FEDERAL COURT OF AUSTRALIA

Blank v Commissioner of Taxation [2014] FCA 87

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

Applicant | |

|

AND: |

Respondent |

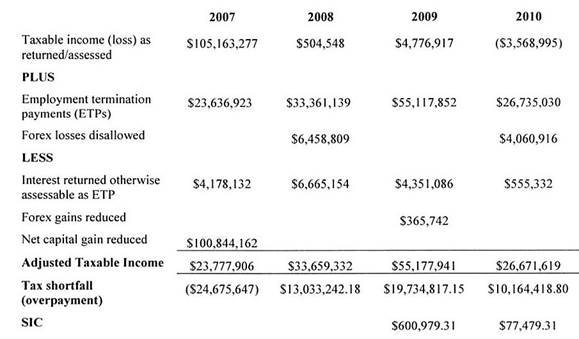

|

DATE OF ORDER: |

|

|

WHERE MADE: |

THE COURT ORDERS THAT:

1. On or before 4:00 pm on Wednesday, 26 February 2014, the parties provide short minutes of order to give effect to these reasons by way of email to my chambers. If the parties cannot agree on the form or terms of the orders, on or before the same time and date, each party provide short minutes of order by way of email to my chambers.

2. The matter be listed for pronounciation of orders on Thursday, 27 February 2014 at 2:15 pm.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 1913 of 2012 |

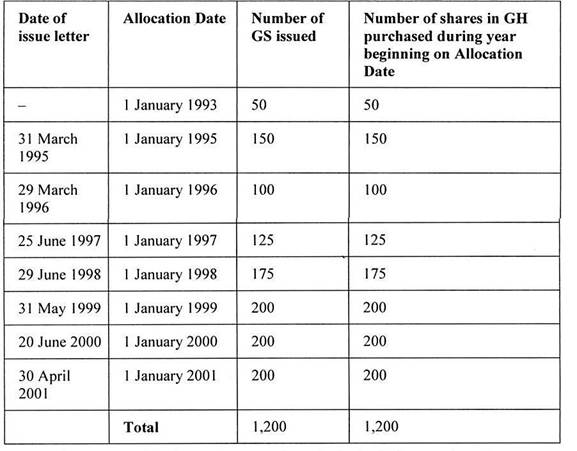

|

BETWEEN: |

VAUGHAN RUDD BLANK Applicant |

|

AND: |

COMMISSIONER OF TAXATION Respondent |

|

JUDGE: |

EDMONDS J |

|

DATE: |

21 FEBRUARY 2014 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

INTRODUCTION

1 Over the last thirty to forty years there have been any number of leading academics who have been critical of what has been called “the judicial concept of income” as a tax base, preferring instead the economists’ notion of income as “gain … during a specified time interval”, perhaps best expressed by Henry Simons in his book, Personal Income Taxation, The Definition of Income as a Problem of Fiscal Policy, University of Chicago Press, (1938). For example, see Income Taxation – An Institution in Decay?, Ross Parsons (1986) 12 Monash University Law Review 77; Avoidance, Evasion and Reform: Who Dismantled and Who’s Rebuilding the Australian Income Tax System?”, Rick Krever, (1987) 10 UNSW Law Journal 215. Simons suggested that it was folly to describe income as a flow and rejected the trust law concept of income built, as it is, on the idea of flows. In the words of Parsons (at 94):

The trust concept was not moved by any underlying notion of gain which is the only notion that could give it coherence and a claim to fairness as the base of an income tax.

On the other hand, the learned author’s conclusion going forward could only be described as one of despair. At 105 he wrote:

Overwhelming in its bulk, and intrusive into all aspects of our lives, the income tax is built on a concept of income that was designed for a purpose quite different from providing the base of a tax. As the base of a tax it is a concept lacking in any underlying principle that can command respect. The tax tests not our morality, but our submissiveness, and commands our submission with the threat of penalties. Being taxed becomes a game, albeit a dangerous game and not for the faint-hearted.

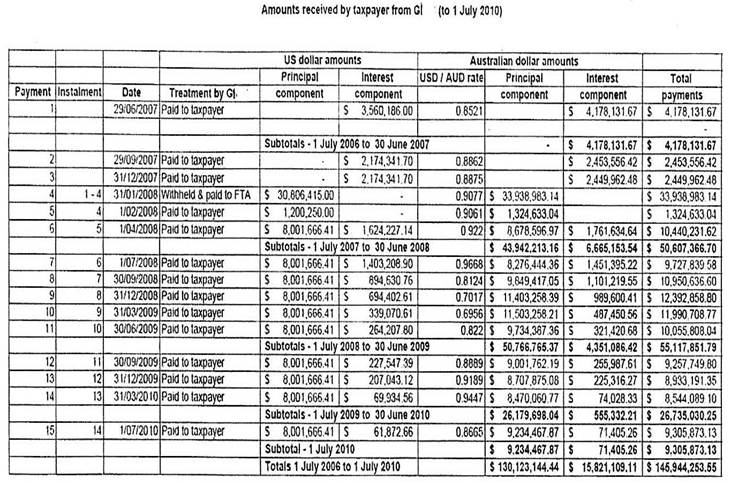

The concept of income in the natural legal meaning of the word is so entrenched by judicial decision and a ready acceptance of judicial decision by the draftsman in framing statutory provisions, that it defies change that may bring it nearer to the only notion that may give it coherent principle and a claim to fairness – the notion of gain. The income tax must start again under a new name if that is to be done, and if it can be done. The prophet of the notion of gain – Simons – compromised his revelation by accepting that it was not feasible to have a base for an income tax that extended generally to unrealised gains. In that compromise the revelation was abandoned. The notion of gain as the base of an income tax is an ideal impossible of achievement. The burdens of administration and compliance involved would press us to extinction, which may establish a correlation between the two great certainties of life.

2 The difficulties, and consequential doubts, in determining the issues raised by this case give “starch” to the criticism levelled at the judicial concept of income as a tax base; they also reinforce the importance of the first of the Henry Review’s four key areas for reform – assessing personal income on a more comprehensive basis: Australia’s future tax system – Report to the Treasurer, December 2009, Pt 1, Overview, p xvii.

3 The relevant facts of this case are recounted in more detail at [11]–[46] below, but the following summary will enable the reader to better understand, at the outset, the issues in dispute between the parties and the statutory and jurisprudential context in which those issues arise for consideration and determination.

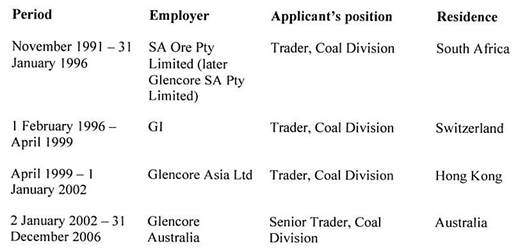

4 The applicant (on occasions referred to as the “taxpayer”) arrived in Australia in early 2002 to take up a position with Glencore Australia Pty Limited (“Glencore Australia”), a wholly owned subsidiary of Glencore International AG (“GI”). It is common ground that the applicant became a resident of Australia on 2 January 2002 and retains that fiscal status to this date. Prior to coming to Australia, the applicant had worked as an employee of GI, or one of its wholly owned subsidiaries – from 1 November 1991 to 31 January 1996 in South Africa; from 1 February 1996 to April 1999 in Switzerland; and from April 1999 to 31 December 2002 in Hong Kong. When the applicant came to this country to join Glencore Australia, he did so with some “baggage” in the form of vested and unvested entitlements to participate in an employee profit participation plan operated by GI for selected employees of the Glencore group. While working with Glencore Australia, the applicant continued to receive unvested entitlements, which subsequently vested, in the profit participation plan and in plans which replaced it in 2003 and 2005. The applicant’s employment with Glencore Australia was terminated on 31 December 2006 and he thereupon ceased to be an employee of the Glencore group of companies. On 15 March 2007 the applicant executed certain documents pursuant to the plan as it then existed and became entitled to receive USD160,033,328.25 in relinquishment of “his claim to payments with respect to [profit entitlements] allocated in his name together with all preferential and ancillary rights”. In accordance with the plan as it then existed, the USD160,033,328.25 was payable in 20 instalments over a five year period (together with interest on the outstanding balance) with the final instalment being payable on 31 December 2011.

