FEDERAL COURT OF AUSTRALIA

Commissioner of Taxation v Zoffanies Pty Ltd [2003] FCAFC 236

TAXATION – whether the Administrative Appeals Tribunal applied the wrong test under s 177D of the Income Tax Assessment Act 1936 (Cth) by considering the subjective rather than objective intention of the taxpayer – whether the Administrative Appeals Tribunal failed to consider an alternative particularisation of the scheme alleged to exist by the Commissioner and thereby erred in law

PRACTICE AND PROCEDURE – whether the Court has power to order the remittal of part of the matter to the Administrative Appeals Tribunal where the Commissioner appealed only as to that part of the judgment of the Administrative Appeals Tribunal and, if so, whether it ought to so remit

Administrative Appeals Tribunal Act 1975 (Cth) s 44(1), 44(3)(b)(ii)

Income Tax Assessment Act 1936 (Cth) s 73B, 73CA, 177A(1), 177D, 177F(1), s 260

Migration Act 1958 (Cth)

Collector of Customs v Agfa-Gevaert Ltd (1996) 186 CLR 389 applied

Collector of Customs v Pozzolanic Enterprises Pty Ltd (1993) 43 FCR 280 applied

Commissioner of Taxation v Spotless Services Ltd (1996) 186 CLR 404 applied

Eastern Nitrogen Ltd v Commissioner of Taxation (2001) 108 FCR 27 referred to

Minister for Immigration & Ethnic Affairs v Gungor (1982) 42 ALR 209 applied

Minister for Immigration & Multicultural Affairs v Thiyagarajah (2000) 199 CLR 343 applied

Minister for Immigration and Ethnic Affairs v Wu Shan Liang (1996) 185 CLR 259 applied

Minister for Immigration and Multicultural Affairs v Wang (2003) 196 ALR 385 approved

Minister for Immigration and Multicultural Affairs v Yusuf (2001) 206 CLR 323 applied

Morales v Minister for Immigration and Multicultural Affairs (1998) 82 FCR 374 applied

Peabody v Commissioner of Taxation (1993) 40 FCR 531 applied

Re Minister for Immigration and Multicultural and Indigenous Affairs; Ex parte Applicants S134/2002 [2003] HCA 1 applied

COMMISSIONER OF TAXATION v ZOFFANIES PTY LIMITED

N 1029 OF 2002

HILL, HELY, & GYLES JJ

24 OCTOBER 2003

SYDNEY

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

N1029 OF 2002 |

ON APPEAL FROM THE ADMINISTRATIVE APPEALS TRIBUNAL

|

BETWEEN: |

COMMISSIONER OF TAXATION APPELLANT

|

|

AND: |

ZOFFANIES PTY LIMITED RESPONDENT

|

|

HILL, HELY & GYLES JJ |

|

|

DATE OF ORDER: |

24 OCTOBER 2003 |

|

WHERE MADE: |

SYDNEY |

THE COURT ORDERS THAT:

1. Appeal allowed.

2. The decision of the Tribunal is set aside insofar as it found that the provisions of Pt IVA of the Income Tax Assessment Act 1936 (Cth) (‘the Act’) did not apply to the circumstances of the case such as to support the income tax assessment dated 14 November 2000 for the substituted accounting period ending on 30 September 1992 (‘the assessment’) against which the taxpayer’s objection in issue was lodged.

3. The proceeding be remitted to the Administrative Appeals Tribunal to hear and determine the issue as to whether Pt IVA of the Act applied to the circumstances so as to support the assessment by the Commissioner giving rise to the objection in issue and, in the light of such determination, to decide the taxpayer’s objection against the assessment.

4. The taxpayer is to pay the Commissioner’s costs of the appeal.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

N1029 OF 2002 |

ON APPEAL FROM THE ADMINISTRATIVE APPEALS TRIBUNAL

|

BETWEEN: |

COMMISSIONER OF TAXATION APPELLANT

|

|

AND: |

ZOFFANIES PTY LIMITED RESPONDENT

|

|

JUDGES: |

HILL, HELY & GYLES JJ |

|

DATE: |

24 OCTOBER 2003 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

1 The appellant, the Commissioner of Taxation (‘the Commissioner’), appeals from a decision of the Administrative Appeals Tribunal (‘the Tribunal’) which set aside the Commissioner’s decision disallowing an objection lodged by the respondent Zoffanies Pty Limited (‘the taxpayer’) in respect of an assessment of income tax for the substituted accounting period ending on 30 September 1992 (‘the year of income’), adopted in lieu of the year ending on 30 June 1992.

2 In its tax return for the year of income the taxpayer had claimed to be entitled to a deduction in the amount of $109,947. The amount claimed was part of the loss said to have been incurred by Macquarie Syndication (No 3) Pty Ltd (‘MS3’) in that year of income. Both the taxpayer and MS3 were part of a group of companies of which Macquarie Bank Ltd (‘MBL’) was the parent company. Accordingly, if the loss claimed to have been incurred by MS3 was an allowable deduction to it, part of that loss could be transferred to the tax payer and become an allowable deduction to it. Indeed, in the years of income 1992 to 2001 inclusive, MS3 had claimed losses arising from the arrangements, the subject of the present proceedings, and transferred parts of the losses claimed to 14 wholly owned subsidiaries of MBL, one of which was the taxpayer.

3 The appeal to this Court is an appeal on a question of law, that is to say, an appeal which is limited to a question of law: s 44(1) of the Administrative Appeals Tribunal Act 1975 (Cth) (‘the AAT Act’). The appeal, which is in the original jurisdiction of the Court, was heard by a Full Court in accordance with a direction made by the Chief Justice under s 44(3)(b)(ii) of the AAT Act in consultation with the President of the Tribunal.

The Facts

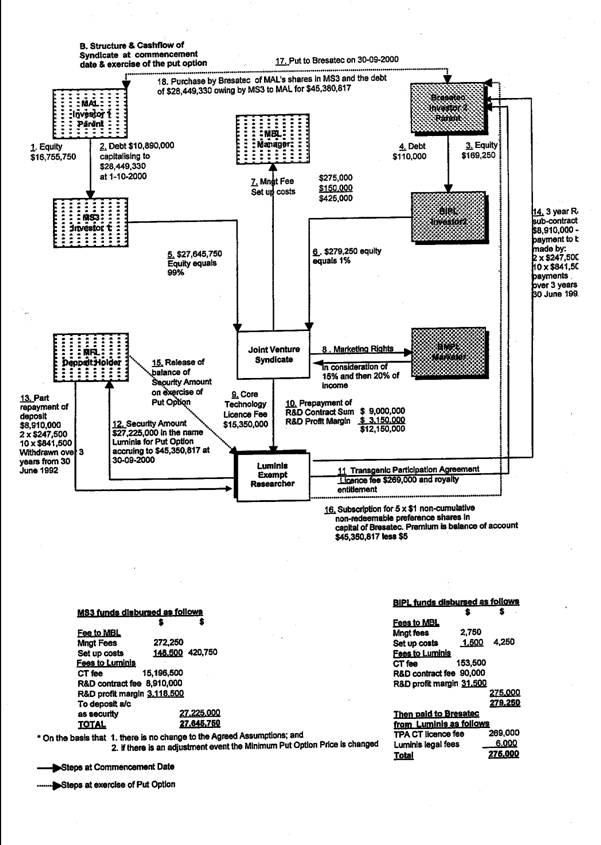

4 The appeal concerns arrangements entered into on 30 June 1992 and 1 July 1992. The agreements entered into were complex and involved a number of entities. They are best understood in association with a diagram which was an exhibit in the proceedings. The exhibit is here reproduced.

5 There are two minor errors in the diagram. Those errors are not material to an understanding of the arrangements entered into. In point 17 of the diagram the date ‘30 September 2000’ should be either 1 or 3 October 2000. The date ‘30 June 1992’ in item 14, which is not in any case reproduced here, was 30 June 1995. There was also a dispute (it is not presently material) between the parties concerning the quantum of set-up costs appearing under that heading and the subheading ‘Fees to MBL’.

