High Court in a joint judgment said:

‘But it is the relevance of the loss or outgoing to some kind of income, actual or potential, that warrants the conclusion that it is incurred in a manner necessary for the application of s 51(1). It was the purpose of the borrowing, that is to say, the acquisition of shares expected to produce dividends as a result of the BAT takeover, that gave rise to the potential application of s 51(1). On the hypotheses (which is in dispute) that it would be reasonable, in the absence of the tax purpose, to expect that ACP would have subscribed directly for shares in CPIL(UK), and that income in the form of dividends paid by CPIL(UK) as a result of the BAT takeover would have had a foreign source, then it is the fact that the purpose of the borrowing was to obtain such income that made the interest potentially deductible under s 51(a).’

57 Later their Honours spoke of ‘potential or prospective income’ as relevant to a deduction under s 51(1) notwithstanding that no income had commenced to be derived.

58 One thing is clear from the jurisprudence on s 51(1) is that for an amount to be deductible it is unnecessary for a taxpayer to show that the outgoing would produce assessable income. As the Full High Court said in Federal Commissioner of Taxation v Smith (1981) 147 CLR 578 at 585-6:

‘The section does not require that the purpose of the expenditure shall be the gaining of income of that year, so long as it was made in the given year and is incidental and relevant to the operations or activities regularly carried on for the production of income. What is incidental and relevant in the sense mentioned falls to be determined not be reference to the certainty or likelihood of the outgoing resulting in the generation of income but to its nature and character, and generally to its connexion with the operations which more directly gain or produce the assessable income.’

59 Smith is, in the present context an important case. It concerned an employed medical practitioner who claimed to be entitled to deduct premiums for an income replacement policy in the event of accident. The proceeds of such a policy would, if received, be assessable income. However, it would be no doubt hoped by the taxpayer that no such proceeds would ever be received. Nevertheless any benefit under the policy would be assessable income. The fact that it was unlikely that the taxpayer would ever receive the assessable income did not preclude the deductibility of the premium. There was a sufficient connection between the purchase of the cover ‘and the consequent earning of assessable income.’

60 While it is no doubt clear that expenditure on a feasibility study to determine whether to carry on some business activity would be expenditure incurred too soon to be deductible, (see Softwood Pulp and Paper Ltd v Federal Commissioner of Taxation (1976) 76 ATC 4439) the failure of such expenditure to satisfy the tests of s 51(1) is not to be found in the fact that the business activity might never generate assessable income. Rather the income producing activity or business has not yet commenced so that the amount claimed to be deductible has been incurred at a point too soon. However, once the business does commence it matters not to deductibility that the income producing activity or business it might fail before any assessable income is produced.