5 The applicant treated the 15 March 2007 event as giving rise to a capital gain in the year of income ended 30 June 2007 (“2007 income year”). In his 2007 return, he returned a capital gain of AUD100,802,046, equal to the capital proceeds (the AUD equivalent of USD160,033,328.25 as at 15 March 2007)) less the cost base (which the applicant assessed at nil) reduced by 50% as a discount capital gain.

6 On 17 June 2008, an assessment was issued to the applicant for the 2007 income year as returned.

7 In May and June 2011, the respondent (“Commissioner”) issued amended assessments to the applicant for the years of income ended 30 June 2008 (“2008 income year”), 30 June 2009 (“2009 income year”) and 30 June 2010 (“2010 income year”) treating the quarterly payments as assessable as and when received on the basis that the payments were “eligible termination payments” (ss 27A and 27B of the Income Tax Assessment Act 1936 (Cth) (“1936 Act”) for the 2007 income year)/“employment termination payments” (s 82-130 of the Income Tax Assessment Act 1997 (Cth) (“1997 Act”) for the 2008 to 2010 income years) or, alternatively, that the payments were ordinary income as a reward for services.

8 In his appeal statement filed 21 December 2012, the Commissioner, for the first time, sought to defend his disallowance of the applicant’s objections to the assessment for the 2007 income year (in part, if not in whole) and the amended assessments for the 2008 to 2010 income years, on the basis that the amounts paid to the applicant, or dealt with at the direction of the applicant, in those years were assessable as dividends or non-share dividends under s 44(1) of the 1936 Act.

9 The applicant’s position on appeal is essentially that adopted in his 2007 return, although he contends that the correct cost base of his entitlement under the profit participation agreement is approximately AUD115,000,000 and not “nil” as returned.

10 The table below sets out the adjustments made by the Commissioner in the income years in dispute, and the amount of tax in dispute in those years. In respect of the 2007 income year, the table reflects the Commissioner’s position reached at the conclusion of an audit into the applicant’s affairs. The Commissioner has not, however, issued an amended assessment for the 2007 income year to give effect to that position; rather, he disallowed the applicant’s objection seeking, in the alternative, for the Commissioner to give effect to that position.

(All amounts are expressed in AUD.)

FACTUAL CONTEXT

Background

11 Between November 1991 and 31 December 2006, the applicant was employed by GI or one of its wholly owned subsidiaries.

12 The table below sets out the various employing entities, the applicant’s position and his country of residence during that period of time:

13 GI was a company incorporated in Switzerland under the name Marc Rich & Co AG, which was changed to GI in 1994. At all material times, GI was a majority owned subsidiary of Glencore Holding AG (“GH”). GH was incorporated in Switzerland under the name Newgen AG (“Newho”), which was changed to GH in 1994. At all material times, GH was the ultimate holding company of the Glencore group of companies (“Glencore Group”). The Glencore Group operated one of the world’s largest international commodity trading businesses.

Profit Participation Agreements and Shareholders’ Agreements

14 From about 1993 to 2010, GI operated employee profit participation plans (“PPPs”) whereby employees of GI (and its subsidiaries) were selected to participate in a plan and became entitled to receive financial benefits. Employees were invited to participate in a plan on the basis that they were considered key to the success of the Glencore Group, having regard to their individual performance, seniority and future potential.

15 Prior to 2006, there was only one type of PPP, later known as the ordinary profit participation plan (“OPPP”). From about May 1994 until ceasing employment with the Glencore Group with effect from 31 December 2006, the applicant participated in the OPPP.

16 The initial terms of the applicant’s participation in the OPPP were set out in two agreements executed by the applicant in around May 1994: an agreement with GI entitled “Profit Participation Agreement” (“PPA 1993”) and an agreement with GH entitled “Shareholders’ Agreement (NEWHO)” (“SA 1994”).

17 The PPA 1993 and SA 1994 were “stapled” together: the validity of the PPA 1993 was conditional on execution of the SA 1994 (PPA 1993, cl B.l) and the operation of the SA 1994 conditional on execution of the PPA 1993 (SA 1994, cll A.2, B.5).

18 Subsequently the PPA 1993 was amended and replaced:

(1) In August 1996, the applicant executed an amendment with GI amending the PPA 1993 (“PPA 1993 (as amended)”).

(2) In October 1999, the applicant executed a new Profit Participation Agreement with GI (“PPA 1999”). Clause C.7 of the PPA 1999 provided that:

Any prior oral or written agreement related to the subject matter of this Agreement in particular any Exchange Profit Participation Agreement or Profit Participation Agreement shall be terminated herewith .

This clause had the effect of terminating the PPA 1993 (as amended) prospectively i.e. from the time of the execution of the PPA 1999.

19 For present purposes, it is sufficient to note that the terms of the PPA 1993, PPA 1993 (as amended) and the PPA 1999 were substantially similar.

20 Pursuant to the SA 1994:

(1) The applicant was entitled to be issued shares in GH from time to time at a price of CHF50 per share (par value) to be paid in cash, provided the applicant had previously executed an Exchange Profit Participation Agreement or Profit Participation Agreement with GI (cll B.4, B.5).

(2) Without the prior consent of GH in writing or the occurrence of a “Triggering Event”, the applicant could not sell, assign, transfer or otherwise deal with the shares (cl D.3).

(3) A “Triggering Event” gave rise to a call option for GH, and a put option for the applicant, over all shares in GH held by the applicant at a price equal to their par value of CHF50 per share (cll D.4.1.1, D.4.2). Relevantly, termination of employment by virtue of retirement was a “Triggering Event” (cl D.4.1.1(a)).

21 Pursuant to the PPA 1999:

(1) The applicant was granted the right to participate in the “results” of GI in the form of:

(i) Genussscheine (“GS”) to be “issued” by GI to the applicant from time to time (for nil consideration), and

(ii) a contractual claim against GI (PPA 1993, cl A.l),

collectively referred to as “Profit Participation”.

Note: A Genussschein (plural Genussscheine) is a profit sharing certificate issued by a company under its articles of association pursuant to Article 657 of the Swiss Code of Obligations. Genussscheine have no par value and must not be issued in exchange for capital contributions. As noted in [23] below, in practice no physical GS certificates were ever issued to the applicant.

(2) To reflect an agreement between GI and the Swiss Federal Tax Administration (“FTA”) contained in a tax ruling issued by the FTA on 1 December 1993, so long as “the approval by the Federal Tax Authorities” was maintained, 55% of the Profit Participation was to be “received” by the applicant as a profit distribution under his GS (cl A.3.5) and the remaining 45% as a contractual claim. The 55% of the Profit Participation “received” as profit distribution under the GS was subject to Swiss dividend withholding tax of 35%, and 35% of 55% of each instalment payable to the applicant would be withheld (cl A .9).

(3) The GS “issued” were to be held for the applicant in a special blocked safekeeping account with GI (cl A.3.4).

(4) Generally, the applicant could not transfer, alienate, grant a right over, assign, cede or encumber his GS or any of his rights and claims granted under the agreement. However, he could assign the rights and claims and GS granted under the agreement to a personal holding company, trust or foundation controlled by the applicant by capital and/or votes, or otherwise, with the prior written approval of GI (cl C.2).

(5) Upon termination of the applicant’s employment with the Glencore Group, the applicant was to return to GI all of his GS and execute a Declaration of Assignment and General Release in the form annexed to the agreement (cll A.3.3, A.5).

(6) Provided that the applicant executed a Declaration of Assignment and General Release substantially in the form annexed to the agreement, then 30 days after notification of termination of the applicant’s employment, the applicant’s Profit Participation would become due (cl A.5), payable in USD in 20 quarterly instalments (cl A.6.1) and bearing interest on its unpaid balance at the six month LIBOR USD rate, compounding annually and paid with each instalment (cl A.7).

(7) The amount of the Profit Participation was determined in accordance with cl A.2. With effect from 31 December of each year the applicant was allocated a portion of the consolidated profits of GI for that year dependent on the number of GS held by the applicant at that time (“Periodical Profit Participation”) (cl A.2.3) and the amounts aggregated over the period in which the applicant held the GS to arrive at the total Profit Participation.

(8) GI could offer at any time to repurchase from the applicant part or all of the applicant’s GS on terms not more favourable than the applicant’s Profit Participation, provided GI at the same time offered to repurchase the same number of GH shares at par value (cl A. 10). From time to time GI entered into such arrangements with other employees of the Glencore Group in a similar position to the applicant.

22 In around 1994, the applicant entered into an agreement with GI entitled “Equity Participation Agreement” by which the applicant became entitled to payment of the total amount of the Special Equity A and Special Equity B accounts created under the agreement at the same time and subject to the same conditions and limitations as the applicant’s entitlement to Profit Participation under the PPA (cl 4.1).