6 The background to the arrangements entered into was transgenic technology, initially developed by research scientists at the University of Adelaide from late 1982. The immediate objective of their research was the production of more food efficient, faster growing and leaner pigs. Initially the intellectual property from that research vested in Luminis Pty Ltd (‘Luminis’) as trustee for the University of Adelaide. On 29 February 1988 the intellectual property in the transgenic technology was transferred by Luminis to Bresatec Ltd (‘Bresatec’), an unlisted public company. The consideration for the transfer was the issue to Luminis of 4,000,000 shares in Bresatec.

7 The technology was the subject of interest to a number of investors, including American Cyanamid Company (‘Cyanamid’), which in 1991 was granted by Bresatec options to purchase a licence from Bresatec of the technology and an option to purchase shares in Bresatec. As a result of the exercise of the second option, Cyanamid became the owner of a parcel of shares in that company. It is common ground that the technology had significant potential, not only in producing high quality lean pork but also in other applications. As it happens, however, the commercialisation of the technology was ultimately hindered by the refusal of Federal and State regulators in Australia to give unequivocal approval for human consumption of pork from transgenic pigs. That difficulty, however, was not foreseen in 1992.

8 Some time in 1991 the possibility arose of the formation of a research and development syndicate (‘R & D syndicate’) involving MBL to raise funds for a three-year research program concerning embryo stem cell technology and the transgenic pig technology (‘the core technology’). It is unnecessary for present purposes to detail the course of events which led to the transactions that are the subject of the present proceedings. It suffices here to say that any such syndication would, if the technology were in Bresatec’s hands, have involved it paying tax on any licence fee it received. In February 1992 a decision was made that the intellectual property owned by Bresatec would be transferred to Luminis. At the time Luminis owned not in its own right, but in its trustee capacity, some of the relevant intellectual property to which the R and D syndicate would need access, particularly in relation to the embryo stem cell technology. Accordingly, before the arrangements under consideration were entered into, Bresatec had agreed to grant to Luminis a licence of the Bresatec technology, in contemplation of Luminis receiving from the R & D syndicate a licence fee in respect of the core technology.

9 The proposal that MBL would participate in an R & D syndicate appears to have originated in July 1991. Dr Venning, an independent valuer, was approached in 1992 to value the core technology. Dr Venning’s formal instructions came via MBL, although Bresatec was responsible for paying his fees.

10 Ultimately Dr Venning concluded that a valuation of around $15.35 million dollars for the core technology to be used by the R & D syndicate was a reasonable figure lying within a range of values he had calculated. The Tribunal found that Dr Venning’s valuation was an arm’s length valuation.

11 Agreement was then reached between the Luminis interests and the MBL interests that an arrangement be entered into. The progress of the negotiations which resulted in the formal agreements being entered into is recorded in the Tribunal’s reasons. It is not necessary to repeat the detail of it. The formal steps that were taken were as follows:

(1) Bresatec granted Luminis a 15 year non exclusive license of the transgenic pig technology in consideration of a payment of $269,000 and a royalty. On 16 September 1992 the licence granted became exclusive.

(2) Macquarie Acceptance Ltd (‘MAL’), a wholly owned subsidiary of MBL, advanced at interest the sum of $10,890,000 and subscribed for equity capital in MS3 in the sum of $16,755,750. Interest on the loan was capitalised and by 1 October 2000 the debt and capitalised interest amounted to $28,449.330.

(3) A joint venture agreement was entered into between MS3 and Bresatec Investments Pty Ltd (‘Bresatec Investments’) a wholly owned subsidiary of Bresatec. The syndicate shares were issued in the ratio of 99 (MS3) to 1 (Bresatec Investments). MS3 contributed to the syndicate $27,645,750, those moneys emanating from the debt and equity investment made by MAL. Bresatec Investments contributed $279,250, the funds emanating from an advance of $110,000 made by Bresatec to it and an equity subscription of $169,250 from that company. MBL was to manage the syndicate and became obliged to pay a management fee of $425,000 to MBL, including set-up costs.

(4) Luminis, the owner of the embryo stem cell technology in its capacity as a trustee and the licensee from Bresatec of the transgenic pig technology then granted the R & D syndicate a 15 year exclusive licence/sublicense in consideration of the payment to it of $15,350,000 (‘the core technology licence fee’). Having regard to the syndicate shares, $15,196,500 of this was attributable to MS3 and $153,500 to Bresatec Investments.

(5) The R &D syndicate then appointed Luminis to carry out a program of research and development in consideration of $12,150,000. The budget for research and development was $9,000,000 and there was in addition a profit margin to Luminis of $3,150,000. Under the agreement a scheduled three year research and development period was to be followed by a commercialisation period of five years. The total of $12,150,000 was paid immediately in cash to Luminis.

(6) From the payment Luminis received from the R & D syndicate, it deposited $27,225,000 with Macquarie Finance Ltd (‘Macquarie Finance’) which apparently carried on a business of borrowing and lending money. As amounts were required for the funding of the research and development, they were drawn down by Luminis.

(7) Luminis, in fact, subcontracted the research and development work to Bresatec. Under that subcontracting arrangement Luminis was to pay $8,910,000 by various instalments over three years to fund the actual work.

(8) The R & D syndicate also granted to Bresatec Marketing Pty Ltd (‘Bresatec Marketing’) an option which, if exercised, entitled Bresatec Marketing to market products resulting from the commercialisation of the core technology in consideration of a licence fee.

(9) A put option was granted by Bresatec to MAL. It was critical to MAL that it have the right to unravel the arrangements and receive, effectively, its money back in the event that it did not wish to continue to be involved in commercialising the technology. The mechanism to achieve this was a put option under which, if exercised, Bresatec would be required to purchase from MAL the issued share capital in MS3 at a predetermined price. The option was exercisable at the conclusion of the commercialisation period in 2000 and as a result of a later amendment in 1992 the exercise price was $45,350,817.06. There appears to have been an issue at the hearing whether there was ever any possibility that MBL would not exercise its put option. The evidence was that the put option would only not be exercised if MBL was entitled to receive royalties of approximately $64,000,000 or more. Because under the agreements as entered into, Bresatec Marketing was entitled to 85% of the revenue in the first three years and 80% thereafter, it is obvious that the total revenue generated by Bresatec Marketing would need to be a large sum indeed before the put option would not be exercised. The matter is not the subject of a specific finding, although the Tribunal member appears to have rejected the submission that there was little possibility that MAL would not exercise the put option on the basis that such a claim could only be made in hindsight and that, at least, in 1992 the parties were optimistic about the success of the project.

(10) The money which Luminis had deposited with Macquarie Finance became security for a guarantee to MAL that Bresatec would, if the put option was exercised purchase MAL’s shares in MS3.

12 It may be remarked that the Tribunal’s reasons consist substantially of an outline of the evidence given by the various witnesses who gave evidence at the hearing which extended over a period of three weeks. It seems to be the case that the Tribunal accepted all evidence recorded in that outline. However, it would certainly be more satisfactory if the Tribunal made it clear what its findings of fact were rather than embark on a summary of the evidence of each witness. Alternatively, if it was thought to be appropriate to set out a summary of the evidence of each witness it would be desirable that the Tribunal indicate specifically whether that evidence was accepted in whole or, to the extent that it was accepted only in part, what part of the evidence was in fact accepted. No complaint was, however, made by either party that the Tribunal had failed to comply with its obligations to make findings of fact and indeed it was accepted that the Tribunal in summarising the evidence of each witness had accepted that evidence and found the facts in accordance with it.

13 Obviously it was critical to the arrangement, at least if the put option was to be exercised, that Bresatec have sufficient funds to pay the consideration it would become liable to pay to MAL for the transfer of the capital in MS3. The funds could only come from the amount which Luminis had deposited with Macquarie Finance unless, of course, the commercialisation of the technology was successful and the purchase price could be financed in some other way. That deposit was agreed to be security for the payment on exercise of the put option. So long as the funds remained on deposit with Macquarie Finance and interest was capitalised, the purchase price could be achieved, especially as Luminis (as trustee) was not liable directly to pay tax on income to which a beneficiary was presently entitled and the University of Adelaide, which was its beneficiary and which was presently entitled to the income, was exempt from income tax. The agreements did permit Luminis to substitute by way of security, bonds or other investments in place of the monies deposited with Macquarie Finance but subject to the consent of the Macquarie interests. Although the matter is not the subject of any specific finding, it may be inferred that the parties contemplated that the $27,225,000 put on deposit with Macquarie Finance would remain there as security for exercise of the put option. Certainly that is what happened. As already indicated, commercialisation was hindered by government inaction as a result of the public perception unfavourable to transgenic meat. Accordingly the put option was actually exercised on 30 September 2000.