23 Between May 1994 and 2 January 2002, from time to time GI “issued” GS to the applicant and GH issued an equal number of shares in GH to the applicant. In practice, no physical GS certificates were ever issued by GI.

24 The shares in GH and the GS were issued to the applicant upon receipt of the purchase price of the shares in GH. However, except for the GS issued in May 1994, the GS were treated for the purposes of calculating the Profit Participation under the PPA 1999 as being “allocated” as at 1 January of the year in which the GS were issued (“Allocation Date”). In the case of the GS issued in May 1994, they were treated for the purposes of PPA 1999 as being allocated on 1 January 1993.

25 As from shortly after 30 April 2001, and up until shortly after 6 May 2002, the applicant had been issued with 1,200 GS in GI and 1,200 shares in GH as set out in the table below:

26 Shortly after 6 May 2002, the applicant was issued a further 300 shares in GH and a further 300 GS were issued by GI with Allocation Date of 1 January 2002.

Incentive Profit Participation Agreement 2003

27 In about June 2003, the applicant executed an agreement entitled “Incentive Profit Participation Agreement” (“IPPA 2003”) with GI and Glencore AG (“AG”), a company incorporated in Switzerland and a wholly owned subsidiary of GI.

28 The IPPA 2003 marked a change to the structure of the OPPP. Under the IPPA 2003, rather than being issued GS in GI directly as under the previous PPAs, the applicant would be allocated with “Phantom Units” in GI (cl A.3.2). As the name suggests, the “Phantom Units” were simply a mechanism for calculating the applicant’s entitlement to Profit Participation (see IPPA 2003, cll A.1.1, A.3.1, A.3.2).

29 Under the IPPA 2003, a Phantom Unit was treated in the same way as a GS issued to the applicant under the PPA 1999 for the purposes of calculating the applicant’s Profit Participation.

30 Shortly after 7 July 2003, the applicant was issued with a further 100 shares in GH and was allocated 100 Phantom Units with an Allocation Date of 1 January 2003.

31 In around late 2004, the applicant and GI entered into an agreement entitled “Amendment to A Profit Participation Agreement” amending the terms of the IPPA 2003.

Incentive Profit Participation Agreement 2005

32 In 2005, at a time when the applicant held 1,500 GS in GI on the terms of the PPA 1999 (as amended) and 100 Phantom Units on the terms of the IPPA 2003 (as amended) and 1,600 shares in GH:

1. The applicant and GH entered into a new Shareholders’ Agreement with GH (“SA 2005”); and

2. the applicant, GI and AG entered into an agreement entitled “Incentive Profit Participation Agreement” (“IPPA 2005”).

33 The SA 2005 replaced the SA 1994 with effect from the time of execution of the SA 2005, and the IPPA 2005 replaced the PPA 1999 and IPPA 2003 with effect from the time of execution of the IPPA 2005.

34 The operation of both the IPPA 2005 and SA 2005 depended on the operation of the other (SA 2005, cl A .2, D.4.1, D.4.2; IPPA 2005, cl B.1). In particular, the IPPA 2005 was only effective if the applicant executed the SA 2005 and fulfilled his obligations thereunder to purchase the same number of shares in GH as the number of PPU allocated under the IPPA 2005.

35 Pursuant to the IPPA 2005:

(1) The applicant was granted deferred compensation called Incentive Profit Participation (“IPP”) (cl A.1.1).

(2) The IPP was calculated in the same manner as Profit Participation under the PPA 1999, but with reference to Profit Participation Units (“PPU”) rather than GS issued by GI to the applicant and Phantom Units (cll A.2, A.5 and A.6).

(3) Solely for the purposes of calculating the IPP, AG issued GS to GI to serve as PPU under the agreement (cl A.1.1, A.3.2).

(4) For the purposes of the IPPA 2005, the applicant was allocated 1,600 PPU with the same Allocation Date as the 1500 GS and 100 Phantom Units previously issued to the applicant under the PPA 1999 and the IPPA 2003 respectively (cl A.3.2, Annex B).

(5) Similarly to the position in respect of the PPA 1999, the applicant generally could not transfer, alienate, grant a right over, assign, cede or encumber his rights under the agreement. However, he could assign the rights and claims under the agreement to a personal holding company, trust or foundation controlled by the applicant provided GI gave its prior written consent to the assignment (cl C.2).

36 Because the IPPA 2005 was the PPP on foot at the time of the termination of the applicant’s employment with Glencore Australia on 31 December 2006 and also at the time he became entitled to receive USD160,033,328.25 on 15 March 2007, I think it would assist in understanding some of the analysis which follows if I reproduce, in addition to the summary in [35] above, extracts from the instruments pursuant to which the IPPA 2005 was constituted. The applicant was referred to in the instrument as the “Employee”, while GI, GH and AG were referred to by the same abbreviations:

WHEREAS, Employee is a person employed by or engaged as agent or other independent contractor performing services for .............. a branch office of GI located in ...........; or ..........., a subsidiary of GI] (such branch or subsidiary being hereinafter referred to as the “Service Provider”) which performs services for AG under a Consulting and Service Agreement between AG and GI (“Service Agreement”);

WHEREAS, the remuneration payable by AG to GI under the Service Agreement is determined with reference to the direct and indirect costs (including overhead expenses) incurred by the Service Provider;

WHEREAS, a significant portion of the services performed by the Employee are in connection with the services provided by the Service Provider for AG;

WHEREAS, GI has adopted a plan of deferred compensation known as the “Incentive Profit Participation Plan for Selected Employees of Glencore International AG and its Subsidiaries”; and

WHEREAS, in consideration of the services to be rendered by Employee to the Service Provider in connection with the Service Agreement, AG and GI have agreed that Employee should participate in such plan and Employee desires to participate in such plan;

WHEREAS, the majority of the voting stock in GI is held by Glencore Holding AG, a company incorporated and existing under the laws of Switzerland and having its registered office in Baar, Baarermattstrasse 3, of which Employee shall become a shareholder under a separate shareholders’ agreement;

NOW, THEREFORE, the parties hereto agree as follows:

Definitions

1. Allocation Date means the date as of which PPU are allocated.

2. CO means the Swiss Code of Obligations.

3. Court of Arbitration means the court of arbitration consisting of three arbitrators and having its seat in Zurich determined as per C.12.

4. Due Date means the thirtieth day after the Notice Date.

5. AG means Glencore AG, a company incorporated and existing under the laws of Switzerland and having its registered office at Baarermattstrasse 3, CH-6341, Baar, Switzerland, and an office at 301 Tresser Boulevard, Stamford, Connecticut, USA.

6. GH means Glencore Holding AG, a company incorporated under the laws of Switzerland and having its registered office at Baarermattstrasse 3, 6341 Baar, Switzerland.

7. GI means Glencore International AG, a company incorporated under the laws of Switzerland and having its registered office at Baarermattstrasse 3, 6341 Baar, Switzerland.

8. GS means “Genussscheine” issued by GI or AG as authorised by their articles of association.

9. IFRS means International Financial Reporting Standards.

10. Incentive Profit Participation / IPP means the deferred compensation calculated on the basis of the results of GI granted to Employee hereunder.

11. Measurement Date means the date as of which GI’s annual consolidated financial statements are prepared and audited.

12. Net Income for IPP means income for the year (before attribution) less attribution to minorities, adjusted by other changes in reserves (before attribution), but excluding movements in asset revaluation or equivalent reserves and cash flow hedge reserves (see Annex A).

13. Notice Date means the last day (a) of the month notice of termination of Employee by GI or a Subsidiary is received either by the Employee or by the employing company or (b) in case of death or permanent disability, of the month of the occurrence of such event or (c) such other date agreed to be the Notice Date between the parties.

14. Period Amount means IPP per PPU for a particular period.

15. Periodical IPP means the Period Amount multiplied by the number of PPU allocated to an Employee during such period.

16. Plan means a plan of deferred compensation known as the “Incentive Profit Participation Plan for Selected Employees of Glencore International AG and its Subsidiaries”.

17. Profit Participation Units / PPU means the number of GS actually allocated and participating as of a respective date, whether issued by AG under the Plan and any Incentive Profit Participation Agreement (including this Agreement) and held by GI in accordance with the terms of the Plan and this Agreement or GS issued by GI and held directly by Employees of GI or any of its Subsidiaries pursuant to profit participation agreements.

18. Service Agreement means the agreement between AG and GI for the performance of services.

19. Service Provider means the branch office of GI or the Subsidiary by which the Employee is employed or engaged as agent or other independent contractor.

20. Shareholders’ Agreement (GH) means the agreement to be executed by Employee for the shareholding in and the operation of GH.

21. Subsidiary means any direct or indirect subsidiary of GI.

A. Incentive Profit Participation

A.1 Grant; No Right to Assets

A.1.1. GI grants Employee deferred compensation which will be calculated on the basis of the results of GI (IPP). Solely for purposes of calculating the amount of IPP, AG has issued to GI GS pursuant to Section [sic] 657 CO which shall serve as PPU for the purpose of calculating Employee’s IPP as provided in A.2. below.

A.1.2. The parties to this Agreement acknowledge that the GS issued by AG and owned and held by GI are being issued solely for the purpose of implementing the Plan and calculating the amount of deferred compensation in the form of PPU which shall be allocated to Employee in accordance with the Plan and this Agreement. Employee shall not have nor be deemed to have any interest whatsoever in the GS. Employee shall not acquire by reason of the Plan or this Agreement any right in or title to any assets, funds or property of GI, AG or any other Subsidiary whatsoever, including, without limiting the generality of the foregoing, any specific funds or assets (including the GS which AG has issued to GI pursuant to A.l.l).

A.2. Calculation

A.2.1 IPP commences as of the Allocation Date. The first Measurement Date is the one following the Allocation Date.

Only such PPU that have been allocated at the Notice Date for more than 24 months from the Allocation Date shall be vested. This vesting period shall not apply in case of death or permanent disability of Employee.

A.2.2 The basis for the calculation of Employee’s IPP are the audited consolidated financial statements of GI prepared in accordance with IFRS.

A.2.3 Net Income for IPP for a particular period shall be divided by the number of PPU allocated and participating during that period to produce the Period Amount. The number of PPU participating in such period is calculated as the number of PPU participating at the Measurement Date and the PPU repurchased during that period. Where such PPU are not held for the whole calculation period, the calculation shall be performed by applying monthly fractions.

The Period Amount calculation shall be reviewed and reported by GI’s independent statutory auditors, as being in accordance with this Agreement.

A.2.4 The Periodical IPP for each allocation of PPU to Employee shall be aggregated over the period the Employee holds such PPU from the Allocation Date to and including the Notice Date. For the purpose of this Agreement, notice of termination of employment shall be valid whether made in writing or made otherwise and independent of any contestations or conditions or requirements of the law governing the employment or other engagement of the Employee.

The last Measurement Date is the date of GI’s audited consolidated financial statements following the Notice Date.

A.2.5 If, at the Notice Date, the aggregated Periodical IPP of Employee is negative, such amount shall be deemed to be zero. Such negative amount shall be proportionately allocated to the PPU allocated to Employees at the Measurement Date on or following such Notice Date.

A.3. GS

A.3.1. Under its articles of incorporation AG is authorized to issue GS which shall serve as the PPU hereunder.

A.3.2. AG has issued to GI the number of GS, and GI has allocated to Employee, the number of PPU indicated in Annex B.

Periodically, the Employee may be allocated additional PPU. IPP for such PPU commences as of the Allocation Date of such PPU, subject to the vesting conditions as per A.2.1 above.

A.3.3. With effects from Notice Date (a) AG will (i) purchase from GI the GS owned or held by GI with respect to Employee or (ii) request that GI change its records as to the GS and reallocate the PPU to a different employee selected under the terms of the Plan, and (b) the Employee shall execute and remit to GI a declaration of assignment and general release substantially in the form as per Annex C hereof.

A.4. Swiss Withholding Tax

For purposes of applying Swiss Withholding Tax Law, as long as the approval by the Swiss Federal Tax Authorities is maintained, Employee shall receive 55 percent of his IPP as profit distribution, which is subject to Swiss Withholding Tax.

A.5. Due Date

The IPP will become due as of the Due Date, provided that a declaration of assignment and general release substantially in the form as per Annex C hereof has been executed by the Employee and submitted to GI.

A.6. Payment in Instalments

A.6.1. Reservations made as to certain limitations hereinafter, IPP shall be paid by GI to Employee in twenty equal quarterly instalments over a period of five years in USD to an account designated by Employee.

A.6.2. A provisional payment shall be made to Employee on the Due Date in the amount of 75% of the first quarterly instalment, to be calculated as of the last Measurement Date for which Gl’s independent statutory auditors have reviewed and reported the Period Amount as per A.2.3 hereof.

A.6.3. The balance of the first quarterly instalment shall be paid together with the second quarterly instalment on the last day of the calendar quarter following the quarter of the Due Date.

A.6.4. The quarterly instalments shall be calculated provisionally as of the preceding Measurement Date until Gl’s independent statutory auditors have reviewed and reported the Period Amount as of such Measurement Date applicable for Employee as per A.2.5 hereof. Any balance between final and provisional calculation becomes due with the first quarterly instalment after the review and reporting of the Period Amount by Gl’s independent statutory auditors as of such Measurement Date applicable for Employee as per A.2.5 hereof.

A.7. Interest

IPP shall bear interest on its unpaid balance from the Due Date only at the rate per annum equal to the six months LIBOR (London Interbank of Offered Rate) for USD on the first day of the calendar half following the Notice Date, as published in the London Financial Times Newspaper rounded up to the next 1/16% and shall be adjusted each year as of 30 June and 31 December. Interest shall be calculated on the basis of 360 days per year and the actual number of days elapsed, compounded annually, and shall be paid with each instalment.

A.8. Set-Off

GI is entitled to set-off against IPP, to the extent permitted by law, any and all claims it or a current or future Subsidiary may have at any time against Employee irrespective of any assignment by Employee of rights and claims hereunder to a personal holding company, trust, foundation or otherwise.

A.9. Taxes and Charges

A.9.1. Except as hereinafter provided in A.9.1 and A.9.2, all payments in connection with IPP shall be made to the extent permitted by law without deduction of any taxes, charges or duties, present or future which are required to be withheld at source by GI or which are or may be levied or imposed by Switzerland or any other country or any state or political subdivision thereof. Deductions will have to be made in connection with payments of IPP for Swiss withholding tax (see A.4.) and other amounts to the extent applicable.

A.9.2. Service Provider and Employee shall mutually cooperate to arrange for the payment of any taxes required to be withheld by Service Provider from Employee with respect to the payments made hereunder. GI, AG and Employee hereby agree and acknowledge that for U.S. federal income tax purposes the payments made directly by GI to Employee hereunder represent compensation being paid in consideration of the services to be rendered by the Employee to the Service Provider. If the Employee was based within the United States at any time following the Allocation Date, GI, Service Provider and Employee shall mutually cooperate to arrange for the payment of any taxes required to be withheld by Service Provider from Employee with respect to the payments made hereunder.

B. GH Shares

B.1. Execution and Maintenance of Shareholders’ Agreement (GH)

This Agreement shall only be effective if Employee has executed the Shareholders’ Agreement (GH) and fulfilled his obligations thereunder, in particular to subscribe and pay the par value for the same number of shares in GH as the number of PPU the Employee is entitled to have allocated to him hereunder, and for as long as such Shareholders’ Agreement (GH) remains in force.

C. Miscellaneous

…

C.2. No Transfer or Encumbrance

Employee agrees for the time from the date of this Agreement to the Due Date not to transfer or to alienate otherwise, and not to grant any option right, pre-emption right or right of first refusal or the likes and not to assign, cede and encumber, pledge or to give any other lien or any rights in connection with the rights and claims granted or issued hereunder and/or the Plan, with the exception of the assignment of rights and claims granted hereunder, but not of this Agreement itself, to a personal holding company, trust or foundation controlled by capital and/or votes or otherwise by Employee, provided GI has given its prior written consent for such assignment.

If the Employee is a “United States person” within the meaning of the U.S. Internal Revenue Code, no such assignments will be permitted.

…

Annex B to Incentive Profit Participation Agreement

For: Name: Blank Vaughan

Address:

Number of PPU allocated to Employee (number of “GS” to be issued by AG and held by GI for purposes of calculating Employee’s Incentive Profit Participation):

1.1.1993 50

1.1.1995 150

1.1.1996 100

1.1.1997 125

1.1.1998 175

1.1.1999 200

1.1.2000 200

1.1.2001 200

1.1.2002 300

1.1.2003 100

Barr, in 2005

Annex C to Incentive Profit Participation Agreement

Declaration of Assignment and General Release

by

........................................................................ (Employee)

A. The Employee confirms the termination of his employment or other engagement with AG or one of the Subsidiaries. Notice of termination has been received as of ……………

B. In consideration of the sum of

USD ..................