The Issues in the Tribunal

14 The Commissioner’s primary case in the Tribunal turned upon the provisions of s 73B of the Income Tax Assessment Act 1936 (Cth) (‘the Act’). It was the Commissioner’s submission that the core technology licensing fee and an amount of $178,098 representing interest paid by MS3 to MAL were not research and development expenditure deductible under the provisions of s 73B. This was said to be the case because, so the Commissioner argued, the R & D syndicate and Luminis did not deal with each other at arm’s length in relation to the incurring of the expenditure: see s 73B(31)(b). It was submitted that the expenditure in question was greater than would have been incurred if such an arm’s length dealing had been undertaken.

15 The issues arising under s 73B(12) were resolved in favour of the taxpayer. Although the Commissioner’s grounds of appeal asserted that the Tribunal had made a legal error in this part of its decision, this ground of appeal was withdrawn before the hearing of the appeal. Accordingly, no issue arose on the appeal with respect to the specific provisions of the Act related to deductions for research and development expenditure.

16 In addition to the issues arising under s 73B the Commissioner sought to support the assessment on the basis that there had been a scheme to which the provisions of Part IVA of the Act applied and that accordingly the Commissioner was authorised to make a determination under s 177F(1) disallowing to MS3, as a party to the R & D syndicate, its share of the core technology licence fee and interest. It is important to note that the Commissioner at no time sought to disallow to the R & D syndicate a deduction for the sum of $12,150,000, being for actual research and development.

17 Accordingly the second issue before the Tribunal was whether the facts disclosed a scheme to which the provisions of Part IVA of the Act applied: s 177D. This issue the Tribunal also decided in favour of the taxpayer.

18 It will be necessary to examine in greater detail the case put by the Commissioner under Part IVA and the Tribunal’s reasons for finding against the Commissioner

The Issues on the Appeal

19 Ultimately there were only two issues in the appeal. These were:

1) That the Tribunal erred in applying the wrong test in reaching the conclusion it drew under s 177D of the Act. Specifically, it was submitted, the Tribunal applied a test of subjective purpose rather than, as required by s 177D, what may be referred to as an objective test of purpose.

2) That the Tribunal in concluding in favour of the taxpayer failed to consider an alternative particularisation of the scheme to which the provisions of Part IVA applied advanced at the hearing on behalf of the Commissioner.

20 The second issue was formulated in the alternative. The alternative was that the Tribunal had erred in law by failing to consider the submission of the Commissioner put to the Tribunal, that in reaching the conclusion required to be drawn for the purpose of s 177D the Tribunal was required to weigh against the commercial benefits (including such as might become available to MS3 in the future should the technology be commercialised and the put option not be exercised), the tax deductions contained in the Commissioner’s alternative particularisation of the scheme, the latter of which deductions were certain and immediate (but for Part IVA itself), whereas the commercial benefits were uncertain and future.

The Statutory Provisions – Part IVA

21 Section 177F(1) of the Act permits the Commissioner to disallow a deduction to a taxpayer where that deduction is a ‘tax benefit’ as defined and is obtained by the taxpayer in connection with a ‘scheme’ to which Part IVA applies.

22 There was no dispute between the parties that each of the deductions to which reference has been made, that is to say, those particularised by the Commissioner in the alternative particularisation of the scheme, which deductions include those the subject of the present proceedings, fall within the meaning of the expression ‘tax benefit’. Nor was there any dispute between the parties that those tax benefits were obtained in connection with the scheme. The only dispute between the parties was whether the scheme was one to which the provisions of Part IVA of the Act applied.

23 A scheme will be one to which the provisions of Part IVA apply if it falls within s 177D of the Act. That section provides:

‘This Part applies to any scheme that has been or is entered into after 27 May 1981, and to any scheme that has been or is carried out or commenced to be carried out after that date (other than a scheme that was entered into on or before that date), whether the scheme has been or is entered into or carried out in Australia or outside Australia or partly in Australia and partly outside Australia, where:

(a) a taxpayer (in this section referred to as the relevant taxpayer) has obtained, or would but for section 177F obtain, a tax benefit in connection with the scheme; and

(b) having regard to:

(i) the manner in which the scheme was entered into or

carried out;

(ii) the form and substance of the scheme;

(iii) the time at which the scheme was entered into and the

length of the period during which the scheme was carried out;

(iv) the result in relation to the operation of this Act that,

but for this Part, would be achieved by the scheme;

(v) any change in the financial position of the relevant

taxpayer that has resulted, will result, or may

reasonably be expected to result, from the scheme;

(vi) any change in the financial position of any person who

has, or has had, any connection (whether of a business, family or other nature) with the relevant taxpayer, being a change that has resulted, will result or may reasonably be expected to result, from the scheme;

(vii) any other consequence for the relevant taxpayer, or

for any person referred to in subparagraph (vi), of the scheme having been entered into or carried out; and

(viii) the nature of any connection (whether of a business,

family or other nature) between the relevant taxpayer and any person referred to in subparagraph (vi);

it would be concluded that the person, or one of the persons, who entered into or carried out the scheme or any part of the scheme did so for the purpose of enabling the relevant taxpayer to obtain a tax benefit in connection with the scheme or of enabling the relevant taxpayer and another taxpayer or other taxpayers each to obtain a tax benefit in connection with the scheme (whether or not that person who entered into or carried out the scheme or any part of the scheme is the relevant taxpayer or is the other taxpayer or one of the other taxpayers).’

The Questions of Law

24 There was also no dispute between the parties that each of the submissions of the Commissioner involved a question of law.

25 It was common ground that there will be a question of law where the Tribunal applies the wrong legal test. The question of law will be one which involves the construction of the Act itself: Collector of Customs v Agfa-Gevaert Ltd (1996) 186 CLR 389 at 396-398.

26 It was likewise common ground that a question of law arises where the Tribunal fails to consider a submission which a party has raised. In such a case the Tribunal will have failed actually or constructively to exercise its jurisdiction: cf Minister for Immigration and Multicultural Affairs v Yusuf (2001) 206 CLR 323 at 346 and 349 – 352 per McHugh, Gummow and Hayne JJ.

27 Each of the submissions require careful consideration of the Tribunal’s reasons. In undertaking this task I acknowledge the need to both read the reasons as a whole and consider them fairly. As Kirby J said in Minister for Immigration and Ethnic Affairs v Wu Shan Liang (1996) 185 CLR 259 at 291:

‘It is erroneous to adopt a narrow approach, combing through the words of the decision-maker with a fine appellate tooth-comb, against the prospect that a verbal slip will be found warranting the inference of an error of law.’

28 I acknowledge, also, that in Wu Shan Liang the remaining members of the High Court (Brennan CJ, Toohey, McHugh and Gummow JJ) referred with approval to the decision of French J in this Court in Collector of Customs v Pozzolanic Enterprises Pty Ltd (1993) 43 FCR 280 at 286-287 where his Honour said in a passage equally relevant to the present case:

‘The limits within which the jurisdiction is conferred require that it be exercised with restraint. Only in exceptional circumstances should the decision of the Tribunal not be the final decision: Blackwood Hodge (Australia) Pty Ltd v Collector of Customs (NSW) (1980) 47 FLR 131 at 145 (Fisher J); Commissioner of Taxation (Cth) v Cainero (1988) 88 ATC 4,427 (Foster J). As the Full Court said in Repatriation Commission v Thompson (1988) 9 AAR 199 at 204:

‘ ... the nature of the task of this Court is clear. It is to leave to the tribunal of fact decisions as to the facts and to interfere only when the identified error is one of law.’

This translates to a practical as well as principled restraint. The Court will not be concerned with looseness in the language of the Tribunal nor with unhappy phrasing of the Tribunal's thoughts: Lennell v Repatriation Commission (1982) 4 ALN N 54 (Northrop and Sheppard JJ); Freeman v Defence Force Retirement and Death Benefits Authority (1985) 5 AAR 156 at 164 (Sheppard J); Repatriation Commission v Bushell (1991) 13 AAR 176 at 183 (Morling and Neaves JJ). The reasons for the decision under review are not to be construed minutely and finely with an eye keenly attuned to the perception of error: Politis v Commissioner of Taxation (Cth) (1988) 16 ALD 707 at 708 (Lockhart J).’