(US Dollars ...............................................00/00)

calculated provisionally as of the preceding Measurement Date as determined in the respective agreement of the Employee with GI and AG and to be paid by GI in accordance with such agreement, and

CHF ………….

(Swiss Francs ……………………………………00/00)

to be paid by Glencore Holding AG (GH), the Employee hereby

a) relinquishes his claim to payments with respect to the PPU and GS allocated in his name together with all preferential and ancillary rights to GI.

b) assigns all his shares of GH, registered and/or held in his name together with all preferential and ancillary rights to GH, and; irrevocably authorizes GH to take over the respective certificates.

The final calculation of the above US Dollar consideration shall be made by GI and communicated to the Employee once GI’s independent statutory auditors have reviewed and reported the Period Amount for Employee’s last Measurement Date as determined in the respective agreement of the Employee with GI.

C. Per A.4. of the Incentive Profit Participation Agreement, GI is currently required to collect and pay to the Swiss tax authorities the Swiss withholding tax, which is 35% of 55% of the principal amount of Employee’s total IPP. This represents 35% of 55% of the USD consideration in B above and will be withheld from each instalment payment or any lump sum payment, as applicable. AG and/or GI may be required by law to collect and pay other amounts, which if applicable, will be withheld from each instalment payment.

D. GI and GH are entitled to set-off against the claim of the Employee as per B. above, any and all claims GH, GI or any of its direct or indirect subsidiaries may have at any time against Employee irrespective of any assignment by Employee of rights and claims under the Incentive Profit Participation Agreement to a holding company, trust, foundation or otherwise.

E. Payment of the total sum indicated under B. above shall be effected after any set off or withholding in such instalments and on such dates and under such conditions and limitations as provided for in the respective agreement of the Employee with GI, AG and GH, in particular the Incentive Profit Participation Agreement and in the Shareholders’ Agreement (GH).

F. With the exception of the payment of the total final consideration referred to in B. above, the Employee herewith explicitly releases and discharges GI, GH and any subsidiaries or affiliates of such companies (hereinafter the Companies) from any and all liabilities and/or responsibilities, both contractual or in tort, in connection with any employment, loan, profit participation or other contractual relationship between the Employee and any of the Companies.

G. If not already terminated by separate notice of termination or for other reasons, the undersigned hereby terminates his Incentive Profit Participation Agreement with GI and his Shareholders’ Agreement (GH) with GH, effective at the date hereof.

This or any other termination of the Incentive Profit Participation Agreement does not affect the confidentiality obligations as per C.9 thereof which shall continue to be effective for an undetermined period of time

H. This declaration of assignment and general release shall be governed by and construed and interpreted in accordance with the substantive laws of Switzerland.

Place and date: Signature:

_____________________

The Employee

Termination of Employment

37 On 31 December 2006, the applicant’s employment with Glencore Australia was terminated by his resignation, and the applicant ceased to be an employee of the Glencore Group of companies.

Declaration of Assignment and General Release

38 On 15 March 2007, the applicant executed a Declaration of Assignment and General Release (“Declaration”) (see Annex C in the extracts reproduced in [36] above) by which, in consideration for USD160,033,328.25 and CHF80,000, he:

(1) Relinquished “his claim to payments with respect to the PPU and GS allocated in his name together with all preferential and ancillary rights to GI”;

(2) assigned “all GS, registered and/or held in his name together with all preferential and ancillary rights, to GI, and irrevocably [authorised] GI to take over the respective certificates”; and

(3) assigned “all his shares of GH, registered and/or held in his name together with all preferential and ancillary rights to GH”.

39 The form of the Declaration was prepared by staff of GI and provided to the applicant for him to sign in late February or early March 2007. Owing to a mistaken deletion from the proforma declaration contained in Annex C of the IPPA 2005, the Declaration appears to state that the entire consideration to be received by the applicant was to be paid by GH. In fact only CHF80,000, being the par value of the applicant’s shares in GH, was to be paid by GH. The remaining USD160,033,328.25 was to be paid by GI in accordance with the “conditions and limitations” provided in the IPPA 2005 (see cl E of the Declaration).

40 In accordance with the IPPA 2005, the USD160,033,328.25 was payable in 20 instalments over a five year period (together with interest at the six month LIBOR rate for USD on the outstanding balance of the debt), with the final instalment being payable on 31 December 2011.

Receipt and Dealings with Payments

41 On 15 January 2008, the applicant (through his agent in Switzerland) executed an agreement with GI to alter his repayment schedule, the effect of which was that the applicant agreed that GI would withhold the first four instalments in order to pay the applicant’s dividend withholding tax liability to the FTA. The applicant submitted that nothing turns on the fact that the payments were treated as, in part, subject to Swiss dividend withholding tax, because the treatment under Swiss tax law is not relevant to the Australian tax law characterisation of the payments. That must be correct and, indeed, was not put in issue by the Commissioner.

42 On 31 January 2008, GI paid USD30,806,415.70 (AUD33,938,983.92) to the FTA in respect of the applicant’s dividend withholding tax liability on his IPP entitlement.

43 On or shortly after 10 March 2008, the applicant claimed relief from the FTA under the double taxation agreement between Switzerland and Australia which, relevantly, limited Swiss withholding tax on dividends (defined as meaning income from shares and other income assimilated to income from shares under Swiss law) payable by the applicant to 15%.

44 On 19 May 2008, the applicant received a refund of CHF19,571,879.32 (AUD19,360,846.10) from the FTA.

45 On 20 November 2008, GI paid a further CHF136,325 (AUD173,464) to the FTA representing a final adjustment of the applicant’s Swiss dividend withholding tax liability. In total, the applicant paid AUD14,751,601 in Swiss tax.

46 From 31 July 2007 until 1 July 2010, in accordance with its contractual obligations GI paid to the applicant, or otherwise dealt with as the applicant directed, the 14 instalment payments. The timing and amount of the payments, including the principal and interest component of each payment, is set out in the table below:

47

THE COMMISSIONER’S HEADS OF ASSESSABILITY

48 The Commissioner seeks to defend his disallowance of the applicant’s objections to the assessment for the 2007 income year and the amended assessments for the 2008 to 2010 income years under three alternative heads of assessability, namely, that the USD160,033,328.25 (“the Amount”) is, or is received as:

(1) Ordinary income;

(2) assessable dividends or non-share dividends; or

(3) assessable eligible or employment termination payments.

49 As a fall-back, or defence of last resort, the Commissioner says that the applicant derived a capital gain on the realisation of his interest in the IPPA 2005 in the 2007 income year as returned by the applicant, but concedes in that event, the amended assessments for the subsequent years fall away. There is, nevertheless, an issue in dispute arising under this head concerning the applicant’s cost base in the interest. This issue goes to the market value of the applicant’s interest in the PPP at the time he became an Australian resident on 2 January 2002: s 855-45(2) of the 1997 Act. The applicant returned the capital gain by reference to a nil cost base (see [5] above), but on the hearing of his appeal the applicant adduced evidence from an expert valuer, Mr Wayne Lonergan, that the market value of his interest in the PPP at the time he became a resident of Australia was AUD103 million. The Commissioner adduced evidence through an expert valuer, Mr Tony Samuel, that the market value of the applicant’s interest in the PPP as at 2 January 2002 was between AUD19.795 million and AUD20.626 million, certainly greater than nil, but considerably less than Mr Lonergan’s valuation.

50 In relation to the three heads of assessability upon which the Commissioner relies in [47] above, as well as the issue of assessability, there is, in relation to the first two at least, an issue as to the time of derivation. The Commissioner’s position, as exemplified by the amended assessments for the 2008 to 2010 income years, is that there was no derivation of ordinary income or dividend/non-share dividend until amounts were actually received by the applicant. The applicant’s position is that if assessable, the ordinary income or dividend/non-share dividend was derived solely in the 2007 income year and the amended assessments for the subsequent years cannot stand. The Commissioner resists the applicant’s position because, even if he is correct on assessability under one of these heads, it is common ground that he is out of time to amend the assessment (upwards) for the 2007 income year.

51 The third head of assessability upon which the Commissioner relies – assessable eligible or employment termination payments – is only relevant if the ordinary income head or the dividend/non-share dividend head is not applicable. As between those latter heads, s 6-25(2) of the 1997 Act dictates that I first consider the dividend/non-share dividend head. The ordinary income head of assessability is only relevant if the dividend/non-share dividend head of assessability is held to be inapplicable.

THE ISSUES IN DISPUTE; THEIR ANALYSIS AND DETERMINATION

52 It is convenient to identify and classify the issues in dispute by reference to the different heads upon which the Commissioner seeks to defend his disallowance of the applicant’s objections to the assessment for the 2007 income year and the amended assessments for the 2008 to 2010 income years; and discretely analyse and determine each issue by reference to any relevant statutory context or judicial authority. In relation to issues identified and classified under the same head, depending on the answer to an anterior issue, it may not be necessary to consider and analyse all such issues; on the other hand, in some cases I have taken the view, if only out of deference to the arguments of the parties, that the subsequent issue warrants summary comment and conclusion, notwithstanding the answer to the anterior issue.

First Head: Whether the amounts paid to the applicant are assessable as dividends or non-share dividends

53 The Commissioner provided the applicant with particulars of his new ground of defence through correspondence between the parties by letters dated between 22 January and 19 March 2013 including particulars that:

(1) The GS issued to the applicant by GI were non-share equity interests in GI under s 974-70(1) of the 1997 Act read with either item 1 or, in the alternative, item 2 in the table in s 974-75(1);

(2) the relevant “scheme” relied on is the profit participation agreement entered into on 5 May 1994, amended in 1996, replaced on 15 October 1999, and replaced in June 2003, together with the shareholders agreement entered into on 5 May 1994, and the steps taken to implement them;

(3) that scheme is a “financing arrangement” under s 974-130 on one or more of the following grounds:

(i) the scheme was undertaken to raise finance for GH, a connected entity of GI, as the applicant purchased shares in GH;

(ii) the scheme was undertaken to raise finance for GI, by a contribution of capital to GI by way of services in respect of which a return is paid by GI;

(4) amounts paid to the applicant or dealt with at his direction by GI in the 2007 to 2010 income years are assessable under s 44(1) of the 1936 Act either (i) as dividends under s 159GZZZP of the 1936 Act, or (ii) alternatively, as non-share dividends under s 974-120 of the 1997 Act.

54 The first issue that arises under this first head is whether, as the Commissioner contends, the GS issued to the applicant by GI were non-share equity interests in GI. If the answer to this issue is that they were, it is necessary to consider whether dividends or non-share dividends were paid by GI to the applicant and, if so, whether they are assessable and in what year or years of income. If the answer to this issue is that the GS issued to the applicant by GI were not non-share equity interests in GI, it is unnecessary to consider these other issues because the amounts paid to the applicant could not be dividends or non-share dividends.

55 The Commissioner indicated in his particulars (see [52(1)] above) that he relied on s 974-70(1); he did not rely on s 974-70(2) or s 974-80.

56 Section 974-70(1) provides:

(1) A *scheme gives rises to an equity interest in a company if, when the scheme comes into existence:

(a) The scheme satisfies the equity test in subsection 974-75(1) in relation to the company because of the existence of an interest; and

(b) The interest is not characterised as, and does not form part of a larger interest that is characterised as, a *debt interest in the company, or a *connected entity of the company, under Subdivision 974-B.

57 This provision contains two limbs, in (a) and (b), both of which must be satisfied.

58 The equity test is set out in s 974-75(1):

(1) A *scheme satisfies the equity test in this subsection in relation to a company if it gives rise to an interest set out in the following table:

|

Equity interests | |

|

Item |

Interest |

|

1 |

An interest in the company as a member or stockholder of the company. |

|

2 |

An interest that carries a right to a variable or fixed return from the company if either the right itself, or the amount of the return, is in substance or effect *contingent on the economic performance (whether past, current or future) of: (a) the company; or (b) a part of the company’s activities; or (c) a *connected entity of the company or a part of the activities of a connected entity of the company. The return may be a return of an amount invested in the interest. |

|

3 |

An interest that carries a right to a variable or fixed return from the company if either the right itself, or the amount of the return, is at the discretion of : (a) the company; or (b) a *connected entity of the company. The return may be a return of an amount invested in the interest. |

|

4 |

An interest issued by the company that: (a) gives its holder (or a *connected entity of the holder) a right to be issued with an *equity interest in the company or a *connected entity of the company; or (b) is an *interest that will, or may, convert into an equity interest in the company or a connected entity of the company. |

This subsection has effect subject to subsection (2) (requirement for financing arrangement).

59 In its concluding words, s 974-75(1) is expressed to have effect subject to s 974-75(2), which provides:

A *scheme that would otherwise give rise to an *equity interest in a company because of an item in the table in subsection (1) (other than item 1) does not give rise to an equity interest in the company unless the scheme is a *financing arrangement for the company.

60 In his particulars (see [52(2)] above), the Commissioner identified the relevant scheme as:

[T]he Profit Participation Agreement which was entered into on 5 May 1994, amended in 1996, replaced on 15 October 1999, and replaced in June 2003 (the PPA), together with the Shareholders Agreement entered into on 5 May 1994 (the SA), and the steps taken to implement them.

61 For the purposes of this case, having regard to the terms of s 974-110(1) of the 1997 Act, the applicant submitted that the relevant scheme is strictly that which existed just before 15 March 2007 when the applicant executed the Declaration, which will involve the IPPA 2005, not the IPPA 2003, and the SA 2005, not the SA 1994. I agree with that submission, but that aside, the applicant submitted that there were two substantive reasons why the scheme identified by the Commissioner did not satisfy the equity test.

62 The first reason advanced by the applicant was that the scheme identified by the Commissioner aggregates two separate schemes in an impermissible manner. The thrust of this submission was that accepting that the two separate constituent schemes were related schemes as defined in s 974-155, the conditions for them to be aggregated, as a notional scheme, set out in paras (a), (b) and (c) of s 974-70(2), were not satisfied; s 974-70(3) was satisfied in respect of each of the constituent schemes so as to render s 974-70(2) inapplicable; the related scheme provisions of ss 974-70(2) to (5) were intended to be exhaustive or “to cover the field”, so to speak, as to when aggregation was permissible; and outside those provisions, aggregation was not permissible.

63 This short summary might not do justice to the submission; it is a submission which is undoubtedly arguable, but that said, I think it is easier and, if only for that reason, preferable to decide whether the aggregate scheme as identified by the Commissioner satisfies the equity test, by reference to the second of the substantive reasons advanced by the applicant as to why it does not; it is to that matter that I now turn.

64 The second reason the applicant advanced was that, even if the aggregate scheme identified by the Commissioner is permissible, it fails the equity test in any event because it does not satisfy the requirement in s 974-75(2) that the scheme is a “financing arrangement” for GI.

65 Despite the particulars provided by the Commissioner (see [52(1)] above), it was common ground that the applicant was not a “member or stockholder” of GI such as to attract Item 1 of the table in s 974-75(1). As noted in [58] above, by virtue of s 974-75(2), the other items of the table in s 974-75(2) do not give rise to an equity interest in GI unless the scheme is a “financing arrangement” for GI.

66 The definition of “financing arrangement” is in s 974-130(1):

A *scheme is a financing arrangement for an entity if it is entered into or undertaken:

(a) to raise finance for the entity (or a *connected entity of the entity); or

(b) to fund another scheme, or a part of another scheme, that is a *financing arrangement under paragraph (a); or

(c) to fund a return, or part of a return, payable under or provided by or under another scheme, or a part of another scheme, that is a financing arrangement under paragraph (a).

67 It was common ground that GH was a connected entity of GI at all relevant times.

68 In his particulars (see [52(3)] above), the Commissioner identified two ways in which he contended that the aggregate scheme was a financing arrangement for GI:

(1) The scheme was undertaken to raise finance for GH, a connected entity of GI, as the applicant purchased shares in GH.

(2) The scheme was undertaken to raise finance for GI, by a contribution of capital to GI by way of services in respect of which a return is paid by GI.

69 In relation to the first way, the Commissioner put his case as follows: The definition of “financing arrangement” does not, in terms or by implication, import a requirement that finance must be raised to meet a capital “need” on the part of any particular entity. Such a quantitative assessment is not provided for in s 974-130(1). Rather, the section speaks in terms of a “scheme … entered into or undertaken … to raise finance”. Within this textual formulation, there is no need to consider the amount of capital to be raised. The question under s 974 is qualitative, not quantitative. Here, the scheme was a “financing arrangement” for the purpose of s 974-130(1) because it required a contribution of share capital to GH (a connected entity of GI within the meaning of s 974-130(1)(a)). That contribution was a form of “finance” for GH. Whether GH had a need for that finance in the sense that it was required for its operations, or could not otherwise have been raised, is beside the point.