29 Particularly in considering whether the Tribunal has erred in law by failing to consider an argument advanced by a party it will be necessary to consider not merely the reasons for the decision but also the submissions made to the Tribunal. It may be said, at least generally, that a Tribunal will commit no error of law by failing to deal with an argument that was not put to it: Re Minister for Immigration and Multicultural and Indigenous Affairs; Ex parte Applicants S134/2002 [2003] HCA 1 at [32] per Gleeson CJ, McHugh, Gummow, Hayne and Callinan JJ. Reference to submissions made to the Tribunal may also be relevant to explain the language used by the Tribunal in its reasons and to rebut a suggestion that it should be concluded from the Tribunal’s reasons that it applied a wrong test.

30 Subject to such help as may be obtained from the submissions it will be necessary to set out in some detail the provisions of the Tribunal’s reasons so far as they relate to each of the Commissioner’s submissions.

Did the Tribunal fail to address the argument advanced by the Commissioner that account should be taken of the additional tax benefits?

31 Prior to the commencement of the proceedings, the taxpayer’s solicitors requested particulars of the relevant scheme which the Commissioner submitted should be considered under Part IVA. In response the Commissioner detailed the scheme as consisting of the various steps to which reference has already been made. These steps were the agreements reached between the various parties noting the relevant tax benefits obtained from the scheme to be MS3’s share of interest and the licence fee for the core technology which was the subject of the proceedings in the Tribunal.

32 In opening submissions which were reduced to writing the Commissioner’s counsel wrote of there being tax deductions to ‘MBL entities’ of approximately $71,825,000 over the period from July 1992 to October 2000 and enumerated these deductions as including not merely the deductions disallowed and the subject of the present proceedings but also the research and development deduction to the syndicate of which $8,910,000 would pass to Bresatec. There was also interest incurred by the various Macquarie entities, including interest payable by MS3 to MAL. It may be observed that the Commissioner, at that stage, made no attempt to amend the particulars supplied to the taxpayer’s solicitors, assuming such an amendment was necessary.

33 After the hearing had commenced and had proceeded for some two weeks, it seems that the taxpayer took the view that if the Commissioner wished to make a case different from that which was particularised, it was necessary for the Commissioner to seek leave to amend his particulars.

34 On 21 August 2002 and approximately one week before the hearing finished, the Commissioner wrote to the taxpayer’s solicitors advising that leave would be sought to amend the particulars supplied. The amended particulars described the scheme in the same terms as originally described. However, the particulars referred to there being additional deductions to be taken into account. The additional deductions referred to were deductions to MS3 for its share of the research and development expenditure and interest and a deduction by Macquarie Finance for the interest incurred by it in the 1992 to 2000 years of income in respect of the deposit made by Luminis with Macquarie Finance. The letter noted that the Commissioner had not made a determination to cancel any tax benefits other than those the subject of the proceedings.

35 The matter of amendment of particulars was subsequently dealt with by the Tribunal and the amendment allowed by consent after the Commissioner had given an undertaking not to issue further determinations under Part IVA in respect of the additional deductions referred to and which were not directly the subject of the proceedings before the Tribunal.

36 The Commissioner in due course tendered to the Tribunal extensive written submissions which dealt, inter alia, with Part IVA. These submissions made reference to the tax benefits obtained from the scheme as being not merely those that were the subject of the proceedings but also the additional benefits to MS3 and Macquarie Finance particularised. The submissions referred to ‘fiscal benefits to MBL Group’ including MS3 and Macquarie Finance. It was pointed out that the total of these deductions amounted to approximately $71,825,000 with the consequence being that companies in the Macquarie Group would pay approximately $28,011,750 less in tax than otherwise would be paid if the scheme had not been entered into or carried out. It was conceded that it may be that this figure should be reduced, having regard to the interest payable by MS3 in favour of MAL (another Macquarie Group company) which would be assessable income and the fact that set-up costs and management fees which, while deductible, were payable in favour of MBL and thus assessable to it. It was also conceded that it could also be necessary to reduce the figure further by another $6,885,917 but even so, it was submitted, there was a fiscal benefit to the group of in excess of $21,000,000.

37 The written submissions considered in some detail the seven matters referred to in s 177D(b). The fourth of those matters concerned the result in relation to the operation of the Act but for the operation of Part VIA. The written submissions referred to the expenditure by MS3 of $15,196,500 and $178,827 and interest in favour of MAL but only such interest as was the subject of determinations. Curiously no reference was made in the written submissions under this heading to the interest incurred by Macquarie Finance.

38 It is clear, however, that the substance of the submission was that the conclusion which the Tribunal should draw was one involving balancing against such commercial advantages as might be gained by the Macquarie interests from the scheme, the various tax benefits referred to in Annexure A of the respondent’s written opening. Annexure A included the taxpayer’s share of the actual research and development costs, the deduction on the borrowing from MAL of $10,890,000 accumulating by capitalised interest to $28,400,000 and interest incurred by Macquarie Finance on the deposit by Luminis of $27,225,000. It is unnecessary to detail the oral submissions made by the Commissioner. It suffices only to say that what senior counsel for the taxpayer there referred to as a ‘new matter’ was dealt with, not merely by senior counsel for the Commissioner in his submissions but also by senior counsel for the taxpayer in his closing submissions.

39 In summary, there is no doubt that the case put before the Tribunal on behalf of the Commissioner included a case that, in addition to the tax benefits that were the subject of the present proceedings, there were other tax benefits obtained from the scheme by MS3, namely the research and development expenditure and deductions for interest on the loan advanced by MAL to MS3 and interest on the deposit from Luminis to Macquarie Finance. I did not understand senior counsel for the taxpayer really to contest the submission that the Commissioner had advanced this case. Rather, the question before us was whether the Tribunal had dealt with this alternative case.

Did the Tribunal fail to consider the submission?

40 At the outset of the Tribunal’s reasons so far as they concerned Part IVA, the Tribunal said (at [141]):

‘In the latter stages of the hearing there was, however, disagreement between the parties over the particularisation of the scheme by the Respondent and which tax benefits derived from the scheme were at issue in these proceedings. Initially, the Respondent only identified two tax deductions: the core technology licence fee and the interest component of the R and D. Latterly, the Respondent sought to identify other tax benefits as part of the scheme, in particular, the R and D expenditure in relation to MS3 and benefits accruing to Macquarie Finance. Ultimately, the parties came to an understanding, with the Respondent giving assurances that there would be no further determinations made giving rise to adjustments in relation to the other tax benefits.’

41 That comment clearly shows that the Tribunal was aware of the amended particulars.

42 It may be noted here that the definition of ‘scheme’ in s 177A(1) of the Act is in two parts. The first part is concerned with what may be called agreements or understandings, although it extends to promises or undertakings. This first part can loosely be said to involve a meeting of minds. The second part of the definition is essentially concerned with actions. It includes both ‘acts’ and ‘series of acts’. This second part of the definition does not require any meeting of minds. It hardly seems to add to the definition of scheme on the facts of a particular case the action of making a claim for a relevant tax deduction. If the scheme stopped short of the making of the claim for the deduction, presumably the deduction would, apart from Part IVA in any event be allowable. An amount does not become an allowable deduction just because it is claimed as such in a taxpayer’s return of income. No doubt the making of a claim draws the Commissioner’s attention to the allowable deduction. But it is sufficient for the purposes of Part IVA for a deduction to be a tax benefit that it is, apart from Part IVA, allowable as a deduction. It is immaterial whether it is in fact allowed. It is for this reason that the Commissioner expressed the error of law alternatively to be the Tribunal’s failure to consider the Commissioner’s alternative case, as contrasted with the Tribunal’s failure to consider what was said to be an alternative scheme.

43 Under the heading ‘The second issue is whether a taxpayer obtained a tax benefit in relation to the scheme’, the Tribunal said at [143]:

‘The Applicant does not dispute that the transaction was structured in a way that enabled MS3 to obtain the deductions for which the Act specifically provided (Applicant's Submissions, p46, para186). The Applicant's submissions accept that the tax deductions which are the subject of these proceedings constituted a tax benefit to MS3. The Applicant's objection in the latter stages of the hearing was to the Respondent changing its particularisation of the scheme by including reference to tax benefits accruing to Macquarie Finance. In the Tribunal's view, the more important question is the dominant purpose of the scheme.’

44 It is not clear what the Tribunal meant by the last sentence.

45 The Tribunal then continued at [144]:

‘In his submissions, the Respondent submitted that the allowable deduction of $15,196,500 claimed by MS3 in respect of the acquisition of the core technology licence by the Syndicate from Luminis was a tax benefit to MS3 in connection with the scheme in the subject year of income, within the definition of tax benefit in s 177C(1)(b). The Respondent further submitted that the allowable deduction of $178,098 claimed by MS3 was core technology expenditure, being interest referable to that part of a loan from MAL to MS3 that was used by MS3 in connection with the acquisition of the core technology licence from Luminis for $15,196,500, and a tax benefit to MS3 in connection with the scheme in the subject year of income, as defined in s 177C(1)(b).’

46 In this paragraph the Tribunal seems clearly to restrict its consideration only to the tax benefits that are the subject of the proceedings and to ignore the additional tax benefits relied upon in the Commissioner’s alternative case.

47 The Tribunal then turned to consider the seven matters in s 177D(b) in order to decide whether it would be concluded that a person or persons who entered into or carried out the scheme or any part thereof did so for the purpose or dominant purpose of enabling the relevant taxpayer or the relevant taxpayer and others each to obtain a tax benefit. The first part of this section of the reasons was concerned with a discussion of the law. That discussion is unexceptionable. Thereafter, the Tribunal dealt with various factual matters relevant to what one might refer to as commercial considerations. The fourth matter it was required by s 177D(b)(iv) to consider were the results obtained under the Act but for the operation of Part IVA. Of this and the matters referred to in s 177D(b)(v) and (vi) the Tribunal said (at [168]):

‘The result achieved, but for the operation of Part IVA (subparagraph (iv)), is the deductions under challenge. The relevant taxpayer - MS3 - will incur a substantial loss in the subject year of income as a result of the scheme (subparagraph (v)). The scheme involved a number of other parties (subparagraph (vi)), detailed above, including Luminis which, like Bresatec, originally owned part of the relevant intellectual property and, unlike Bresatec, had the benefit of tax-exempt status, MAL which funded MS3's participation in the syndicate and, one assumes, would have been liable to pay tax on the interest earned, Macquarie Finance which acted as the deposit holder and, presumably, reinvested the money deposited to earn interest, thereby incurring a tax liability, and Bresatec which conducted the research and, ultimately, was called upon to honour the put option.’

48 It is evident from [168] that the Tribunal considered only the deductions that were the subject of the proceedings under subparagraph (iv) of s 177D(b). The reference in [168] to both MAL and Macquarie Finance having taxable income being interest earned appears not to have been considered by the Tribunal under subparagraph (iv) but under subparagraphs (v) and (vi). This may not be surprising having regard to the way the Commissioner advanced his submissions before the Tribunal.

49 The Tribunal’s conclusions under s 177D are set out in [170] and [171] of the Tribunal’s reasons. These paragraphs read as follows:

‘170. In conclusion, the Tribunal finds that the tax deductions facilitated by s 73B and s 73CA of the Act were important influences on how the scheme was structured, and on MBL through the involvement of its wholly owned subsidiary companies. Clearly, the Government intended tax deductions to be an incentive to encourage private investment in R and D. However, while obtaining a tax benefit in connection with the scheme was undoubtedly an important purpose of the scheme, the Tribunal finds that a reasonable person would conclude that it was not the dominant purpose.

171. MBL is in the business of banking, finance and investment. In this case, it decided to invest in the Syndicate and, in the Tribunal's view, the evidence supports a finding that this investment was its dominant purpose. The extent of Mr Phillips' involvement in the project both in the period before the finalisation of the terms of the transaction on 30 June 1992/1 July 1992 and in the three year period afterwards, and his stated reasons for this, described above, supports this conclusion. Mr Phillips' evidence is, in turn, supported by that of Dr Smeaton and the Applicant's other witnesses who attested to the Bresatec team's optimism about the successful commercialisation of the transgenic pig technology. The events under consideration took place against the backdrop of the Government's tax incentives for such investments. As Hely J recognised in Hart (supra) at paragraph 83, ‘Where the line is drawn is a matter of degree, having regard to the eight factors itemised in s 177D’. Having had regard to those factors, the Tribunal finds in favour of the Applicant.’

50 It is obvious that the reference to tax deductions in [170] is only to deductions under s 73B, being research and development expenditure deductions but not to deductions by way of interest. The reference to s 73CA in [170] is, however, a reference to the deduction for research and development available to MS3 ie the license for the core technology, for s 73CA is relevantly concerned only with that deduction.

51 As is obvious from the quotations from the Tribunal’s reasons set out above the Tribunal member was aware that the Commissioner sought to have considered not merely the deductions for interest and the core technology licence fee that were the subject of the proceedings but the additional deductions mentioned in the amended particulars. However, it is difficult to conclude other than that the Tribunal regarded the case it had to decide as one limited to the deductions the subject of the proceedings. Particularly, what the Tribunal did not do, as senior counsel for the Commissioner submitted it should have done, for the purposes of s 177D, was weigh against the objective factual matters which may be referred to as commercial, the entirety of the deductions available to the Macquarie entities as comprehended not merely by those that were the subject of the proceedings before the Tribunal but also the additional deductions referred to by the Commissioner in the amended particulars. It is therefore with some regret that I would conclude that the Tribunal erred in not considering the submission advanced by the Commissioner and in consequence erred in law.

52 It may well be that the Tribunal’s failure to consider the submission advanced by the Commissioner is related to the second matter complained of by the Commissioner, namely, the application by the Tribunal of the wrong test as to purpose. It is to this that I now turn.

Submissions Concerning Purpose

53 Section 177D requires the finder of fact to reach a conclusion whether there is a person who entered into or carried out the scheme or any part of if it for the purpose (or the dominant purpose) of enabling the relevant taxpayer or that taxpayer and another taxpayer or taxpayers each to obtain a tax benefit in connection with the scheme. However, it is clear from the terms of the section itself that that conclusion is one that must be reached having regard to the eight matters stipulated in s 177D(b) and no other matters. It follows that while the conclusion required to be drawn is one that requires consideration of the purpose or dominant purpose of a person, including the taxpayer, that conclusion can not take into account evidence of the actual purpose of a taxpayer or other person, save and except so far as that could be forensically relevant to any one of the matters specifically referred to in s 177D(b) for example, the manner in which the scheme was entered into. None of the eight matters refer to the actual purpose of any person. It also follows that generally, at least, evidence of what may be referred to as the actual or subjective purpose of the taxpayer is irrelevant. However, it may well be the case, as in the present circumstances, that evidence of subjective purpose might be admissible for the purpose of the determining some other issue in the case, for example, here, the provisions dealing with deductions for research and development expenditure. The nature of the conclusion required by s 177D is discussed in the decision of the Full Court of this Court in Eastern Nitrogen Ltd v Commissioner of Taxation (2001) 108 FCR 27 at 44-45 per Carr J (with whom Lee and French JJ agreed) and see also Hart v Commissioner of Taxation (2002) 196 ALR 636 at [55] and Consolidated Press Pty Ltd v Federal Commissioner of Taxation (2001)179 ALR 625at [95].

54 It is sometimes said that the conclusion under s 177D is a conclusion of objective purpose. That way of putting it is correct if what is meant by it is that the conclusion is not one drawn from evidence of the actual purpose of the relevant taxpayer or other taxpayers. It may perhaps contribute to confusion if it is suggested that the conclusion to be drawn is other than a conclusion about the actual purpose of the taxpayer. Particularly, the conclusion required to be drawn is not a conclusion about the transaction itself but the state of mind of a person. To this extent Part IVA differs from the previous general anti-avoidance provision (s 260) which was concerned inter alia with the purpose of the contract agreement or arrangement of the kind to which the section referred and not the purpose of a person party thereto.

55 There was no dispute between the parties to the appeal concerning the correct test to be applied. The dispute was as to whether the Tribunal had applied this test.

The Submission made to the Tribunal

56 A perusal of the submissions, whether oral or in writing, made to the Tribunal, makes it clear that senior counsel for the Commissioner and senior counsel for the taxpayer both stated expressly the proper test to be applied and particularly made it clear that the question for decision by the Tribunal was not one to be decided by reference to evidence of the subjective purpose of the taxpayer.