70 It may be accepted that, irrespective of whether capital raised was needed or required as finance, a scheme entered into or undertaken to raise capital could be a “financing arrangement’. The need or requirement for finance is not determinative although the existence of such a need or requirement might more readily lead to the conclusion that the scheme was entered into or undertaken to raise finance. But such a conclusion might well be reached where there is no such need or requirement but where the relevant facts and circumstances lead to the conclusion that finance is being raised on a stand-by basis or as a reserve fund.

71 Equally, the amount of capital raised by the issue of shares will not, of itself, be determinative of whether the arrangement is entered into or undertaken to raise finance for the company issuing the shares. But para (a) of the definition of “financing arrangement” requires the scheme to be entered into or undertaken “to raise finance for the entity”, not just capital. The two are not coterminous, and a conclusion that a scheme is entered into or undertaken to raise capital for prudential, management or other good governance reasons will not be entered into or undertaken to raise finance which contemplates, sooner or later, expenditure of the amount raised. Unless that dichotomy is observed, each and every raising of capital, irrespective of the objective purpose of the raising, will be a raising of finance. In my view, such a conclusion is not consistent with the legislative intention to be discerned from the text of s 974-130(1), viewed in the context of Div 974 of the 1997 Act as a whole.

72 More specifically, whether or not a scheme is a “financing arrangement” will depend upon the conclusion one would draw, from all the relevant facts and circumstances, as to the purpose or object of the scheme. Contrary to the submission of the Commissioner in [68] above, the fact that capital is paid, or contributed in kind, to a company does not, without more, lead to the conclusion that the scheme was a “financing arrangement”. More is required before one can draw any such conclusion. What this exemplifies is that no relevant fact or circumstance is determinative although the weight each carries in the determination process may well be different.

73 The identity of the relevant facts and circumstances in the determination process will vary from case to case but there will be some common indicia to consider. These include the objectively discerned intention of the parties; the size and nature of the company’s business; the size and nature of its other debt obligations; the size and nature of the capital raised under the scheme; the existence and extent of any non-financing purposes of the scheme; and the identity and nature of the provider or providers of the capital so raised – which has at one end of the spectrum a bank or finance company, and at the other end employees of the company or an affiliate participating in a scheme of remuneration. All these will be relevant, albeit non-determinative, facts and circumstances in the determination process.

74 In the present case, apart from the fact that capital was raised by GH each and every time it issued shares to participants in the PPPs, there were no indicia which pointed to the scheme, as identified by the Commissioner, being a financing arrangement. Indeed, all relevant indicia point to the contrary. One has only to review SA 2005 to realise that the Commissioner’s submission has no substance. None of the recitals suggest that the purpose of SA 2005 is to raise finance for GH. Indeed, the recitals suggest that the main purpose of GH’s existence is to act as a holding company, to hold the shares of GI, and that the shareholders of GH (which include the applicant) wish to provide for the stability of GH and its majority holding in GI; to promote the continuity of the management and policies in both GI and GH; and to restrict the manner and means by which the shares in GH may be sold, assigned or otherwise transferred.

75 All of this points to the raising of capital by the issue of shares by GH to participants in the PPPs being for the ongoing internal management of both GH and GI being maintained in the hands of those participants; this is exemplified in the following clauses in the operative part of SA 2005:

C.1.3.2 The purpose of GH is the purchase from GI of up to 100% of the voting stock of GI and to hold such participation and to exercise its controlling interest in GI as a majority shareholder and through its nominees on the board of GI.

The purpose of GH is neither the generation of profits nor the distribution of dividends to Shareholders.

…

C.2.3.1. In its capacity as major shareholder of GI and through its nominees on the board of GI, GH will provide that, to the extent permitted by law, profits of GI are in principle not distributed as dividends to shareholders of GI, with the exception of a preferred dividend to GH on its registered shares B in GI as provided for in GI’s articles and necessary for covering GH’s expenses, in particular interest payments due on the loans extended by GI to GH, and GH will provide that profits are otherwise distributed according to GI’s contractual obligations, in particular under Profit Participation Agreements or Incentive Profit Participation Agreements or Profit Participation Option Agreements or other similar agreements concluded with Shareholders.

…

D.4.1.3. Unless GH’s last audited stand-alone financial statements state reserves and/or retained earnings, the purchase price for the Shares shall be equal to their par value.

Should at the time the Exercise Event occurred, GH’s last audited stand-alone financial statements state reserves and/or retained earnings, the purchase price shall be equal to the affected Shareholder’s proportionate share of shareholders’ equity, as presented in GH’s audited stand-alone financial statements, calculated on the number of Shares to be purchased. If the option is exercised between January 1 and June 30, the purchase price shall be calculated based on GH’s stand-alone financial statements as of December 31 of the preceding year, if the option is exercised between July 1 and December 31, the purchase price shall be calculated based on GH’s stand-alone financial statements of the same year.

76 For all these reasons, I do not accept the first way the Commissioner put his case as to why the aggregate scheme he identified was entered into or undertaken to raise finance for GH and, because it was a connected entity of GI, that aggregate scheme was a “financing arrangement” of GI within s 974-130(1).

77 The second way the Commissioner put his case on this issue was that the aggregate scheme was undertaken to raise finance for GI itself by a contribution of capital to GI by way of services in respect of which a return is paid by GI.

78 I have to admit of some difficulty in understanding this second way and, for that reason, have reproduced below the Commissioner’s written submissions verbatim.

79 The Commissioner submitted that the “financing arrangement” was of the kind described in the Explanatory Memorandum to the New Business Tax System (Debt and Equity) Bill 2001 (Cth):

2 .7 The raising of finance generally entails a contribution to the capital of an entity, whether by way of money, property or services, in respect of which a return is paid by the entity, be it contingent (connoting equity) or non-contingent (connoting debt). It is important, however, to consider all the relevant circumstances and features of a particular arrangement to determine whether, in substance, it is appropriately characterised as a financing arrangement or not. In this regard, the intentions of the parties to the arrangement may be relevant, but are not determinative.

2.8 In the vast majority of cases it is readily apparent whether a particular arrangement constitutes the raising of finance. The issuing of a debt/equity hybrid instrument, whether in consideration for money (as would usually be the case), property or the provision of services, would, for example, constitute a financing arrangement. Conversely, a financing arrangement is not created from a contract for personal services entered into in the ordinary course of business where, in consideration for the provision of services, the employer provides a return in the form of salary commensurate with the value of the services provided. This is the case even if there is some delay between the provision of services and the payment of the salary, as occurs when, for example, an employer provided long service leave payments in recognition of services provided several years before ...

2.9 However, the example of an employment contract demonstrates how important it is to consider all the relevant circumstances and features of a particular arrangement to determine whether, in substance, it is appropriately characterised as a financing arrangement or not. This is because in certain, albeit unusual, circumstances an employment contract may constitute a financing arrangement, as Example 2.4 shows. The example illustrates an exception to the general rule that employment contracts do not constitute financing arrangements.

80 Example 2.4 set out in the Explanatory Memorandum reads:

A company issues shares to all the members of a family except one, who is instead employed by the company for a salary contingent on profits of the company. The calculation of the salary is such that the employee receives a return equivalent to that of the other family members on their shares (increased to reflect the value of the services provided).

In these unusual circumstances the employment contract would constitute a financing arrangement because the employee is effectively funding the company by providing services instead of money. The employment contract is a substitute for shares in the company.

81 The Commissioner then submitted:

As the passages extracted from the Explanatory Memorandum above make clear, the contribution of services can constitute raising finance, and contracts for services may, in some cases, amount to financing arrangements within the meaning of s 974-130(1).

82 There is a threshold difficulty in the way of acceptance of this submission in that the applicant’s service agreement with Glencore Australia dated 2 January 2002 was not identified as being a constituent scheme or part of the aggregate scheme particularised and relied on by the Commissioner (see [52(2)] above). That difficulty aside, there are other obstacles in the way of its acceptance spelt out below.

83 The essence of the Commissioner’s submission is perhaps best summed up in the following extract from his written submissions:

The effect of the arrangement was that GI was entitled to retain profits (instead of distributing them) indefinitely and would not be required to distribute them for so long as – and to the extent that – its owners remained employed in the business. The arrangement was thus also one whereby GI raised finance, in the form of an ability to retain profits, in return for the service of its key personnel.