57 This is not to say that the matter was always put accurately in the submissions. Senior counsel for the taxpayer, for example, said on day 12, ‘[o]ne has to look at the scheme identified by the Commissioner and say whether the purpose of that scheme is to derive a benefit.’ Of course, comments of this kind must be read in context and the context there was an argument seeking to reject what the proponents of it refer to as ‘causative purpose’.

58 One quotation from the oral submissions of senior counsel for the Commissioner suffices to put the submission made by the Commissioner on this point clearly. On day 13 (transcript reference 1114) senior counsel for the Commissioner said:

‘The process of identifying dominant purpose is objective. S 177D(b) is not concerned with the subjective intention or the subjective purpose of a party to a scheme. So this case cannot be decided by Mr Phillips asserting, as he does in his evidence, that he went into this intending to hopefully share in the great rewards that might eventuate. One has to look at the surrounding circumstances, but that degree of subjectivity can’t prevail.’

The Tribunal’s Reasons for Decision

59 At the outset of the learned member’s discussion on s 177D there are set out quotations from various judgments, including that of the Full Court of this Court in Peabody v Commissioner of Taxation (1993) 40 FCR 531 at 542, and from the judgment of the High Court in Commissioner of Taxation v Spotless Services Ltd (1996) 186 CLR 404 at 415; quotations consistent with a correct understanding of the position, namely that the relevant question for determination is not one to be reached by reference to the evidence of the subjective purpose of the tax payer or any other person. So at [151] the Tribunal said:

‘…the issue,… is whether having regard to the matters set out in subparagraphs (i) to (viii) of s 177D(b), a reasonable person would conclude that the taxpayers entered into or carried out the scheme with the dominant purpose of obtaining a tax benefit in connection with the scheme.’

60 That statement which is but a paraphrase of the words of the section is unexceptionable. However, immediately afterwards the Tribunal said (at [153]):

‘Relying on the evidence of Dr Smeaton, Dr Seamark and Mr Hart, the Tribunal finds that Bresatec's objective, and that of Luminis, was to raise R and D funding to finance ongoing research on transgenic pigs and ESC technology.

61 The Tribunal then discussed some of that evidence, including the evidence of Mr Phillips who was employed in the Corporate Finance and Leasing Services Division of MBL and who could be seen to be the relevant mind of the taxpayer in respect of the project. The learned Tribunal member at [162] noted that both university research scientists and employees of Bresatec such as Dr Robins and Dr Smeaton were optimistic about the transgenic and the embryo stem cell technology and the chances of its successful commercialisation. The Tribunal then said (at [163]):

‘Again, while it is easy to be sceptical in hindsight, the Tribunal is not satisfied that there is any evidence to suggest MBL's motives were other than as stated by Mr Phillips. For example, Mr Phillips said he attended and chaired all but one of the quarterly meetings held in the period 13 January 1993 to 21 July 1995. In the Tribunal's view, such conduct is consonant with this being a genuine investment by MBL. With the benefit of the knowledge that the Syndicate was not ultimately successful, the Respondent has sought to impute a different motive to MBL from the terms of the transaction. However, it is clear from Dr Smeaton's evidence that the R and D was a technical success and that it was only when regulatory approval was not forthcoming in 1995/1996 that commercialisation was put on hold.’

62 After considering, in some details, Mr Phillips’ evidence, the Tribunal turned to consider the various matters in subparagraphs (i) – (viii) of s 177D(b). The Tribunal then set out its findings at [170] and [171] of its reasons. These paragraphs read as follows:

‘170. In conclusion, the Tribunal finds that the tax deductions facilitated by s 73B and s 73CA of the Act were important influences on how the scheme was structured, and on MBL through the involvement of its wholly owned subsidiary companies. Clearly, the Government intended tax deductions to be an incentive to encourage private investment in R and D. However, while obtaining a tax benefit in connection with the scheme was undoubtedly an important purpose of the scheme, the Tribunal finds that a reasonable person would conclude that it was not the dominant purpose.

171. MBL is in the business of banking, finance and investment. In this case, it decided to invest in the Syndicate and, in the Tribunal's view, the evidence supports a finding that this investment was its dominant purpose. The extent of Mr Phillips' involvement in the project both in the period before the finalisation of the terms of the transaction on 30 June 1992/1 July 1992 and in the three year period afterwards, and his stated reasons for this, described above, supports this conclusion. Mr Phillips' evidence is, in turn, supported by that of Dr Smeaton and the Applicant's other witnesses who attested to the Bresatec team's optimism about the successful commercialisation of the transgenic pig technology. The events under consideration took place against the backdrop of the Government's tax incentives for such investments. As Hely J recognised in Hart (supra) at paragraph 83, ‘Where the line is drawn is a matter of degree, having regard to the eight factors itemised in s 177D’. Having had regard to those factors, the Tribunal finds in favour of the Applicant.’

63 There is ambiguity in these last two paragraphs. Putting aside any objection to a reference to the purpose of the scheme rather than the purpose of a person (a reference perhaps to the submission of counsel for the taxpayer quoted above), [170] of the reasons is capable of being read as concerned only with objective matters. It is [171] that presents the greatest difficulty. It can be read as support for the view that Mr Phillips’ subjective purpose was taken to be a matter relevant in reaching a conclusion about the taxpayer’s purpose. This is particularly so when it is read with the summary of Mr Phillips’ evidence noted earlier. If this is the way the Tribunal’s reasons should be read, then it clearly demonstrates error on the part of the Tribunal in applying the wrong test.

64 It is not necessary in the view I take of the first issue in the appeal for me to determine whether the Tribunal took into account impermissibly the state of mind of the taxpayer or of any other person. It is possible, given that the Tribunal appears initially to have appreciated the correct issue, that statements such as those in [171] of the reasons are merely a result of loose language. It seems inconceivable, having regard to the fact that the relevant tests were clearly expressed by counsel for both parties and initially by the Tribunal itself ignored these submissions and its own summary of the law and thus proceeded to apply the wrong test. My view has fluctuated on the matter. However, not without some doubt I have concluded that the Tribunal did apply the wrong test in stating its conclusion as to purpose and accordingly for this reasons too the decision must be set aside.

Should the Court Itself Affirm the Assessment?

65 Senior counsel for the Commissioner submitted that the Court should not merely set aside the decision of the Tribunal but also order that the application to the Tribunal be dismissed and the assessment affirmed. He submitted that this was the only outcome open.

66 With respect to the submission, this is not a case where it could be said that only one outcome was possible, namely that which favours the Commissioner. Part IVA of the Act clearly requires a conclusion to be drawn by reference to the matters set out in s 177D(b). Those matters are factual and the conclusion required to be drawn is itself a conclusion of fact. It would be necessary for the Court on appeal to consider all of the evidence before the Tribunal, from a hearing which extended over some three weeks, before it could be in a position to decide whether only one outcome was possible. This I decline to do for it is clear from the Tribunal’s reasons and particularly its factual findings (excluding matters of subjective purpose) that it would be possible to reach either a conclusion favourable to the Commissioner or one favourable to the taxpayer.

67 It is for the Tribunal and not the Court to decide factual matters and it is for the Tribunal to undertake the task of determining whether to draw the conclusion which s 177D requires to be drawn.

The Orders to be Made

68 Senior counsel for the taxpayer submitted that if the Court were to decide the appeal adversely to his client, the Court should remit only that part of the matter as related to Part IVA to the Tribunal. It was conceded, having regard to the decision of Minister for Immigration and Multicultural Affairs v Wang (2003) 196 ALR 385, that the Court should not order that the matter be remitted to a Tribunal constituted by the same member as had heard the original application.

69 Section 44(1) of the AAT Act permits, as already noted, a party to a proceeding before the Tribunal to appeal on a question of law from any decision of the Tribunal in that proceeding. In the present case the relevant decision was that the objection decision under review be set aside and in its place there be substituted a new decision allowing the applicant’s objection.

70 The jurisdiction of the Court to hear and determine the appeal is provided for in s 44(3) of that Act. Subsection (4) and (5) of the same section then provide:

‘(4) The Federal Court of Australia shall hear and determine the appeal and may make such order as it thinks appropriate by reason of its decision.

(5) Without limiting by implication the generality of subsection (4), the orders that may be made by the Federal Court of Australia on an appeal include an order affirming or setting aside the decision of the Tribunal and an order remitting the case to be heard and decided again, either with or without the hearing of further evidence, by the Tribunal in accordance with the directions of the Court.’

71 Subsection (6) of the same section provides that if an order is made remitting the case to be heard and decided again by the Tribunal, the person who made the decision to which the appeal relates need not constitute the Tribunal for the hearing.

72 It is clear from the requirement that the appeal to the Court is limited to a question of law that the Court’s ‘determination’ will be a determination of and limited to that question of law. The power of the Court to make orders, however, is granted in wide terms and is limited only by the requirement that the Court, acting judicially must think the orders appropriate, having regard to the decision the Court has reached. The expression ‘by reason of its decision’ delimits ‘the general power to make such determination as it thinks appropriate. That is, orders can only be made if they are appropriate by reason of the decision on the point of law’: Morales v Minister for Immigration and Multicultural Affairs (1998) 82 FCR 374 at 386-7, citing Minister for Immigration and Ethnic Affairs v Gungor (1982) 63 FLR 441 at 454-455; Director-General of Social Services and Health v Hangan (1982) 70 FLR 212 at 223.

73 In Wang the Full Court of this Court had remitted a decision to the Tribunal to be determined in accordance with law. However, it granted liberty to apply in the event that there was dispute over the composition of the Tribunal. The Court had done so because of a concern that if the matter were to be heard by a Tribunal differently constituted the respondent might be deprived of favourable findings made by the Tribunal as originally constituted. When the matter was remitted to the Tribunal it was in fact constituted by a different member. For that reason the liberty to apply was exercised and an order was thereafter made by the Full Court remitting the matter to the Tribunal as originally constituted. The question whether such an order could or should be made was raised by an appeal to the High Court by the Minister, whose appeal was allowed by Gleeson CJ, McHugh, Gummow and Hayne JJ (Kirby J dissenting).

74 Wang arose under the Migration Act 1958 (Cth) (‘the Migration Act’). It was conceded that the Court had power to order on remittal to the Tribunal that the matter be heard by a Tribunal differently constituted. Gleeson CJ indicated that his Honour was of the view that the Court had power to remit the matter to the member who had originally heard it but thought that the propriety of the exercise of such a power as a matter of judicial discretion and comity was another matter. His Honour made it clear that questions such as costs or efficiency might, in a particular case, dictate that a matter remitted should be heard by the original member. His Honour pointed out that necessarily, after remission, the Tribunal was obliged to undertake a further review of the delegate’s decision and the information before it could differ from that before the original decision maker. The mere fact that the original decision maker would be likely to maintain the original factual findings if no other information was presented did not require the order in fact be made. The Chief Justice refrained from deciding whether the result sought could have been achieved by an order of the Court limiting the matter the subject of the hearing.

75 McHugh J took the view that while under the Migration Actthe Court was given express power to give directions, that express power did not carry with it a power to give directions inconsistent with an express provision of the Migration Act. The Migration Actitself contained express provision authorising the principal member of the Tribunal in question to give a written direction as to the composition of the Tribunal for the purposes of a particular review. Thus, directions could not be given which would conflict with the specific power conferred on the principal member.

76 His Honour left open the question whether the Court could give a direction requiring the Tribunal to treat certain facts as established. His Honour pointed out that the facts that existed at the time of the Tribunal’s reconsideration may not be the same as those which existed at the time of the initial hearing. His Honour referred to the problem that the Tribunal might be embarrassed by a direction which could hamper the ability of the Tribunal to determine the case as at the date of its decision.

77 Gummow and Hayne JJ were likewise of the view that whether or not the Court had power to order the matter to be determined by the Tribunal constituted as it was originally, it was inappropriate to exercise that power. Their Honours pointed to the difficulties that would flow from an attempt to preserve certain factual findings from reconsideration in the event a matter was remitted to the Tribunal. Reference was made to the fact that the question before the Tribunal (there whether the applicant was a person to whom Australia owed protection obligations) was a matter to be determined at the time the Tribunal made its decision. So if the matter were remitted necessarily different facts could emerge on the remitter.

78 It is true that there are some differences between the provisions of the AAT Act on the one hand and the Migration Acton the other. However, there are also some similarities. Subject to certain provisions not presently relevant, the composition of the AAT, like the composition of the Refugee Review Tribunal, is one to be determined by a specified person, here the President. Further, it is clear that the Tribunal’s decision necessarily is to be given by reference to the state of affairs existing at the time of making the decision, so that, at least theoretically, relevant facts could alter between the making of an initial decision and the making of a decision after the matter has been remitted.

79 There is another question in the present case. The jurisdiction of this Court being limited to questions of law only, the orders the Court might make as a result of its decision must, as earlier noted, be such as are appropriate by reason of the decision it has made on the questions of law. The Court’s reasons have been limited to questions of law related to what may be referred to as the Part IVA issue. The decision of the Court involves the setting aside of the Tribunal’s decision, that being a decision reached on a review of the disallowance of the taxpayer’s objection. It may be argued that the decision that the Tribunal is empowered to review and which constitutes the matter before it can not readily be divided into separate decisions or parts of decisions, notwithstanding that there were two separate issues which the Tribunal discussed. Whether this is correct need not detain us here. But it is relevant to note that the Court’s exercise of discretion to make orders must necessarily take into account the fact that the ultimate decision will need to be given having regard to facts before the Tribunal when it ultimately comes to make its decision. This is not to say that if the matter were to be returned to the same member that member would necessarily need to embark on a reconsideration of matters already decided. Indeed, the questions of efficiency and cost would likely be taken into account. Nor does this mean that a member of a Tribunal differently constituted would necessarily need to rehear the whole of the evidence. The Tribunal’s procedure is sufficiently flexible to avoid that course. Regard would no doubt be had, in determining the course the Tribunal would follow, to the fact that not only had the research and development issue been initially determined but also that the Commissioner had withdrawn in this Court any ground of appeal on a question of law related to the decision on that issue.

80 While there could be some efficiency in seeking to avoid a rehearing of the evidence related to the research and development issue I am of the view that it would be inappropriate for this Court in remitting the matter to the Tribunal to specifically exclude from consideration by the Tribunal that issue, even if the Court does have power to do this, a matter I do not need to decide. Ultimately the constitution of the Tribunal will be a matter for the President and essentially Parliament has entrusted to the Tribunal the task of reviewing decisions which may be referred to it and on the basis that the procedure which the Tribunal will adopt will be a matter for the Tribunal as so constituted.

81 Accordingly, the appropriate order is to set aside the Tribunal’s decision and to remit the matter to a Tribunal to be reheard in accordance with law. The taxpayer shall pay the Commissioner’s costs of the appeal to this Court.

|

I certify that the preceding eighty-one (81) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Hill. |

Associate:

Dated: 24 October 2003

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

N 1029 OF 2002 |

ON APPEAL FROM THE ADMINISTRATIVE APPEALS TRIBUNAL

|

BETWEEN: |

COMMISSIONER OF TAXATION APPELLANT

|

|

AND: |

ZOFFANIES PTY LIMITED RESPONDENT

|

|

JUDGES: |

HILL, HELY & GYLES JJ |

|

DATE: |

24 OCTOBER 2003 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

HELY J:

82 I have had the advantage of reading the reasons for judgment of Hill J and Gyles J in draft form. I would uphold the Commissioner’s appeal on both of the issues identified by Hill J in par [19] of his reasons for decision.

83 I agree with Hill J’s reasons for concluding that the Tribunal ignored the additional tax benefits relied upon in the Commissioner’s alternative case, and in consequence erred in law. Sections 177D(b)(vi), (vii) and (viii) of the Act obliged the Tribunal to have regard to these matters in deciding whether the conclusion referred to in s 177D(b) should be drawn. The Tribunal did not do so.