84 In relation to the aggregate scheme particularised by the Commissioner, the IPPA on its face did not raise, nor could have been intended to raise, any finance for GI (or GH): the applicant’s rights under the IPPA 2005 (and all previous IPPA and PPPs) were acquired for nil consideration. Furthermore, the preamble to the IPPA 2005 describes the Incentive Profit Participation Plan as one of deferred compensation for selected employees of GI and its subsidiaries for services provided by employees. Objectively, the agreements are not consistent with the Commissioner’s contention.

85 The example in the Explanatory Memorandum is clearly distinguishable from the present case. Each employee receives a salary (in no way contingent on the profits of GI or any affiliate employer company) and discretionary bonuses in addition to their rights under the PPPs so employees cannot be said to be “effectively funding the company by providing services instead of money”. Rather they are being rewarded for their performance by deferred compensation.

86 In any event, an example in an explanatory memorandum cannot control the meaning of the text of the statute: see, e.g., Brooks v Commissioner of Taxation (2000) 100 FCR 117 at 135–136. The Commissioner’s contention rests on the idea that an employee’s provision of services constitutes the provision of “finance” to the employer. Whether that is right, and s 974-130(3)(b) of the 1997 Act casts serious doubt on that notion, the relevant statutory question is whether the scheme was entered into or undertaken “to raise finance”. The word “raise” at least suggests that but for the scheme the company would not have the finance which the scheme is intended to provide, and further, that as a result of the scheme the company has an increased ability to finance activities of the company that it would not otherwise be able to finance. But under the IPPA 2005, GI acquired no more services from the employee than it was already entitled to, and had no greater ability to finance its activities.

87 For all these reasons, I do not accept the second way the Commissioner contended that the aggregate scheme was a financing arrangement for GI.

88 I am therefore of the view that the aggregate scheme particularised and relied on by the Commissioner does not satisfy the equity test in s 974-75(1) and it follows, in my view, that that scheme does not give rise to an equity interest in GI under s 974-70(1) because para (a) is not satisfied. As noted in [56] above, both limbs, paras (a) and (b), must be satisfied for a scheme to give rise to an equity interest in a company.

89 The applicant also submitted that even if, contrary to the conclusion in [87] above, the aggregate scheme particularised and relied on by the Commissioner does satisfy the equity test in s 974-75(1) so that the para (a) limb of s 974-70(1) is satisfied, that scheme will not give rise to an equity interest in GI because, under the para (b) “tie-breaker” limb of s 974-70(1), the interest can be characterised as part of a larger interest that is characterised as a debt interest in GI, or a connected entity of GI, under Subdiv 974-B. It is not necessary that I consider this submission having regard to my conclusion that the equity test in s 974-75(1) is not satisfied and the para (a) limb of s 974-70(1) is therefore not satisfied. However, I should say that I do not accept the submission: I am not satisfied that the “effectively non-contingent obligation” requirement in para (c) of the debt test in s 974-20(1) is satisfied having regard to the terms of s 974-135(3) as to when an obligation is non-contingent.

90 But it does follow from my conclusion in [87] above that the GS issued to the applicant by GI were not equity interests, and therefore not non-share equity interests, in GI, that the amounts paid to the applicant by GI could not be dividends or non-share dividends. It is therefore strictly unnecessary to consider the assessability of such amounts and, if assessable, the year or years of derivation; however, I will make the following summary comments and conclusions on the premise that such amounts were dividends or non-share dividends.

91 If they were dividends, they would only be dividends by operation of s 159GZZZP(1) of the 1936 Act – where there is a buy-back of a share or a non-share equity interest by a company in an off-market purchase – which provides that an arithmetical difference “is taken to be a dividend paid by the company –

(c) to the seller as a shareholder in the company; and

(d) out of profits derived by the company; and

(e) on the day the buy-back occurs.”

While such a dividend would be assessable to the applicant by virtue of s 44(1)(a)(i) of the 1936 Act, it would be wholly assessable in the 2007 income year (s 159GZZZP(1)(e)). So much was conceded by the Commissioner.

92 If the amounts paid to the applicant by GI were non-share dividends by virtue of ss 974-115 and 974-120 of the 1997 Act, they would not be assessable under s 44(1)(a)(ii) of the 1936 Act because the applicant was not a “shareholder” in GI and there is no relevant deeming as there is in s 159GZZZP(1)(c). That difficulty aside, any assessability under s 44(1) would arise in the 2007 income year when the non-share dividend was “paid” by GI. There could be no argument that in that year the non-share dividend was, at the request and with the agreement of the applicant, credited to him in full: see the definition of “paid” in relation to dividends or non-share dividends in s 6(1) of the 1936 Act; see too Brookton Co-operative Society Limited v Federal Commissioner of Taxation (1980–1981) 147 CLR 441 at 455–456 per Mason J.

Second Head: Whether the Amount is ordinary income

93 In the alternative, the Commissioner submitted that the Amount was ordinary income on one or more of three grounds:

(1) Deferred compensation as a reward for services as an employee;

(2) even if the GS should be characterised as assets of the applicant (in the form of “contractual rights” as submitted by the applicant), they were revenue assets and the gain on the realisation of them is ordinary income under the principles coming out of Federal Commissioner of Taxation v Myer Emporium Ltd (1986–1987) 163 CLR 199; and

(3) it was income from property: reliance was placed on what was said in Commissioner of Taxation v McNeil (2007) 229 CLR 656 using the applicant’s holding of GH shares as the identifiable property left intact by way of analogy to Mrs McNeil’s holding of shares in St George Bank.

94 I do not propose to consider the second and third grounds because, in my view, they have no arguable merit. It is sufficient to dispose of the second ground to say that the applicant was not carrying on any business to which the first, as distinct from the second, strand of reasoning in Myer Emporium might attach (see S P Investments Pty Ltd v Commissioner of Taxation (1993) 41 FCR 282 at 297 per Hill J, with whom Burchett and O’Loughlin JJ agreed). It is sufficient to dispose of the third ground to say that the GH analogy is not only irrelevant, but wrong. The relevant company is GI and the applicant held no interest in that company, if it ever held such an interest, upon execution of the Declaration on 15 March 2007.

95 It is the first ground – deferred compensation as a reward for services as an employee – which demands closer scrutiny. There can be no doubt, if the recitals (called preamble) to the instruments under the last two manifestations of the PPPs – the IPPA 2003 and the IPPA 2005 – can be taken as a guide, that the plans were intended by the relevant parties – GI, AG and the applicant – to provide the applicant with deferred compensation in consideration of the services to be rendered by the applicant to his Glencore Group employer. Further support for this conclusion is to be drawn from the operative part of the instruments, in the case of the IPPA 2005 – the definition of Incentive Profit Participation/IPP and Plan in paras 10 and 16; Clause A.14.1; “GI grants Employee deferred compensation…”; and Clause A.1.2 refers to GS being “issued solely for the purpose of … calculating the amount of deferred compensation”.

96 But the applicant says that what was provided as a reward for services as an employee were the GS issued to him, not the proceeds of their subsequent realisation following the termination of his employment. According to the applicant, each GS was a benefit which was capable of being turned to pecuniary account and hence was income according to ordinary concepts as a reward for services or, alternatively, was a benefit “allowed, given or granted” to the applicant in respect of, or for, or in relation directly or indirectly to his employment in the year of income in which they were “allowed given or granted” within the meaning of the former s 26(e) of the 1936 Act.

97 The difficulty I have with the applicant’s submission is that it is predicated on a premise which does not accord with the facts. Whatever the applicant was granted or issued with under earlier manifestations of the PPPs, the applicant was not granted and did not hold anything in the way of a right or interest in property under the IPPA 2005: see cll A.1.1 and A.1.2 which make it clear that AG issued GS to GI not to the applicant; that the applicant did not have any interest whatsoever in the GS; that the applicant did not acquire by reason of the plan or the IPPA 2005 any right in or title to any assets, funds or property of GI, AG or any other subsidiary whatsoever, including any specific funds or assets (including the GS which AG issued to GI). Indeed, under the IPPA 2005 the applicant was granted, and held, nothing more than a contractual right, if one of certain nominated events occurred and if he executed and submitted to GI the Annex C Declaration before a fixed date, to become a creditor of GI on that fixed date for a sum of money quantified by reference to a formula, which debt was payable, together with interest, by 20 equal quarterly instalments.