84 I agree with Gyles J’s reasons for concluding that the Tribunal applied the wrong test in stating its conclusions as to purpose. I agree with Hill J’s observation at par [52] that it may well be that there is a relationship between the two errors. That this may be so is demonstrated by the following passage in the Tribunal’s reasons:

‘143. The Applicant’s submissions accept that the tax deductions which are the subject of these proceedings constituted a tax benefit to MS3. The Applicant’s objection in the latter stages of the hearing was to the Respondent changing its particularisation of the scheme by including reference to tax benefits accruing to Macquarie Finance. In the Tribunal’s view the more important question is the dominant purpose of the scheme.’ (emphasis added)

85 The tax benefits accruing to Macquarie Finance was a matter to which the Tribunal was bound to have regard in determining what was the dominant purpose of person(s) who entered into or carried out the scheme.

86 I agree with the form of orders proposed by Gyles J, and with his Honour’s reasons for concluding that the Tribunal’s decision should be set aside only insofar as it relates to the Part IVA issue, which should be remitted to the Tribunal for redetermination.

|

I certify that the preceding five (5) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Hely. |

Associate:

Dated: 24 October 2003

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

N 1029 OF 2002 |

ON APPEAL FROM THE ADMINISTRATIVE APPEALS TRIBUNAL

|

BETWEEN: |

COMMISSIONER OF TAXATION APPELLANT

|

|

AND: |

ZOFFANIES PTY LIMITED RESPONDENT

|

|

JUDGES: |

HILL, HELY & GYLES JJ |

|

DATE: |

24 OCTOBER 2003 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

GYLES J:

87 I have had the advantage of reading the judgment of Hill J in draft. I need not repeat how the issues arise. I agree with Hill J that the appeal ought to be allowed, and that the matter should be remitted to the Administrative Appeals Tribunal (‘the Tribunal’) although, as will appear, I have a different view as to the precise form of remitter. In my opinion, the Tribunal took into account findings as to the actual purpose and motive of the taxpayer in considering the purpose of the taxpayer as provided by s 177D(b) of the Income Tax Assessment Act 1936 (Cth) (‘the Act’). That was an error of law which properly gives rise to an appeal on a question of law within the meaning of s 44 of the Administrative Appeals Tribunal Act 1975 (Cth).

88 I acknowledge that the reasons of the Tribunal referred to authorities which correctly explained the application of s 177D and that the Tribunal initially stated the correct issue for decision. I accept without hesitation the necessity to avoid a pedantic approach to the reasons of the Tribunal as required by the well-known authorities referred to by Hill J. However, in my respectful opinion, the reference by the Tribunal to actual motive or purpose in its reasons is too clear and too persistent to be disregarded as loose language.

89 Attention on the appeal has, naturally, focused upon the findings in relation to the taxpayer, but it should not be overlooked, as pointed out by Hill J, that the opening sentence of the Tribunal’s consideration of the facts relevant to the application of Pt IVA was as follows (at [153]):

‘Relying on the evidence of Dr Smeaton, Dr Seamark and Mr Hart, the Tribunal finds that Bresatec’s objective, and that of Luminis, was to raise R and D funding to finance ongoing research on transgenic pigs and ESC technology.’

90 The evidence of Mr Phillips was dealt with (with some interpolations) between [156] and [165] of the reasons of the Tribunal, including the statement:

‘[T]he Tribunal is not satisfied that there is any evidence to suggest MBL’s motives were other than as stated by Mr Phillips.’

Mr Phillips is again referred to in the paragraph of the reasons which explains the conclusion that obtaining a tax benefit was not the dominant purpose of the taxpayer. Hill J has set out [170] and [171], and I need only refer to part of [171]:

‘MBL is in the business of banking, finance and investment. In this case, it decided to invest in the Syndicate and, in the Tribunal’s view, the evidence supports a finding that this investment was its dominant purpose. The extent of Mr Phillips’ involvement in the project both in the period before the finalisation of the terms of the transaction on 30 June 1992/1 July 1992 and in the three year period afterwards, and his stated reasons for this, described above, supports this conclusion.’ (emphasis added)

In my respectful opinion, there is no ambiguity in this explanation. I conclude that the Tribunal not only took into account the evidence of Mr Phillips as to his subjective motives and purposes, but that this was a critical factor in the decision of the Tribunal.

91 I should add that I have no great surprise at the nature of the error. The difference between the actual purpose of a taxpayer, on the one hand, and the purpose which is to be imputed to the taxpayer based upon an exclusive set of criteria, on the other hand, is not without subtlety and has been misunderstood before. Consideration of the written submissions in reply to the Tribunal on behalf of the taxpayer as to purpose in relation to s 177D (particularly at [60] and [61]) underlines the point and may well have been misunderstood.

92 The other basis for the appeal put forward on behalf of the Commissioner is more problematic. There is a good deal to be said for the view that the Tribunal did not fully analyse, consider and take into account the tax implications of the scheme for what might be called the Macquarie Group as a whole. It is, however, by no means clear that the Tribunal was bound, as a matter of law, to do so. I find it difficult to regard the claiming or receiving of tax benefits as part of a scheme for relevant purposes, rather this would be the result of the operation of the scheme. It is also difficult to regard the concept of tax benefit in s 177D as extending beyond the tax benefit in issue. Thus, to be relevant, the issue must be tied back to purpose and so to the enumerated heads in s 177D(b). It may be that subs (vi), (vii), (viii) would provide a nexus. It is a large step from such a nexus to a conclusion that there was any error of law involved in the manner in which the Tribunal considered these sub-paragraphs. Each was specifically addressed by the Tribunal in its reasons. An error in doing so would normally be factual. An administrative tribunal is not bound to deal with all factual matters proposed by a party as relevant to a topic in the manner put forward to it. Put another way, the statute only requires consideration of the topic, not pieces of evidence relating to it.

93 The contention that this issue (in its various forms) does not involve an appeal on a question of law was distinctly taken in the taxpayer’s written submissions, and was repeated at the outset of the oral submissions for the taxpayer. Whether or not the error alleged here would be of fact or law is of some nicety, a decision as to which would involve consideration of a good deal of authority, not all of which is easy to reconcile. As the matter is to be remitted for further hearing and determination by the Tribunal, I do not need to make that decision. The parties will be free to clearly put to the Tribunal what each says about the matter at that stage.

94 I agree with Hill J that it would not be appropriate for this Court to determine the Pt IVA issue, and do not wish to add anything as to that. However, I would favour setting aside the Tribunal’s decision only insofar as it relates to Pt IVA, and would remit that issue for determination. I am in no doubt that that is the appropriate result if it can be achieved. The Pt IVA issue was distinct and severable from the other issues, all of which were decided favourably to the taxpayer. The Commissioner did not pursue an appeal against any of those favourable findings. In my view, they should be regarded as closed. Indeed, it is still an open question as to whether such findings by the Tribunal might constitute the equivalent of cause of action estoppel or issue estoppel (cf Miller v University of New South Wales [2003] FCAFC 180 per Ryan and Gyles JJ at [48]-[75], particularly [61]). Whether that be so or not, it is undesirable to facilitate the reopening of those issues. To do so would involve all of the evils involved in re-litigation of issues already determined, including time and cost and the possibility of inconsistent decisions. It is commonplace in relation to appeals in the Court system to set aside only part of the judgment below, and remit part of a matter for rehearing, although only one cause of action is involved. A new trial of an action for negligence limited to damages is a commonplace example.

95 In my opinion, the provisions of ss 44(4) and (5) of the Administrative Appeals Tribunal Act 1995 (Cth) provide ample power to achieve the same result. There is no reason to read down those sections beyond the limitations explained in Minister for Immigration & Ethnic Affairs v Gungor (1982) 42 ALR 209 at 220, approved of by Gleeson CJ, McHugh, Gummow and Hayne JJ in Minister for Immigration & Multicultural Affairs v Thiyagarajah (2000) 199 CLR 343 at [34]. Indeed, consistently with Gungor, it is necessary to relate the orders made to the error of law which has been established. In this case, that error only relates to Pt IVA. I note that it was recognised in Thiyagarajah at [35] that affirming part of a decision and setting aside another part of the decision is an example of a situation which may call for special orders under provisions of this kind.

96 The orders of the Court should be:

1. Appeal allowed.

2. The decision of the Tribunal is set aside insofar as it found that the provisions of Pt IVA of the Income Tax Assessment Act 1936 (Cth) (‘the Act’) did not apply to the circumstances of the case such as to support the income tax assessment dated 14 November 2000 for the substituted accounting period ending on 30 September 1992 (‘the assessment’) against which the taxpayer’s objection in issue was lodged.